Intellectual property (IP) is a category of property that includes intangible creations of the human intellect. There are many types of intellectual property, and some countries recognize more than others. The best-known types are patents, copyrights, trademarks, and trade secrets. The modern concept of intellectual property developed in England in the 17th and 18th centuries. The term "intellectual property" began to be used in the 19th century, though it was not until the late 20th century that intellectual property became commonplace in most of the world's legal systems.

Property law is the area of law that governs the various forms of ownership in real property (land) and personal property. Property refers to legally protected claims to resources, such as land and personal property, including intellectual property. Property can be exchanged through contract law, and if property is violated, one could sue under tort law to protect it.

Personal property is property that is movable. In common law systems, personal property may also be called chattels or personalty. In civil law systems, personal property is often called movable property or movables—any property that can be moved from one location to another.

Business is the practice of making one's living or making money by producing or buying and selling products. It is also "any activity or enterprise entered into for profit."

A sales tax is a tax paid to a governing body for the sales of certain goods and services. Usually laws allow the seller to collect funds for the tax from the consumer at the point of purchase.

In common law, an estate is a living or deceased person's net worth. It is the sum of a person's assets – the legal rights, interests, and entitlements to property of any kind – less all liabilities at a given time. The issue is of special legal significance on a question of bankruptcy and death of the person.

A shell corporation is a company or corporation with no significant assets or operations often formed to obtain financing before beginning business. Shell companies were primarily vehicles for lawfully hiding the identity of their beneficial owners, and this is still the defining feature of shell companies due to the loopholes in the global corporate transparency initiatives. It may hold passive investments or be the registered owner of assets, such as intellectual property, or ships. Shell companies may be registered to the address of a company that provides a service setting up shell companies, and which may act as the agent for receipt of legal correspondence. The company may serve as a vehicle for business transactions without itself having any significant assets or operations.

Intangible property, also known as incorporeal property, is something that a person or corporation can have ownership of and can transfer ownership to another person or corporation, but has no physical substance, for example brand identity or knowledge/intellectual property.

A use tax is a type of tax levied in the United States by numerous state governments. It is essentially the same as a sales tax but is applied not where a product or service was sold but where a merchant bought a product or service and then converted it for its own use, without having paid tax when it was initially purchased. Use taxes are functionally equivalent to sales taxes. They are typically levied upon the use, storage, enjoyment, or other consumption in the state of tangible personal property that has not been subjected to a sales tax.

In law, the situs of property is where the property is treated as being located for legal purposes. This may be important when determining which laws apply to the property, since the situs of an object determines the lex situs, that is, the law applicable in the jurisdiction where the object is located, which may differ from the lex fori, the law applicable in the jurisdiction where a legal action is brought. For example, real estate in England is subject to English law, real estate in Scotland is subject to Scottish law, and real estate in France is subject to French law.

The Modified Accelerated Cost Recovery System (MACRS) is the current tax depreciation system in the United States. Under this system, the capitalized cost (basis) of tangible property is recovered over a specified life by annual deductions for depreciation. The lives are specified broadly in the Internal Revenue Code. The Internal Revenue Service (IRS) publishes detailed tables of lives by classes of assets. The deduction for depreciation is computed under one of two methods (declining balance switching to straight line or straight line) at the election of the taxpayer, with limitations. See IRS Publication 946 for a 120-page guide to MACRS.

A gift, in the law of property, is the voluntary and immediate transfer of property from one person to another without consideration. There are several type of gifts in property law, most notably inter vivos gifts which are made in the donor's lifetime and causa mortis (deathbed) gifts which are made in expectation of the donor's imminent death. Both types of gifts share three elements which must be met in order for the gift to be legally effective: donative intent, the delivery of the gift to the donee, and the acceptance of the gift. In addition to those elements, causa mortis gifts require that the donor must die of the impending peril that he or she had contemplated when making the gift.

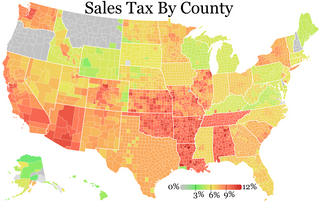

Sales taxes in the United States are taxes placed on the sale or lease of goods and services in the United States. Sales tax is governed at the state level and no national general sales tax exists. 45 states, the District of Columbia, the territories of Puerto Rico, and Guam impose general sales taxes that apply to the sale or lease of most goods and some services, and states also may levy selective sales taxes on the sale or lease of particular goods or services. States may grant local governments the authority to impose additional general or selective sales taxes.

Rental value is the fair market value of property while rented out in a lease. More generally, it may be the consideration paid under the lease for the right to occupy, or the royalties or return received by a lessor (landlord) under a license to real property. In the science and art of appraisal, it is the amount that would be paid for rental of similar real property in the same condition and in the same area.

Cultural property, also known as cultural patrimony, comprises the physical items that are part of the cultural heritage of a group or society, as opposed to less tangible cultural expressions. They include such items as cultural landscapes, historic buildings, works of art, archaeological sites, as well as collections of libraries, archives, and museums.

Digital goods are software programs, music, videos or other electronic files that users download exclusively from the Internet. Some digital goods are free, others are available for a fee. The taxation of digital goods and/or services, sometimes referred to as digital tax and/or a digital services tax, is gaining popularity across the globe.

A Cultural Property is administered by the Japanese government's Agency for Cultural Affairs, and includes tangible properties ; intangible properties ; folk properties both tangible and intangible; monuments historic, scenic and natural; cultural landscapes; and groups of traditional buildings. Buried properties and conservation techniques are also protected. Together these cultural properties are to be preserved and utilized as the heritage of the Japanese people.

A Tangible Cultural Property as defined by the Japanese government's Law for the Protection of Cultural Properties is a part of the Cultural Properties of high historical or artistic value such as structures, paintings, sculptures, handicrafts, calligraphic works, ancient books, historic documents, archeological artifacts and other such items created in Japan. All objects which are not structures are called "works of fine arts and crafts.

Hunter v Moss [1994] 1 WLR 452 is an English trusts law case from the Court of Appeal concerning the certainty of subject matter necessary to form a trust. Moss promised Hunter 50 shares in his company as part of an employment contract, but failed to provide them. Hunter brought a claim against Moss for them, arguing that Moss's promise had created a trust over those 50 shares. The constitution of trusts normally requires that trust property be segregated from non-trust property for the trust to be valid, as in Re London Wine Co (Shippers) Ltd. On this occasion, however, both Colin Rimer in the High Court of Justice and Dillon, Mann and Hirst LJJ in the Court of Appeal felt that, because this case dealt with intangible rather than tangible property, this rule did not have to be applied. Because all the shares were identical, it did not matter that they were not segregated, and the trust was valid. The decision was applied in Re Harvard Securities, creating a rule that segregation is not always necessary when the trust concerns intangible, identical property.

Massachusetts Question 3, filed under the name, the 3 percent Sales Tax Relief Act, appears on the November 2, 2010 ballot in the state of Massachusetts as an initiative. The measure, if enacted by voters, would reduce the state sales tax rate from 6.25 to 3 percent. The measure is being sponsored by the Alliance to Roll Back Taxes headed by Carla Howell. The measure would be enacted into a law 30 days after the election if approved by voters.