The Fair Deal was an ambitious set of proposals put forward by U.S. President Harry S. Truman to Congress in his January 1949 State of the Union address. More generally the term characterizes the entire domestic agenda of the Truman administration, from 1945 to 1953. It offered new proposals to continue New Deal liberalism, but with the Conservative Coalition controlling Congress, only a few of its major initiatives became law and then only if they had considerable GOP support. As Richard Neustadt concludes, the most important proposals were aid to education, universal health insurance, the Fair Employment Practices Commission, and repeal of the Taft–Hartley Act. They were all debated at length, then voted down. Nevertheless, enough smaller and less controversial items passed that liberals could claim some success.

Section 8 of the Housing Act of 1937, often called Section 8, as repeatedly amended, authorizes the payment of rental housing assistance to private landlords on behalf of approximately 4.8 million low-income households, as of 2008, in the United States. The largest part of the section is the Housing Choice Voucher program which pays a large portion of the rents and utilities of about 2.1 million households. The U.S. Department of Housing and Urban Development manages Section 8 programs.

An FHA insured loan is a US Federal Housing Administration mortgage insurance backed mortgage loan which is provided by an FHA-approved lender. FHA insured loans are a type of federal assistance and have historically allowed lower income Americans to borrow money for the purchase of a home that they would not otherwise be able to afford. Because this type of loan is more geared towards new house owners rather than real-estate investors, FHA loans are different from conventional loan in the sense that the house must be owner occupant for at least a year. Since loans with lower down-payments usually involve more risk to the lender, the home-buyer must pay a two-part mortgage insurance which involves a one-time bulk payment in addition to a monthly payment to compensate for the increased risk.

Canada Mortgage and Housing Corporation (CMHC) is a Crown Corporation of the Government of Canada. Its superseding agency was established after World War II, to help returning war veterans find housing. It has since expanded its mandate to assist housing for all Canadians. The organization's primary goals are to provide mortgage liquidity, assist in affordable housing development, and provide unbiased research and advice to the Canadian government, and housing industry.

The Federal Agriculture Improvement and Reform Act of 1996, known informally as the Freedom to Farm Act, the FAIR Act, or the 1996 U.S. Farm Bill, was the omnibus 1996 farm bill that, among other provisions, revises and simplifies direct payment programs for crops and eliminates milk price supports through direct government purchases.

The Oklahoma Housing Finance Agency (OHFA) is a non-profit organization which serves the people of Oklahoma by offering affordable housing resources, including loans and rent assistance. OHFA was created in 1975 when Governor of Oklahoma David L. Boren approved the agency's first trust indenture. OHFA is a public trust with the State of Oklahoma as the beneficiary. The Trust was established to better the housing stock and the housing conditions in the State of Oklahoma and administers the Section 8 housing program along with other housing programs for the State.

The Housing and Economic Recovery Act of 2008 was designed primarily to address the subprime mortgage crisis. It authorized the Federal Housing Administration to guarantee up to $300 billion in new 30-year fixed rate mortgages for subprime borrowers if lenders wrote down principal loan balances to 90 percent of current appraisal value. It was intended to restore confidence in Fannie Mae and Freddie Mac by strengthening regulations and injecting capital into the two large U.S. suppliers of mortgage funding. States are authorized to refinance subprime loans using mortgage revenue bonds. Enactment of the Act led to the government conservatorship of Fannie Mae and Freddie Mac.

Public housing policies in Canada includes rent controls, as well as subsidized interest rates and grants. Early public housing policy in Canada consisted of public-private lending schemes which focused on expanding home ownership among the middle class. The first major housing initiative in Canada was the Dominion Housing Act of 1935, which increased the amount of credit available for mortgage loans.

Loan modification is the systematic alteration of mortgage loan agreements that help those having problems making the payments by reducing interest rates, monthly payments or principal balances. Lending institutions could make one or more of these changes to relieve financial pressure on borrowers to prevent the condition of foreclosure. Loan modifications have been practiced in the United States since The 2008 Crash Of The Housing Market from Washington Mutual, Chase Home Finance, Chase, JP Morgan & Chase, other contributors like MER's. Crimes of Mortgage ad Real Estate Staff had long assisted nd finally the squeaky will could not continue as their deviant practices broke the state and crashed. Modification owners either ordered by The United States Department of Housing, The United States IRS or President Obamas letters from Note Holders came to those various departments asking for the Democratic process to help them keep their homes and protection them from explosion. Thus the birth of Modifications. It is yet to date for clarity how theses enforcements came into existence and except b whom, but t is certain that note holders form the Midwest reached out in the Democratic Process for assistance. FBI Mortgage Fraud Department came into existence. Modifications HMAP HARP were also birthed to help note holders get Justice through reduced mortgage by making terms legal. Modification of mortgage terms was introduced by IRS staff addressing the crisis called the HAMP TEAMS that went across the United States desiring the new products to assist homeowners that were victims of predatory lending practices, unethical staff, brokers, attorneys and lenders that contributed to the crash. Modification were a fix to the crash as litigation has ensued as the lenders reorganized and renamed the lending institutions and government agencies are to closely monitor them. Prior to modifications loan holders that experiences crisis would use Loan assumptions and Loan transfers to keep the note in the 1930s. During the Great Depression, loan transfers, loan assumption, and loan bail out programs took place at the state level in an effort to reduce levels of loan foreclosures while the Federal Bureau of Investigation, Federal Trade Commission, Comptroller, the United States Government and State Government responded to lending institution violations of law in these arenas by setting public court records that are legal precedence of such illegal actions. The legal precedents and reporting agencies were created to address the violations of laws to consumers while the Modifications were created to assist the consumers that are victims of predatory lending practices. During the so-called "Great Recession" of the early 21st century, loan modification became a matter of national policy, with various actions taken to alter mortgage loan terms to prevent further economic destabilization. Due to absorbent personal profits nothing has been done to educate Homeowners or Creditors that this money from equity, escrow is truly theirs the Loan Note Holder and it is their monetary rights as the real prize and reason for the Housing Crash was the profit n obtaining the mortgage holders Escrow. The Escrow and Equity that is accursed form the Note Holders payments various staff through the United States claimed as recorded and cashed by all staff in real-estate from local residential Tax Assessing Staff, Real Estate Staff, Ordinance Staff, Police Staff, Brokers, attorneys, lending institutional staff but typically Attorneys who are also typically the owners or Rental properties that are trained through Bankruptcies'. that collect the Escrow that is rightfully the Homeowners but because most Homeowners are unaware of what money is due them and how they can loose their escrow. Most Creditors are unaware that as the note holder that the Note Holder are due a annual or semi annual equity check and again bank or other lending and or legal intuitions staff claim this monies instead. This money Note Holders were unaware of is the prize of real estate and the cause of the Real Estate Crash of 2008 where Lending Institutions provided mortgages to people years prior they know they would eventually loose with Loan holders purchasing Balloon Mortgages lending product that is designed to make fast money off the note holder whom is always typically unaware of their escrow, equity and that are further victimized by conferences and books on HOW TO MAKE MONEY IN REAL STATE - when in fact the money is the Note Holder. The key of the crash was not the House, but the loan product used and the interest and money that was accrued form the note holders that staff too immorally. The immoral and illegal actions of predatory lending station and their staff began with the inception of balloon mortgages although illegal activity has always existed in the arena, yet the crash created "Watch Dog" like HAMP TEAM, IRS, COMPTROLLER< Federal Trade Commission Consumer Protection Bureau, FBI, CIA, Local Police Department, ICE and other watch dog agencies came into existence to examine if houses were purchased through a processed check at Government Debited office as many obtained free homes illegally. Many were incarcerated for such illegal actions. Modifications fixed the Notes to proper lower interest, escrow, tax fees that staff typically raised for no reason. Many people from various arenas involved in reals estate have been incarcerated for these actions as well as other illegal actions like charging for a modification. Additionally Modifications were also made to address the falsifications such as inappropriate mortgage charges, filing of fraudulently deeds, reporting of and at times filing of fraudulent mortgages that were already paid off that were fraudulently continued by lenders staff and attorneys or brokers or anyone in the Real Estate Chain through the issues of real estate terms to continue to violate United States Laws, contract law and legal precedence where collusion was often done again to defraud and steal from the Note Holder was such a common practice that was evidence as to why the Mortgage Crash in 2008 occurred for the purpose of wining the prize of stealing form Homeowners and those that foreclosed was actually often purposefully for these monies note holders were unaware of to be obtained which was why Balloon mortgages and loans were given to the staff in the Real Estate Market with the hoper and the expectation that the loan holders would default as it offered opportunity to commit illegal transactions of obtaining the homeowners funds. While such scams were addressed through modifications in 2008. The Market relied heavily on Consumers ignorance to prosper, ignorance of real estate terms, ignorance on what they were to be charged properly for unethical financial gain and while staff in real estates lending arenas mingled terms to deceive y deliberate confusion consumers out of cash and homes while the USA Government provided Justice through President Obamas Inception and IRS Inception of Modifications which addressed these unethical profits in Reals Estate. It was in 2009 that HARP, HAMP and Modifications were introduced to stop the victimization of Note Holders. Taking on the Banks that ran USA Government was a great and dangerous undertaking that made America Great Again as Justice for Consumers reigned. Legal action taken against institutions that have such business practices can be viewed in State Code of Law and Federal Law on precedent cases that are available to the public. Finally, It had been unlawful to be charged by an attorney to modify as well as for banking staff to modify terms to increase a mortgage and or change lending product to a balloon in an concerted effort to make homeowner foreclose which is also illegal, computer fraud and not the governments intended purpose or definition of a modification. There are reputable companies that are trained to assist with foreclosure defense and home retention options. In addition, hud.gov offers a variety of non-profit agencies that offer assistance.

Section 533 grants are a USDA rural housing rehabilitation program authorized under Section 533 of the Housing Act of 1949. The Rural Housing Service (RHS) is authorized to make grants to capable organizations for:

Section 524 loans are land acquisition and development loans in the United States that are authorized under Section 524 of the federal Housing Act of 1949.

Section 523 loans are a mutual self-help rural housing program authorized under Section 523 of the Housing Act of 1949 and administered by the Rural Housing Service (RHS). Nonprofit organizations may obtain 2-year loans to purchase and develop land that is to be subdivided into building sites for housing. The interest rate is 3% for these loans. Applicants must demonstrate a need for the proposed building sites in the locality. Sponsors also may obtain technical assistance (TA) grants to pay for all or part of the cost of developing, administering, and coordinating programs of technical and supervisory assistance to the families who are building their own homes. Each family is expected to contribute at least 700 hours of labor in building homes for each other. Applicants must demonstrate that:

Section 521 rental assistance is rental assistance authorized under Section 521 of the Housing Act of 1949. Owners of housing financed under Section 515 or Section 514 may receive rental assistance payments from the Rural Housing Service (RHS). The assistance payments enable eligible tenants to make monthly rent payments that do not exceed the greater of: (1) 30% of monthly adjusted family income; (2) 10 percent of monthly income; or, (3) the portion of the family’s welfare payment that is designated for housing costs. The rental assistance payments, which are made directly to the borrowers, make up the difference between the tenants’ payments and the RHS-approved rent for the units. Borrowers must agree to operate the property on a limited profit or nonprofit basis. The term of the rental assistance agreement is 20 years for new construction projects and 5 years for existing projects. Agreements may be renewed for up to 5 years. An eligible borrower who does not participate in the program may be petitioned to participate by 20 percent or more of the tenants eligible for rental assistance.

Section 516 grants are a USDA farm labor housing program authorized by Section 516 of the Housing Act of 1949. Qualified nonprofit organizations, Indian tribes, or public bodies obtain grants for the development cost of farm labor housing. Grants may be used simultaneously with Section 514 loans if the housing, for which there is a “pressing need,” will not be built without assistance from the Rural Housing Service (RHS). Grants may be made for up to 90% of the development cost of the housing. In a given fiscal year, up to 10% of the Section 516 funds shall be for domestic and migrant farm worker housing. Applicants must contribute at least 10% of the total development costs from their own resources or from other sources including Section 514 loans. Funds may be used to buy, build, or improve housing and related facilities for farm workers, and to purchase and improve the land where the housing will be located, including installation of streets, water supply and waste disposal systems, parking areas, and driveways as well as for the purchase and installation of appliances such as ranges, refrigerators, and clothes washers and dryers. Related facilities may include the maintenance workshop, recreation center, small infirmary, laundry room, day care center, and office and living quarters for the resident manager.

Section 514 loans are a domestic, farm labor housing program in the United States, authorized under Section 514 of the Housing Act of 1949. They are the only nationwide program to provide housing for farm laborers. The Rural Housing Service (RHS) makes loans to farm owners, associations of farm owners, Indian tribes, or nonprofit organizations to provide modest living quarters, basic household furnishings, and related facilities. Loans may also be used to repair existing housing for farm labor use. The loans are repayable in 33 years and bear an interest rate of 1%.

Section 504 loans and grants are a USDA rural housing repair program authorized under Section 504 of the Housing Act of 1949. Under current regulations, rural homeowners with incomes of 50% or less of the area median may qualify for the Rural Housing Service (RHS) direct loans to repair their homes. Loans are limited to $20,000 and have a 20-year term at a 1% interest rate. Owners of age 62 or more may qualify for grants of up to $7,500 to pay for needed repairs that remove a health or safety hazard. To qualify for the grants, the elderly must be unable to obtain affordable credit elsewhere. Depending on the cost of the repairs and the income of the homeowner, the owner may be eligible for a grant for the full cost of the repairs or for some combination of a loan and a grant to covers repair costs. The combination loan and grant may total no more than $20,000.

Section 502 loans are a rural housing loan program, administered by the Rural Housing Service (RHS), authorized under Section 502 of the Housing Act of 1949. Borrowers may obtain loans for purchasing or repairing new or existing single-family housing. Loans are made directly by RHS or by private lenders with a USDA guarantee. Borrowers with income of 80% or less of the area median may be eligible for 33- year direct loans and may receive interest credit to bring the interest rate to as low as 1%. In a given fiscal year, at least 40% of the units financed under this section must be made available only to very low-income families or individuals with terms up to 38 years. Borrowers must have the means to repay the loans, but be unable to secure reasonable credit terms elsewhere. Borrowers with income of up to 115% of the area median may be eligible for 30-year guaranteed loans from private lenders. Priority is given to first-time home buyers, and the RHS may require that borrowers complete a home ownership counseling program.

The Consolidated Farm and Rural Development Act, authorizes the Farm Service Agency to make direct and guaranteed farm ownership loans to eligible family farmers.

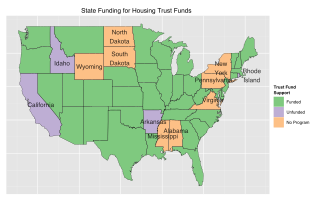

Housing trust funds are established sources of funding for affordable housing construction and other related purposes created by governments in the United States (U.S.). Housing Trust Funds (HTF) began as a way of funding affordable housing in the late 1970s. Since then, elected government officials from all levels of government in the U.S. have established housing trust funds to support the construction, acquisition, and preservation of affordable housing and related services to meet the housing needs of low-income households. Ideally, HTFs are funded through dedicated revenues like real estate transfer taxes or document recording fees to ensure a steady stream of funding rather than being dependent on regular budget processes. As of 2016, 400 state, local and county trust funds existed across the U.S.

The Transportation, Housing and Urban Development, and Related Agencies Appropriations Act, 2015 is an appropriations bill that would provide funding for the United States Department of Transportation and the United States Department of Housing and Urban Development (HUD) for fiscal year 2015.