The United States of America has separate federal, state, and local governments with taxes imposed at each of these levels. Taxes are levied on income, payroll, property, sales, capital gains, dividends, imports, estates and gifts, as well as various fees. In 2010, taxes collected by federal, state, and municipal governments amounted to 24.8% of GDP. In the OECD, only Chile and Mexico are taxed less as a share of their GDP.

In the United States, a 401(k) plan is the tax-qualified, defined-contribution pension account defined in subsection 401(k) of the Internal Revenue Code. Under the plan, retirement savings contributions are provided by an employer, deducted from the employee's paycheck before taxation, and limited to a maximum pre-tax annual contribution of $19,000.

An income tax is a tax imposed on individuals or entities (taxpayers) that varies with respective income or profits. Income tax generally is computed as the product of a tax rate times taxable income. Taxation rates may vary by type or characteristics of the taxpayer.

In accounting, revenue is the income that a business has from its normal business activities, usually from the sale of goods and services to customers. Revenue is also referred to as sales or turnover. Some companies receive revenue from interest, royalties, or other fees. Revenue may refer to business income in general, or it may refer to the amount, in a monetary unit, earned during a period of time, as in "Last year, Company X had revenue of $42 million". Profits or net income generally imply total revenue minus total expenses in a given period. In accounting, in the balance statement it is a subsection of the Equity section and revenue increases equity, it is often referred to as the "top line" due to its position on the income statement at the very top. This is to be contrasted with the "bottom line" which denotes net income.

A taxpayer is a person or organization subject to pay a tax. Taxpayers have an Identification Number, a reference number issued by a government to its citizens.

The Canada Revenue Agency, known as the Canada Customs and Revenue Agency previously and as Revenue Canada before that, is a Canadian federal agency that administers tax laws for the Government of Canada and for most provinces and territories, international trade legislation, and various social and economic benefit and incentive programs delivered through the tax system. It also oversees the registration of charities in Canada, and tax credit programmes such as the Scientific Research and Experimental Development Tax Credit Program.

A withholding tax, or a retention tax, is an income tax to be paid to the government by the payer of the income rather than by the recipient of the income. The tax is thus withheld or deducted from the income due to the recipient. In most jurisdictions, withholding tax applies to employment income. Many jurisdictions also require withholding tax on payments of interest or dividends. In most jurisdictions, there are additional withholding tax obligations if the recipient of the income is resident in a different jurisdiction, and in those circumstances withholding tax sometimes applies to royalties, rent or even the sale of real estate. Governments use withholding tax as a means to combat tax evasion, and sometimes impose additional withholding tax requirements if the recipient has been delinquent in filing tax returns, or in industries where tax evasion is perceived to be common.

Taxation in France is determined by the yearly budget vote by the French Parliament, which determines which kinds of taxes can be levied and which rates can be applied.

Income taxes in the United States are imposed by the federal, most state, and many local governments. The income taxes are determined by applying a tax rate, which may increase as income increases, to taxable income, which is the total income less allowable deductions. Income is broadly defined. Individuals and corporations are directly taxable, and estates and trusts may be taxable on undistributed income. Partnerships are not taxed, but their partners are taxed on their shares of partnership income. Residents and citizens are taxed on worldwide income, while nonresidents are taxed only on income within the jurisdiction. Several types of credits reduce tax, and some types of credits may exceed tax before credits. An alternative tax applies at the federal and some state levels.

Taxes in New Zealand are collected at a national level by the Inland Revenue Department (IRD) on behalf of the Government of New Zealand. National taxes are levied on personal and business income, and on the supply of goods and services. There is no capital gains tax, although certain "gains" such as profits on the sale of patent rights are deemed to be income – income tax does apply to property transactions in certain circumstances, particularly speculation. There are currently no land taxes, but local property taxes (rates) are managed and collected by local authorities. Some goods and services carry a specific tax, referred to as an excise or a duty, such as alcohol excise or gaming duty. These are collected by a range of government agencies such as the New Zealand Customs Service. There is no social security (payroll) tax.

Tax amnesty is a limited-time opportunity for a specified group of taxpayers to pay a defined amount, in exchange for forgiveness of a tax liability relating to a previous tax period or periods and without fear of criminal prosecution. It typically expires when some authority begins a tax investigation of the past-due tax. In some cases, legislation extending amnesty also imposes harsher penalties on those who are eligible for amnesty but do not take it. Tax amnesty is one of voluntary compliance strategies to increase tax base and tax revenue. Tax amnesty is different from other voluntary compliance strategies in part where tax amnesty usually waives the taxpayers' tax liability.

Income taxes in Canada constitute the majority of the annual revenues of the Government of Canada, and of the governments of the Provinces of Canada. In the fiscal year ending 31 March 2018, the federal government collected just over three times more revenue from personal income taxes than it did from corporate income taxes.

Creative real estate investing is any non-traditional method of buying and selling real estate. Confidence tricks and pyramid schemes in the 20th and 21st century such as Nouveau Riche have embraced the term, leading contemporary usage of the term to be synonymous with unscrupulous practices.

Basis, as used in United States tax law, is the original cost of property, adjusted for factors such as depreciation. When property is sold, the taxpayer pays/(saves) taxes on a capital gain/(loss) that equals the amount realized on the sale minus the sold property's basis.

A tax sale is the forced sale of property by a governmental entity for unpaid taxes by the property's owner.

Privatized tax collection occurs wherever the state passes on its obligation to collect taxes to private companies or firms in return for a fixed or ad valorem fee. This contrasts with tax farming where a private individual or organization pays off a pre-determined tax debt, and then subsequently recoups that payment by collecting money from the people within a certain area or business.

Taxes in Indiana are almost entirely authorized at the state level, although the revenue is used to fund both local and state level government. The state of Indiana's income comes from four primary tax areas. Most state level income is from a sales tax of 7% and a flat state income tax of 3.3% with another cut coming in 2017 that will bring the rate down to 3.23%. The state also collects an additional income tax for some counties. Local governments are funded by a property tax that is the sum of rates set by local boards, but the total rate must be approved by the Indiana General Assembly before it can be imposed. Residential property tax rates are capped at maximum of 1% of property value. Excise tax is the fourth form of taxation and is charged on motor vehicles, alcohol, tobacco, gasoline, and certain other forms of movable property; most of the proceeds are used to fund state and local roads and health programs. The Indiana Department of Revenue collects all taxes and pays them out to the appropriate agencies and municipalities. The Indiana Tax Court deals with all tax disputes issues, but decisions can be appealed to the Indiana Supreme Court.

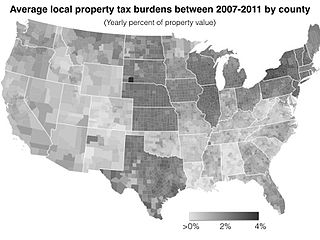

Most local governments in the United States impose a property tax, also known as a millage rate, as a principal source of revenue. This tax may be imposed on real estate or personal property. The tax is nearly always computed as the fair market value of the property times an assessment ratio times a tax rate, and is generally an obligation of the owner of the property. Values are determined by local officials, and may be disputed by property owners. For the taxing authority, one advantage of the property tax over the sales tax or income tax is that the revenue always equals the tax levy, unlike the other taxes. The property tax typically produces the required revenue for municipalities' tax levies. A disadvantage to the taxpayer is that the tax liability is fixed, while the taxpayer's income is not.

President Ulysses S. Grant signed a series of laws during his first and second terms that limited the number of special tax agents and prevented or reduced the collection of delinquent taxes under a commissions or moiety system. The public outcry over the Sanborn incident caused the Grant administration to abolish the practice of appointing special treasury agents to collect commissions or moieties on delinquent taxes.