Form 1040 is one of three IRS tax forms used for personal (individual) federal income tax returns filed with the Internal Revenue Service (IRS) by United States residents for tax purposes.

A wage is monetary compensation paid by an employer to an employee in exchange for work done. Payment may be calculated as a fixed amount for each task completed, or at an hourly or daily rate, or based on an easily measured quantity of work done.

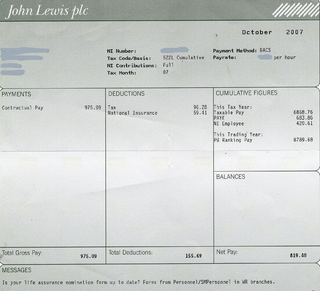

Payroll taxes are taxes imposed on employers or employees, and are usually calculated as a percentage of the salaries that employers pay their staff. Payroll taxes generally fall into two categories: deductions from an employee’s wages, and taxes paid by the employer based on the employee's wages. The first kind are taxes that employers are required to withhold from employees' wages, also known as withholding tax, pay-as-you-earn tax (PAYE), or pay-as-you-go tax (PAYG) and often covering advance payment of income tax, social security contributions, and various insurances. The second kind is a tax that is paid from the employer's own funds and that is directly related to employing a worker. These can consist of fixed charges or be proportionally linked to an employee's pay. The charges paid by the employer usually cover the employer's funding of the social security system, medicare, and other insurance programs. The economic burden of the payroll tax falls almost entirely on the worker, regardless of whether the tax is remitted by the employer or the employee, as the employers’ share of payroll taxes is passed on to employees in the form of lower wages than would otherwise be paid. Because payroll taxes fall exclusively on wages and not on returns to financial or physical investments, payroll taxes may contribute to underinvestment in human capital such as higher education.

A payroll is a company's list of its employees, but the term is commonly used to refer to:

Garnishment is a legal process for collecting a monetary judgment on behalf of a plaintiff from a defendant. Garnishment allows the plaintiff to take the money or property of the debtor from the person or institution that holds that property. A similar legal mechanism called execution allows the seizure of money or property held directly by the debtor.

Form W-2 is an Internal Revenue Service (IRS) tax form used in the United States to report wages paid to employees and the taxes withheld from them. Employers must complete a Form W-2 for each employee to whom they pay a salary, wage, or other compensation as part of the employment relationship. An employer must mail out the Form W-2 to employees on or before January 31. This deadline gives these taxpayers about 2 months to prepare their returns before the April 15 income tax due date. The form is also used to report FICA taxes to the Social Security Administration. The Form W-2, along with Form W-3, generally must be filed by the employer with the Social Security Administration by the end of February. Relevant amounts on Form W-2 are reported by the Social Security Administration to the Internal Revenue Service. In territories, the W-2 is issued with a two letter code indicating which territory, such as W-2GU for Guam. If corrections are made, it can be done on a W-2c.

Remuneration is the pay or other compensation provided in exchange for an employee’s services performed. A number of complementary benefits in addition to pay are increasingly popular remuneration mechanisms. Remuneration is one component of reward management.

Joseph Ronald Banister is a former special agent of the Criminal Investigation Division of the Internal Revenue Service (IRS) and anti-tax activist. Banister resigned from the IRS and later appeared on the television program "60 Minutes II" challenging the conduct of the IRS concerning legal issues with taxation. Banister's books and other material challenge the legality of some aspects of the income tax.

A withholding tax, or a retention tax, is an income tax to be paid to the government by the payer of the income rather than by the recipient of the income. The tax is thus withheld or deducted from the income due to the recipient. In most jurisdictions, withholding tax applies to employment income. Many jurisdictions also require withholding tax on payments of interest or dividends. In most jurisdictions, there are additional withholding tax obligations if the recipient of the income is resident in a different jurisdiction, and in those circumstances withholding tax sometimes applies to royalties, rent or even the sale of real estate. Governments use withholding tax as a means to combat tax evasion, and sometimes impose additional withholding tax requirements if the recipient has been delinquent in filing tax returns, or in industries where tax evasion is perceived to be common.

Income taxes in the United States are imposed by the federal, most state, and many local governments. The income taxes are determined by applying a tax rate, which may increase as income increases, to taxable income, which is the total income less allowable deductions. Income is broadly defined. Individuals and corporations are directly taxable, and estates and trusts may be taxable on undistributed income. Partnerships are not taxed, but their partners are taxed on their shares of partnership income. Residents and citizens are taxed on worldwide income, while nonresidents are taxed only on income within the jurisdiction. Several types of credits reduce tax, and some types of credits may exceed tax before credits. An alternative tax applies at the federal and some state levels.

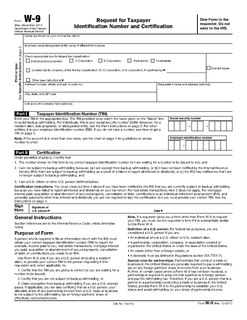

Form W-9 is used in the United States income tax system by a third party who must file an information return with the Internal Revenue Service (IRS). It requests the name, address, and taxpayer identification information of a taxpayer.

Form W-4 is an Internal Revenue Service (IRS) tax form completed by an employee in the United States to indicate his or her tax situation to the employer. The W-4 form tells the employer the correct amount of tax to withhold from an employee's paycheck.

Tax protesters in the United States have advanced a number of arguments asserting that the assessment and collection of the federal income tax violates statutes enacted by the United States Congress and signed into law by the President. Such arguments generally claim that certain statutes fail to create a duty to pay taxes, that such statutes do not impose the income tax on wages or other types of income claimed by the tax protesters, or that provisions within a given statute exempt the tax protesters from a duty to pay.

Internal Revenue Service (IRS) tax forms are forms used for taxpayers and tax-exempt organizations to report financial information to the Internal Revenue Service of the United States. They are used to report income, calculate taxes to be paid to the federal government, and disclose other information as required by the Internal Revenue Code (IRC). There are over 800 various forms and schedules. Other tax forms in the United States are filed with state and local governments.

The Foreign Investment in Real Property Tax Act of 1980 (FIRPTA), enacted as Subtitle C of Title XI of the Omnibus Reconciliation Act of 1980, Pub. L. No. 96-499, 94 Stat. 2599, 2682, is a United States tax law that imposes income tax on foreign persons disposing of US real property interests. Tax is imposed at regular tax rates for the taxpayer on the amount of gain considered recognized. Purchasers of real property interests are required to withhold tax on payment for the property. Withholding may be reduced from the standard 15% to an amount that will cover the tax liability, upon application in advance of sale to the Internal Revenue Service. FIRPTA overrides most nonrecognition provisions as well as those remaining tax treaties that provide exemption from tax for such gains.

A Qualified Intermediary refers to a person that acts as an intermediary qualified under certain sections of the U.S. Internal Revenue Code (IRC) to undertake specified activities.

A tax protester is someone who refuses to pay a tax claiming that the tax laws are unconstitutional or otherwise invalid. Tax protesters are different from tax resisters, who refuse to pay taxes as a protest against a government or its policies, or a moral opposition to taxation in general, not out of a belief that the tax law itself is invalid. The United States has a large and organized culture of people who espouse such theories. Tax protesters also exist in other countries.

In the United States, Form 1099-R is a variant of Form 1099 used for reporting on distributions from pensions, annuities, retirement or profit sharing plans, IRAs, charitable gift annuities and Insurance Contracts. Form 1099-R is filed for each person who has received a distribution of $10 or more from any of the above.