20,000 (1935) and declined to less than 500 (1950)

The Home Owners' Loan Corporation (HOLC) was a government-sponsored corporation created as part of the New Deal. The corporation was established in 1933 by the Home Owners' Loan Corporation Act under the leadership of President Franklin D. Roosevelt.[2] Its purpose was to refinance home mortgages currently in default to prevent foreclosure, as well as to expand home buying opportunities.

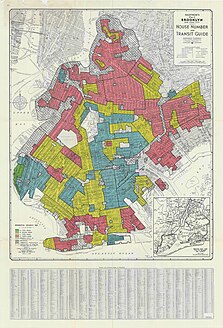

The HOLC created a housing appraisal system of color-coded maps that categorized the riskiness of lending to households in different neighborhoods. While the maps relied on various housing and economic measures, they also used demographic information (such as the racial, ethnic, and immigrant composition of neighborhoods) to categorize creditworthiness.[3] Since Kenneth T. Jackson's work in the 1980s, a number of studies have found that HOLC was a key promoter of redlining and a driver of racial residential segregation and racial wealth inequality in the United States.[4][5][3]

Organizational history

HOLC was established as an emergency agency under Federal Home Loan Bank Board (FHLBB) supervision by the Home Owners' Loan Act of 1933, June 13, 1933.[6] It was transferred with FHLBB and its components to the Federal Loan Agency by Reorganization Plan No. I of 1939, effective July 1, 1939. It was assigned with other components of abolished FHLBB to the Federal Home Loan Bank Administration (FHLBA), National Housing Agency, by EO 9070, February 24, 1942. Its board of directors was abolished by Reorganization Plan No. 3 of 1947, effective July 27, 1947, and HOLC was assigned, for purposes of liquidation, to the Home Loan Bank Board within the Housing and Home Finance Agency. It was terminated by order of Home Loan Bank Board Secretary, effective February 3, 1954, pursuant to an act of June 30, 1953 (67Stat.121).

Operations

The HOLC issued bonds and then used the bonds to purchase mortgage loans from lenders. The loans purchased were for homeowners who were having problems making the payments on their mortgage loans "through no fault of their own". The HOLC refinanced the loans for the borrowers. Many of the lenders gained from selling the loans because the HOLC bought the loans by offering a value of bonds equal to the amount of principal owed by the borrower, plus unpaid interest on the loan, plus taxes that the lender paid on the property. This value of the loan was the amount of the loan that was refinanced for the borrower. The borrower gained because they were offered a loan with a longer time frame at a lower interest rate. It was rare to reduce the amount of principal owed.

Loan repayments and foreclosure policies

Between 1933 and 1935, the HOLC made slightly more than one million loans. At that point it stopped making new loans and then focused on the repayments of the loans. The typical borrower whose loan was refinanced by the HOLC was more than 2 years behind on payments of the loan and more than 2 years behind on making tax payments on the property. The HOLC eventually foreclosed on 20 percent of the loans that it refinanced. It tended to wait until the borrower had failed to make payments on the loan for more than a year before it foreclosed on the loan. When the HOLC foreclosed, it typically refurbished the home. In many cases it rented out the home until it could be resold. The HOLC tried to avoid selling too many homes quickly to avoid having negative effects on housing prices. Ultimately, more than 800,000 people repaid their HOLC loans, and many repaid them on time.[7][8] HOLC officially ceased operations in 1951, when its last assets were sold to private lenders. HOLC was only applicable to nonfarm homes, worth less than $20,000. HOLC also assisted mortgage lenders by refinancing problematic loans and increasing the institutions' liquidity. When its last assets were sold in 1951, HOLC turned a small profit.[9][10]

HOLC is often cited as the originator of mortgage redlining.[11][12]HOLC maps[13] generated during the 1930s to assess credit-worthiness were color-coded by mortgage security risk, with majority African-American areas disproportionately likely to be marked in red indicating designation as "hazardous."[14] These maps were made as part of HOLC's City Survey project that ran from late 1935 until 1940.[15] Perhaps ironically, HOLC had issued refinancing loans to African American homeowners in its initial "rescue" phase before it started making its redlining maps.[16] The racist attitudes and language found in HOLC appraisal sheets and Residential Security Maps created by the HOLC gave federal support to real-estate practices that helped segregate American housing throughout the 20th century.[17]

The effects of redlining, as noted in HOLC maps, endures to the present time. A study released in 2018 found that 74 percent of neighborhoods that HOLC graded as high-risk or "hazardous" are low-to-moderate income neighborhoods today, while 64 percent of the neighborhoods graded "hazardous" are minority neighborhoods today.[18] "It's as if some of these places have been trapped in the past, locking neighborhoods into concentrated poverty," said Jason Richardson, director of research at the NCRC, a consumer advocacy group.[19]

A 2020 study in the American Sociological Review found that HOLC led to substantial and persistent increases in racial residential segregation.[4] A 2021 study in the American Economic Journal found that areas classified as high-risk on HOLC maps became increasingly segregated by race during the next 30–35 years, and suffered long-run declines in home ownership, house values, and credit scores.[20] HOLC's evaluation of neighborhoods in the 1930s correlates with "health, employment, education, and income measures" in these same neighborhoods decades later.[21]

Since the rediscovery of HOLC documents in the 1980s, there has been considerable debate about the exact role of HOLC and its maps in redlining: even as the neighborhood evaluations largely align with race and with ongoing disparities, it is unclear exactly how much of an effect HOLC itself had.[22] According to a paper by economic historian Price V. Fishback and three co-authors, issued in 2021,[23] the blame placed on HOLC is misplaced. Far from "ironically" issuing a few loans to African-Americans in an "initial phase" and then becoming a major promoter of redlining, HOLC actually refinanced mortgage loans for African-Americans in near proportion to the share of African-American homeowners.[neutrality is disputed] The pattern of loans had basically no relationship to the "redlining" maps because the program to create the maps did not even begin until after 90% of HOLC refinancing agreements had already been concluded.[neutrality is disputed]

However, the HOLC shared their maps with the other major New Deal housing program, the Federal Housing Administration. But, the FHA already had its own discriminatory program of systematically rating urban neighborhoods and the HOLC used the FHA's discriminatory guidelines for its maps.[24]

As for private lenders, though Kenneth T. Jackson's claim that they relied on the HOLC's maps to implement their own discriminatory practices has been widely repeated, the evidence is weak that private lenders even had access to the maps.[citation needed] By contrast, it is well documented that private lenders understood which neighborhoods the FHA favored and disfavored; suburban greenfield developers often explicitly advertised the FHA-insurability of their properties in ads for prospective buyers. Redlining was an established practice in the real estate industry before the federal government had any significant role in it; to the extent that any federal agency is to blame for perpetuating the practice, it is the Federal Housing Administration and not the Home Owners' Loan Corporation.[25][23]

↑ Fishback, Price; Rose, Jonathan; Snowden, Kenneth (October 2013). Well Worth Saving: How the New Deal Safeguarded Home Ownership (1sted.). Chicago: University of Chicago Press. ISBN978-0226082448.

↑ Connolly, N. D. B.; Winling, LaDale; Nelson, Robert K.; Marciano, Richard (2018-01-19), "Mapping inequality", The Routledge Companion to Spatial History, Routledge, pp.502–524, doi:10.4324/9781315099781-29, ISBN9781315099781

↑ Freund, David M.P. (2007). Colored Property: State Policy and White Racial Politics in Suburban America. Chicago: University of Chicago Press. ISBN978-0-226-26276-5.

↑ White, Anna G.; Guikema, Seth D.; Logan, Tom M. (July 2021). "Urban population characteristics and their correlation with historic discriminatory housing practices". Applied Geography. 132: 102445. doi:10.1016/j.apgeog.2021.102445. S2CID236261789.

Brennana, John F. "The Impact of Depression-era Homeowners' Loan Corporation Lending in Greater Cleveland, Ohio," Urban Geography, (2015) 36#1 pp: 1-28.

Price Fishback, Jonathan Rose, and Kenneth Snowden, Well Worth Saving: How the New Deal Safeguarded Home Ownership. Chicago: University of Chicago Press, 2013.

The Federal Housing Administration (FHA), also known as the Office of Housing within the Department of Housing and Urban Development (HUD), is a United States government agency founded by President Franklin Delano Roosevelt, established in part by the National Housing Act of 1934. Its primary function is to provide insurance for mortgages originated by private lenders for various types of properties, including single-family homes, multifamily rental properties, hospitals, and residential care facilities. FHA mortgage insurance serves to safeguard these private lenders from financial losses. In the event that a property owner defaults on their mortgage, FHA steps in to compensate the lender for the outstanding principal balance.

Redlining is a discriminatory practice in which financial services are withheld from neighborhoods that have significant numbers of racial and ethnic minorities. Redlining has been most prominent in the United States, and has mostly been directed against African-Americans. The most common examples involve denial of credit and insurance, denial of healthcare, and the development of food deserts in minority neighborhoods.

Refinancing is the replacement of an existing debt obligation with another debt obligation under a different term and interest rate. The terms and conditions of refinancing may vary widely by country, province, or state, based on several economic factors such as inherent risk, projected risk, political stability of a nation, currency stability, banking regulations, borrower's credit worthiness, and credit rating of a nation. In many industrialized nations, common forms of refinancing include primary residence mortgages and car loans.

An FHA insured loan is a US Federal Housing Administration mortgage insurance backed mortgage loan that is provided by an FHA-approved lender. FHA mortgage insurance protects lenders against losses. They have historically allowed lower-income Americans to borrow money to purchase a home that they would not otherwise be able to afford. Because this type of loan is more geared towards new house owners than real estate investors, FHA loans are different from conventional loans in the sense that the house must be owner-occupant for at least a year. Since loans with lower down-payments usually involve more risk to the lender, the home-buyer must pay a two-part mortgage insurance that involves a one-time bulk payment and a monthly payment to compensate for the increased risk. Frequently, individuals "refinance" or replace their FHA loan to remove their monthly mortgage insurance premium. Removing mortgage insurance premium by paying down the loan has become more difficult with FHA loans as of 2013.

The Federal Home Loan Bank Board (FHLBB) was a board created in 1932 that governed the Federal Home Loan Banks also created by the act, the Federal Savings and Loan Insurance Corporation (FSLIC) and nationally-chartered thrifts. It was abolished and superseded by the Federal Housing Finance Board and the Office of Thrift Supervision in 1989 due to the savings and loan crisis of the 1980s, as Federal Home Loan Banks gave favorable lending to the thrifts it regulated leading to regulatory capture.

Blockbusting is a business practice in the United States in which real estate agents and building developers convinced residents in a particular area to sell their property at below-market prices. This was achieved by fearmongering the homeowners, telling them that racial minorities would soon be moving into their neighborhoods. The blockbusters would then sell those same houses at inflated prices to black families seeking upward mobility. Blockbusting became prominent after post-World War II bans on explicitly segregationist real estate practices. By the 1980s it had mostly disappeared in the United States after changes to the law and real estate market.

The Home Mortgage Disclosure Act is a United States federal law that requires certain financial institutions to provide mortgage data to the public. Congress enacted HMDA in 1975.

Homer Hoyt was an American economist known for his pioneering work in land use planning, zoning, and real estate economics. He conducted notable research on land economics and developed an influential approach to the analysis of neighborhoods and housing markets. His sector model of land use was influential in urban planning for several decades. His legacy is controversial today, due to his prominent role in the development and justification of racially segregated housing policy and redlining in American cities.

Mortgage discrimination or mortgage lending discrimination is the practice of banks, governments or other lending institutions denying loans to one or more groups of people primarily on the basis of race, ethnic origin, sex or religion.

In the United States, housing segregation is the practice of denying African Americans and other minority groups equal access to housing through the process of misinformation, denial of realty and financing services, and racial steering. Housing policy in the United States has influenced housing segregation trends throughout history. Key legislation include the National Housing Act of 1934, the G.I. Bill, and the Fair Housing Act. Factors such as socioeconomic status, spatial assimilation, and immigration contribute to perpetuating housing segregation. The effects of housing segregation include relocation, unequal living standards, and poverty. However, there have been initiatives to combat housing segregation, such as the Section 8 housing program.

The United States Housing and Economic Recovery Act of 2008 was designed primarily to address the subprime mortgage crisis. It authorized the Federal Housing Administration to guarantee up to $300 billion in new 30-year fixed rate mortgages for subprime borrowers if lenders wrote down principal loan balances to 90 percent of current appraisal value. It was intended to restore confidence in Fannie Mae and Freddie Mac by strengthening regulations and injecting capital into the two large U.S. suppliers of mortgage funding. States are authorized to refinance subprime loans using mortgage revenue bonds. Enactment of the Act led to the government conservatorship of Fannie Mae and Freddie Mac.

The Homeowners Refinancing Act was an Act of Congress of the United States passed as part of Franklin Delano Roosevelt's New Deal during the Great Depression to help those in danger of losing their homes. The act, which went into effect on June 13, 1933, provided mortgage assistance to homeowners or would-be homeowners by providing them money or refinancing mortgages.

Loan modification is the systematic alteration of mortgage loan agreements that help those having problems making the payments by reducing interest rates, monthly payments or principal balances. Lending institutions could make one or more of these changes to relieve financial pressure on borrowers to prevent the condition of foreclosure. Loan modifications have been practiced in the United States since the 1930s. During the Great Depression, loan modification programs took place at the state level in an effort to reduce levels of loan foreclosures.

Housing inequality is a disparity in the quality of housing in a society which is a form of economic inequality. The right to housing is recognized by many national constitutions, and the lack of adequate housing can have adverse consequences for an individual or a family. The term may apply regionally, temporally or culturally. Housing inequality is directly related to racial, social, income and wealth inequality. It is often the result of market forces, discrimination and segregation.

Housing discrimination in the United States refers to the historical and current barriers, policies, and biases that prevent equitable access to housing. Housing discrimination became more pronounced after the abolition of slavery in 1865, typically as part of Jim Crow laws that enforced racial segregation. The federal government didn't begin to take action against these laws until 1917, when the Supreme Court struck down ordinances prohibiting blacks from occupying or owning buildings in majority-white neighborhoods in Buchanan v. Warley. However, the federal government as well as local governments continued to be directly responsible for housing discrimination through redlining and race-restricted covenants until the Civil Rights Act of 1968.

The National Mortgage Crisis of the 1930s was a Depression-era crisis in the United States characterized by high-default rates and soaring loan-to-value ratios in the residential housing market. Rapid expansion in the residential non-farm housing market through the 1920s created a housing bubble inflated in part by ad hoc innovation on the part of the four primary financial intermediaries – commercial banks, life insurance companies, mutual savings banks, and Building & Loans (thrifts). As a result, the federal overhaul stemming from New Deal legislation gave rise to a paradigmatic shift in mortgage lending, popularizing longer-term maturity, fully amortizing mortgages and creating a thick secondary market for mortgage-related securities.

The Detroit Eight Mile Wall, also referred to as Detroit's Wailing Wall, Berlin Wall or The Birwood Wall, is a one-foot-thick (0.30 m), six-foot-high (1.8 m) separation wall that stretches about 1⁄2 mile (0.80 km) in length. 1 foot is buried in the ground and the remaining 5 feet is visible to the community. It was constructed in 1941 to physically separate black and white homeowners on the sole basis of race. The wall no longer serves to racially segregate homeowners and, as of 1971, both sides of the barrier have been predominantly black.

The Contract Buyers League (CBL) was a grassroots organization formed in 1968 by residents of North Lawndale, a Chicago, Illinois community. The CBL was founded in order to address the exploitative practices of predatory land contracts in African American communities. The organization played a significant role in raising awareness about the issue and advocating for fair and affordable housing rights. Assisted by Jack Macnamara, a Jesuit seminarian, and twelve white college students based at Presentation Catholic Church, led by Msgr. John "Jack" Egan, the CBL fought the discriminatory real estate practice known as “contract selling.”

Ghettos in the United States are typically urban neighborhoods perceived as being high in crime and poverty. The origins of these areas are specific to the United States and its laws, which created ghettos through both legislation and private efforts to segregate America for political, economic, social, and ideological reasons: de jure and de facto segregation. De facto segregation continues today in ways such as residential segregation and school segregation because of contemporary behavior and the historical legacy of de jure segregation.

Eight Mile-Wyoming area is located nearly 10 miles (16 km) from Paradise Valley on the northern boundary of Detroit and minimally resembled inner-city neighborhoods. Originally settled in the 1920s by thousands of optimistic migrant farmers, the area became a settlement opportunity for Blacks to construct and own their own homes. The area was fought over for development and housing projects for decades and represented an isolated concentration of Blacks in a vast population of whites.

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.