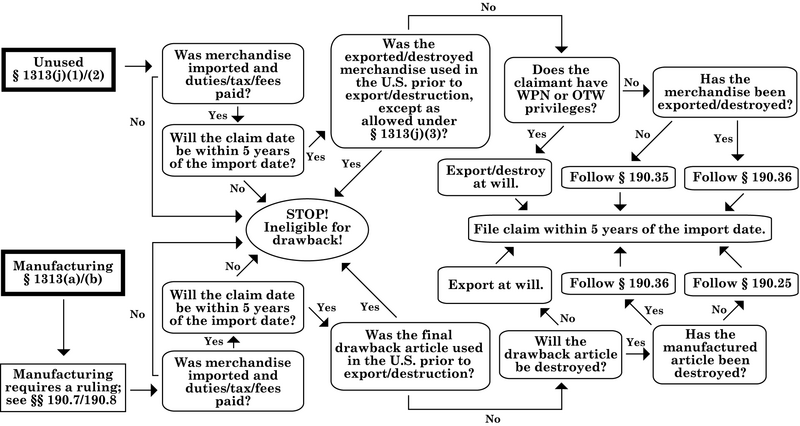

General drawback claim flow for unused and manufacturing claims

Duty drawback is the oldest trade program in the United States and was codified in 1789.[ citation needed ] Drawback is the refund of duties, certain taxes, and certain fees collected upon the importation of merchandise into the United States. Drawback refunds are only allowed upon the export/destruction of the imported merchandise or a valid substitute, or the export/destruction of a certain article manufactured from the imported merchandise or a valid substitute. Claimants may be the importer, exporter, or intermediate party within the drawback transaction.

Claimants can recover the following duties, taxes and fees paid on the imported merchandise:

Claims are filed in accordance with the requirements in 19 C.F.R. Part 190 and the generalized instructions in the ACE Business Rules and Process Document found on CBP.gov.

Claims filed under 19 U.S.C. 1313(d) must be filed within 3 years from the date of export of the manufactured article. NAFTA claims are subject to the time frames in 19 C.F.R. Part 181. All other claims must be filed within 5 years from the date of import of the imported merchandise.

All claims must be filed electronically with CBP through the Automated Broker Interface (ABI). Paper claims are not accepted, and electronic claims may not be submitted through an ACE portal account. Claimants are required to electronically transmit the claim data defined in the drawback CATAIR, which can be found on CBP.gov.

Claimants may file a claim in one of three ways:

Service providers, and software vendors can be found on CBP.gov.

Upon acceptance by CBP, the claim will be automatically routed to a CBP Center of Excellence and Expertise (CEE) for processing according to the claimant's importer number included within the claim. CEE drawback offices are located at Newark/New York, Houston, Chicago, Detroit, and San Francisco.

Privileges. CBP allows three “privileges” that enhance drawback claim processing:

Claimants must submit an application for a privilege which must be approved by a drawback office before a privilege can be invoked on a claim. Claimants may use either the generic privilege application sample found on CBP.gov or submit an application in letter format that includes the data elements defined in the specific regulation. Privilege applications should be emailed to the drawback office that will process the claim if known; else email to the closest drawback office and it will be routed by CBP accordingly.

Manufacturing Rulings for Claims Filed Under 19 U.S.C. 1313(a)/(b). Claimants who use imported merchandise, or a valid substitute, to manufacture a drawback article for export/destruction must have a ruling prior to being approved for a drawback payment. CBP has pre-approved several common manufacturing processes as “general” rulings (found in Appendix A of 19 C.F.R. 190) that any claimant may use provided their manufacturing process falls within the manufacturing process described therein. If a claimant's manufacturing process does not meet the requirements of a general ruling, they must request a specific ruling from CBP Headquarters per 19 C.F.R. 190.8.

General ruling applications should be emailed to the drawback office that will process the claim if known; else email to the closest drawback office and it will be routed by CBP accordingly. Specific ruling applications should be emailed to the drawback section of Regulations and Rulings.

Claimants may file a drawback claim utilizing provisional ruling number 99-99999-999 while waiting for a ruling approval, but in such cases, CBP will not pay drawback or accelerated payment until a claimant's ruling request has been approved.

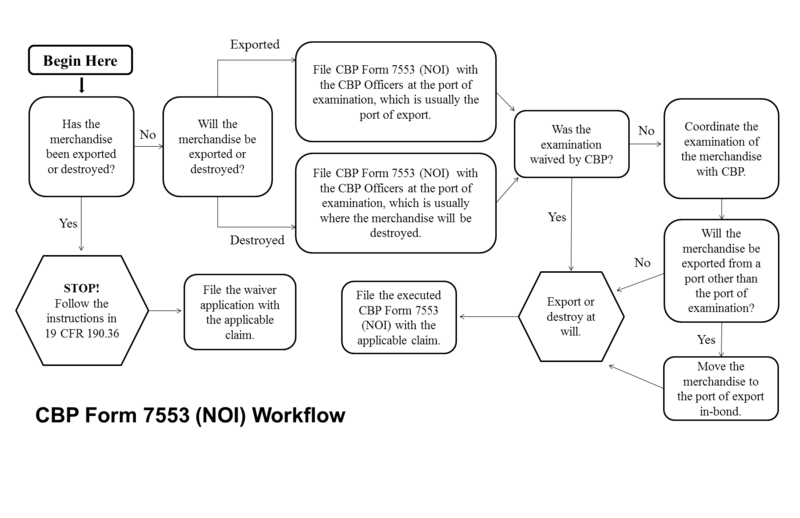

Notice of Intent to Export or Destroy (NOI). Per 19 C.F.R. 190.35, exporters are required to notify CBP prior to the export of unused or rejected merchandise subject to drawback. Notification is made by submitting CBP Form 7553 to the CBP office of examination, which is usually the port of export. Once the requirements of the NOI have been met, the merchandise may be exported, and the executed Form 7553 is included with the drawback claim. The requirements in 19 C.F.R. 190.35 may be waived per the conditions outlined in 19 C.F.R. 190.36 or 19 C.F.R. 190.91.

For merchandise that will be destroyed, an NOI must be submitted to CBP prior to destruction per the requirements in 19 C.F.R. 190.71. Notification is made by submitting CBP Form 7553 to the CBP office of examination, which is usually the port where the destruction will occur. Should CBP decline to witness a destruction, the merchandise must be destroyed by a disinterested third party and the third party must provide the proof of destruction.

The executed NOI (the process is complete, and the NOI has been signed by the CBP Officer) is uploaded into the Document Image System (DIS) at the time of claim filing.

Bonding. A drawback claim does not require a bond unless the claimant has been approved for AP privileges and is requesting AP on the claim. In such cases, a 1A drawback bond must be included with the claim in an amount not less than the AP. All bonds must be filed in eBond .

Payment. Unless approved for AP, an approved drawback payment will usually be issued between one and three years after the claim date. The only predictable payment is AP, and approved AP will usually occur within three weeks of the AP request acceptance date.

Technical Assistance. Filing error status codes may be researched in the Drawback Error Dictionary found on CBP.gov. CBP has personnel dedicated to assisting filers successfully transmit their claims: claimants may contact an ABI rep by sending an email to clientrepoutreach@cbp.dhs.gov.

Drawback on merchandise exported to Canada or Mexico subject to NAFTA can be claimed per the guidance in 19 C.F.R. 181. Unused merchandise that is exported in the same condition as imported may be filed under 19 U.S.C. 1313(j)(1) and 19 C.F.R. 190. Claims under NAFTA may be filed on merchandise entered into the U.S. on or before June 30, 2020. Claims under 19 U.S.C. 1313(c) retail returns substitution may not be filed under NAFTA; retail returns direct identification are allowed.

Drawback on merchandise exported to Canada or Mexico subject to USMCA can be claimed per the guidance in 19 C.F.R. 182. Unused merchandise that is exported in the same condition as imported may be filed under 19 U.S.C. 1313(j)(1) and 19 C.F.R. 190. Claims under USMCA may be filed on merchandise entered into the U.S. on or after July 1, 2020.

Exports to Chile are no longer eligible for drawback unless filed under 19 U.S.C. 1313(j)(1) and the merchandise has not changed in condition. Additional information can be found on CBP.gov.

On February 24, 2015, drawback law was updated via “The Trade Facilitation and Trade Enforcement Act of 2015” (TFTEA) which modernized the drawback statutes and regulations. The final rule was published in the Federal Register on December 18, 2018.

The United States of America has separate federal, state, and local governments with taxes imposed at each of these levels. Taxes are levied on income, payroll, property, sales, capital gains, dividends, imports, estates and gifts, as well as various fees. In 2020, taxes collected by federal, state, and local governments amounted to 25.5% of GDP, below the OECD average of 33.5% of GDP.

United States Customs and Border Protection (CBP) is the largest federal law enforcement agency of the United States Department of Homeland Security. It is the country's primary border control organization, charged with regulating and facilitating international trade, collecting import duties, as well as enforcing U.S. regulations, including trade, customs and immigration. CBP is one of the largest law enforcement agencies in the United States. It has a workforce of more than 45,600 federal agents and officers. It is headquartered in Washington, D.C.

Country of origin (CO) represents the country or countries of manufacture, production, design, or brand origin where an article or product comes from. For multinational brands, CO may include multiple countries within the value-creation process.

A Federal Firearms License (FFL) is a license in the United States that enables an individual or a company to engage in a business pertaining to the manufacture or importation of firearms and ammunition, or the interstate and intrastate sale of firearms. Holding an FFL to engage in certain such activities has been a legal requirement within the United States since the enactment of the Gun Control Act of 1968. The FFL is issued by the Bureau of Alcohol, Tobacco, Firearms, and Explosives

A bonded warehouse, or bond, is a building or other secured area in which dutiable goods may be stored, manipulated, or undergo manufacturing operations without payment of duty. It may be managed by the state or by private enterprise. In the latter case a customs bond must be posted with the government. This system is widely used in developed countries throughout the world.

A freight forwarder, or forwarding agent, is a person or a company who, for a fee, organizes shipments for the shipper by liaising with carriers. A forwarder does not move the goods but acts as an agent in the logistics network.

Custom brokers or Customs House Brokerages are working positions that may be employed by or affiliated with freight forwarders, independent businesses, or shipping lines, importers, exporters, trade authorities, and customs brokerage firms.

An import is the receiving country in an export from the sending country. Importation and exportation are the defining financial transactions of international trade.

Richardson v. Perales, 402 U.S. 389 (1971), was a case heard by the United States Supreme Court to determine and delineate several questions concerning administrative procedure in Social Security disability cases. Among the questions considered was the propriety of using physicians' written reports generated from medical examinations of a disability claimant, and whether these could constitute "substantial evidence" supportive of finding nondisability under the Social Security Act.

In 1789, Alexander Hamilton, the Secretary of the Treasury, calculated that the United States required $3 million a year for operating expenses as well as enough revenue to repay the estimated $75 million in foreign and domestic debt. Under the rates established by the Tariff of 1789, the government could not meet its obligations. Consequently, Hamilton proposed an increase in the average rate from 5 percent to between 7 and 10 percent, the addition of numerous items to the list, and the passage of an excise tax. Congress refused to pass the excise tax, but James Madison successfully steered the tariff increases through the legislature.

In the United States, a foreign-trade zone (FTZ) is a geographical area, in a United States Port of Entry, where commercial merchandise, both domestic and foreign, receives the same Customs treatment it would if it were outside the commerce of the United States. The purpose of such zones is to help American businesses to be competitive in the global economy by reducing tariff burdens on the importation of foreign inputs and on exported finished products. Another definition of an FTZ states that it is an isolated, enclosed and policed area operated as a public utility, furnished with facilities for loading, unloading, handling, storing, manipulating, manufacturing and exhibiting goods and for reshipping them by land, water or air. Merchandise of every description may be held in the zone without being subject to tariffs and other ad valorem taxes. This tariff and tax relief is designed to lower the costs of U.S.-based operations engaged in international trade and thereby create and retain the employment and capital investment opportunities that result from those operations.

The Consumer Product Safety Improvement Act (CPSIA) of 2008 is a United States law signed on August 14, 2008 by President George W. Bush. The legislative bill was known as HR 4040, sponsored by Congressman Bobby Rush (D-Ill.). On December 19, 2007, the U.S. House approved the bill 407-0. On March 6, 2008, the U.S. Senate approved the bill 79-13. The law—public law 110-314—increases the budget of the Consumer Product Safety Commission (CPSC), imposes new testing and documentation requirements, and sets new acceptable levels of several substances. It imposes new requirements on manufacturers of apparel, shoes, personal care products, accessories and jewelry, home furnishings, bedding, toys, electronics and video games, books, school supplies, educational materials and science kits. The Act also increases fines and specifies jail time for some violations.

The Importer Security Filing (ISF) also referred to as 10+2, is a customs import requirement of the United States Customs and Border Protection (CBP) ; which requires containerized cargo information, for security purposes, to be transmitted to the agency at least 24 hours (19 CFR section 149.2 before goods are loaded onto an ocean vessel headed to the U.S. for shipment into the U.S. 10+2 is pursuant to section 203 of the SAFE Port Act, and requires importers to provide 10 data elements to CBP, as well as 2 more data documents from the carrier.

The United States Customs Modernization Act, amended title 19 U.S.C. 1508, 1509 and 1510, formally Title VI of the North American Free Trade Agreement Implementation Act, commonly known as the "Mod Act", amended the Tariff Act of 1930 and related laws.

The United States imposes tariffs on imports of goods. The duty is levied at the time of import and is paid by the importer of record. Customs duties vary by country of origin and product. Goods from many countries are exempt from duty under various trade agreements. Certain types of goods are exempt from duty regardless of source. Customs rules differ from other import restrictions. Failure to properly comply with customs rules can result in seizure of goods and criminal penalties against involved parties. The United States Customs and Border Protection (CBP) enforces customs rules.

The Board of Veterans' Appeals (BVA) is an administrative tribunal within the United States Department of Veterans Affairs (VA), located in Washington, D.C. Established by Executive Order on July 28, 1933, it determines whether U.S. military veterans are entitled to claimed veterans' benefits and services. The Board's mission is to conduct hearings and decide appeals properly before the Board in a timely manner. The Board's jurisdiction extends to all questions in matters involving a decision by the Secretary under a law that affects a provision of benefits by the Secretary to Veterans, their dependents, or their Survivors. Final decision on such appeals are made by the Board based on the entire record in the proceedings and upon consideration of all evidence and applicable provisions of law and regulation. The Board's review is de novo.

CFR Title 9 – Animals and Animal Products is one of 50 titles composing the United States Code of Federal Regulations (CFR) and contains the principal set of rules and regulations issued by federal agencies regarding animals and animal products. It is available in digital and printed form and can be referenced online using the Electronic Code of Federal Regulations (e-CFR).

Customs rulings are binding administrative decisions issued by U.S. Customs and Border Protection (CBP) pursuant to 19 C.F.R. Part 177. Rulings may address customs related matters, including United States tariff classification, marking, and valuation. CBP may issue such rulings to any importer or exporter of merchandise; to any individual or business entity that has a direct and demonstrable interest in the matters or questions presented in the ruling request; or to an agent of either of the aforementioned parties. Rulings may only be prospective and in response to a ruling request.

A customs declaration is a form that lists the details of goods that are being imported or exported when a citizen or visitor enters a customs territory. Most countries require travellers to complete a customs declaration form when bringing notified goods across international borders. Posting items via international mail also requires the sending party to complete a customs declaration form.

The Convention on Cultural Property Implementation Act is a United States Act of Congress that became federal law in 1983. The CCPIA implemented the 1970 UNESCO Convention on the Means of Prohibiting and Preventing the Illicit Import, Export and Transfer of Ownership of Cultural Property. It restricts the importation of some archaeological and ethnological materials into the United States from other State Parties to the Convention.

U.S. Statutory Reference: 19 U.S.C. 1313

U.S. Regulatory Reference (TFTEA): 19 C.F.R. Part 190 (supersedes 19 C.F.R. Part 191)

Drawback filing instructions at CBP.gov

Customs Rulings Online ; include the term 'drawback' in the search field.