Related Research Articles

Financial economics is the branch of economics characterized by a "concentration on monetary activities", in which "money of one type or another is likely to appear on both sides of a trade". Its concern is thus the interrelation of financial variables, such as share prices, interest rates and exchange rates, as opposed to those concerning the real economy. It has two main areas of focus: asset pricing and corporate finance; the first being the perspective of providers of capital, i.e. investors, and the second of users of capital. It thus provides the theoretical underpinning for much of finance.

The Black–Scholes or Black–Scholes–Merton model is a mathematical model for the dynamics of a financial market containing derivative investment instruments, using various underlying assumptions. From the parabolic partial differential equation in the model, known as the Black–Scholes equation, one can deduce the Black–Scholes formula, which gives a theoretical estimate of the price of European-style options and shows that the option has a unique price given the risk of the security and its expected return. The equation and model are named after economists Fischer Black and Myron Scholes; Robert C. Merton, who first wrote an academic paper on the subject, is sometimes also credited.

Fischer Sheffey Black was an American economist, best known as one of the authors of the Black–Scholes equation.

Value at risk (VaR) is a measure of the risk of loss of investment/Capital. It estimates how much a set of investments might lose, given normal market conditions, in a set time period such as a day. VaR is typically used by firms and regulators in the financial industry to gauge the amount of assets needed to cover possible losses.

Financial engineering is a multidisciplinary field involving financial theory, methods of engineering, tools of mathematics and the practice of programming. It has also been defined as the application of technical methods, especially from mathematical finance and computational finance, in the practice of finance.

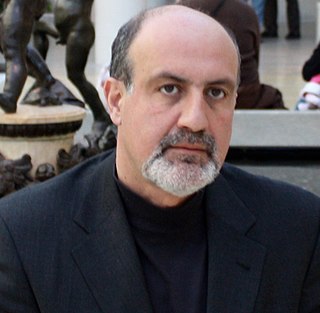

Nassim Nicholas Taleb is a Lebanese-American essayist, mathematical statistician, former option trader, risk analyst, and aphorist whose work concerns problems of randomness, probability, and uncertainty.

In finance, statistical arbitrage is a class of short-term financial trading strategies that employ mean reversion models involving broadly diversified portfolios of securities held for short periods of time. These strategies are supported by substantial mathematical, computational, and trading platforms.

Financial modeling is the task of building an abstract representation of a real world financial situation. This is a mathematical model designed to represent the performance of a financial asset or portfolio of a business, project, or any other investment.

In mathematical finance, the Black–Derman–Toy model (BDT) is a popular short-rate model used in the pricing of bond options, swaptions and other interest rate derivatives; see Lattice model (finance) § Interest rate derivatives. It is a one-factor model; that is, a single stochastic factor—the short rate—determines the future evolution of all interest rates. It was the first model to combine the mean-reverting behaviour of the short rate with the log-normal distribution, and is still widely used.

Emanuel Derman is a South African-born academic, businessman and writer. He is best known as a quantitative analyst, and author of the book My Life as a Quant: Reflections on Physics and Finance.

The following outline is provided as an overview of and topical guide to finance:

A master's degree in quantitative finance concerns the application of mathematical methods to the solution of problems in financial economics. There are several like-titled degrees which may further focus on financial engineering, computational finance, mathematical finance, and/or financial risk management.

In finance, volatility is the degree of variation of a trading price series over time, usually measured by the standard deviation of logarithmic returns.

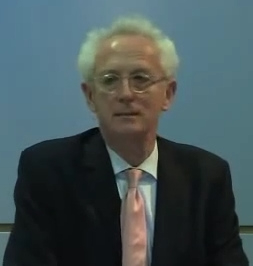

Paul Wilmott is an English researcher, consultant and lecturer in quantitative finance. He is best known as the author of various academic and practitioner texts on risk and derivatives, for Wilmott magazine and Wilmott.com, a quantitative finance portal, and for his prescient warnings about the misuse of mathematics in finance.

In finance, model risk is the risk of loss resulting from using insufficiently accurate models to make decisions, originally and frequently in the context of valuing financial securities. However, model risk is more and more prevalent in activities other than financial securities valuation, such as assigning consumer credit scores, real-time probability prediction of fraudulent credit card transactions, and computing the probability of air flight passenger being a terrorist. Rebonato in 2002 defines model risk as "the risk of occurrence of a significant difference between the mark-to-model value of a complex and/or illiquid instrument, and the price at which the same instrument is revealed to have traded in the market".

Salih Nur Neftçi was a leading expert in the fields of financial markets and financial engineering. He served many advisory roles in national and international financial institutions, and was an active researcher in the fields of finance and financial engineering. Neftçi was an avid and highly regarded educator in mathematical finance who was well known for a lucid and accessible approach towards the field.

Quantitative analysis is the use of mathematical and statistical methods in finance and investment management. Those working in the field are quantitative analysts (quants). Quants tend to specialize in specific areas which may include derivative structuring or pricing, risk management, investment management and other related finance occupations. The occupation is similar to those in industrial mathematics in other industries. The process usually consists of searching vast databases for patterns, such as correlations among liquid assets or price-movement patterns.

Steven "Steve" L. Heston is an American mathematician, economist, and financier. He's also prominently active in the field of gambling-related research, where he sometimes uses the pen name Kim Lee.

Mathematical finance, also known as quantitative finance and financial mathematics, is a field of applied mathematics, concerned with mathematical modeling of financial markets.

References

- ↑ "Financial Models Must Be Clean and Simple", Business Week, December 31, 2008

- ↑ "Financial-Modelers-Manifesto", wilmott.com, January 8, 2009

- ↑ Model Risk

- ↑ The Use, Misuse and Abuse of Mathematics in Finance