The Glass–Steagall legislation describes four provisions of the United States Banking Act of 1933 separating commercial and investment banking. The article 1933 Banking Act describes the entire law, including the legislative history of the provisions covered here.

Banking in the United States began in the late 1790s along with the country's founding and has developed into highly influential and complex system of banking and financial services. Anchored by New York City and Wall Street, it is centered on various financial services namely private banking, asset management, and deposit security.

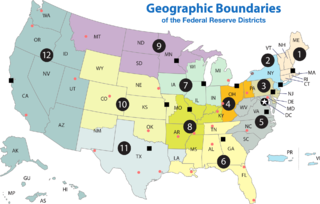

A Federal Reserve Bank is a regional bank of the Federal Reserve System, the central banking system of the United States. There are twelve in total, one for each of the twelve Federal Reserve Districts that were created by the Federal Reserve Act of 1913. The banks are jointly responsible for implementing the monetary policy set forth by the Federal Open Market Committee, and are divided as follows:

A banking license is a legal prerequisite for a financial institution that wants to carry on a banking business. Under the laws of most jurisdictions, a business is not permitted to carry words like a bank, insurance, national in their name, unless it holds a corresponding license. Depending to their banking regulations, jurisdictions may offer different types of banking licenses, such as

An offshore bank is a bank regulated under international banking license, which usually prohibits the bank from establishing any business activities in the jurisdiction of establishment. Due to less regulation and transparency, accounts with offshore banks were often used to hide undeclared income. Since the 1980s, jurisdictions that provide financial services to nonresidents on a big scale, can be referred to as offshore financial centres. Since OFCs often also levy little or no tax corporate and/or personal income and offer, they are often referred to as tax havens.

The savings and loan crisis of the 1980s and 1990s was the failure of 1,043 out of the 3,234 savings and loan associations in the United States from 1986 to 1995: the Federal Savings and Loan Insurance Corporation (FSLIC) closed or otherwise resolved 296 institutions from 1986 to 1989 and the Resolution Trust Corporation (RTC) closed or otherwise resolved 747 institutions from 1989 to 1995.

The reserve requirement is a central bank regulation employed by most, but not all, of the world's central banks, that sets the minimum amount of reserves that must be held by a commercial bank. The minimum reserve is generally determined by the central bank to be no less than a specified percentage of the amount of deposit liabilities the commercial bank owes to its customers. The commercial bank's reserves normally consist of cash owned by the bank and stored physically in the bank vault, plus the amount of the commercial bank's balance in that bank's account with the central bank.

The Community Reinvestment Act is a United States federal law designed to encourage commercial banks and savings associations to help meet the needs of borrowers in all segments of their communities, including low- and moderate-income neighborhoods. Congress passed the Act in 1977 to reduce discriminatory credit practices against low-income neighborhoods, a practice known as redlining.

Bank reserves are a commercial bank's holdings of deposits in accounts with a central bank, plus currency that is physically held in the bank's vault. Some central banks set minimum reserve requirements, which require banks to hold deposits at the central bank equivalent to at least a specified percentage of their liabilities such as customer deposits. Even when there are no reserve requirements, banks often opt to hold some reserves—called desired reserves—against unexpected events such as unusually large net withdrawals by customers or bank runs.

The Banking Act of 1933 was a statute enacted by the United States Congress that established the Federal Deposit Insurance Corporation (FDIC) and imposed various other banking reforms. The entire law is often referred to as the Glass–Steagall Act, after its Congressional sponsors, Senator Carter Glass (D) of Virginia, and Representative Henry B. Steagall (D) of Alabama. The term Glass–Steagall Act, however, is most often used to refer to four provisions of the Banking Act of 1933 that limited commercial bank securities activities and affiliations between commercial banks and securities firms. That limited meaning of the term is described in the article on Glass–Steagall Legislation.

Great Western Bank was a large retail bank that operated primarily in the Western United States. Great Western's headquarters were in Chatsworth, California. At one time, Great Western was one of the largest savings and loan in the nation, second only to Home Savings of America. The bank was acquired by Washington Mutual in 1997 for $6.8 billion.

All regulated financial institutions in the United States are required to file periodic financial and other information with their respective regulators and other parties. For banks in the U.S., one of the key reports required to be filed is the quarterly Consolidated Report of Condition and Income, generally referred to as the call report or RC report. Specifically, every National Bank, State Member Bank and insured Nonmember Bank is required by the Federal Financial Institutions Examination Council (FFIEC) to file a call report as of the close of business on the last day of each calendar quarter, i.e. the report date. The specific reporting requirements depend upon the size of the bank and whether or not it has any foreign offices. Call reports are due no later than 30 days after the end of each calendar quarter. Revisions may be made without prejudice up to 30 days after the initial filing period. Form FFIEC 031 is used for banks with both domestic (U.S.) and foreign (non-U.S.) offices; Form FFIEC 041 is for banks with domestic (U.S.) offices only.

Banner Bank is a Washington-chartered commercial bank headquartered in Walla Walla, Washington, with roots that date back to 1890. The bank provides services in commercial real estate, construction, residential, agricultural and consumer loans. It also provides community banking services through its branches and loan offices located in Washington, Oregon, Idaho and California.

Bank regulation in the United States is highly fragmented compared with other G10 countries, where most countries have only one bank regulator. In the U.S., banking is regulated at both the federal and state level. Depending on the type of charter a banking organization has and on its organizational structure, it may be subject to numerous federal and state banking regulations. Apart from the bank regulatory agencies the U.S. maintains separate securities, commodities, and insurance regulatory agencies at the federal and state level, unlike Japan and the United Kingdom. Bank examiners are generally employed to supervise banks and to ensure compliance with regulations.

A bank is a financial institution that accepts deposits from the public and creates credit. Lending activities can be performed either directly or indirectly through capital markets. Due to their importance in the financial stability of a country, banks are highly regulated in most countries. Most nations have institutionalized a system known as fractional reserve banking under which banks hold liquid assets equal to only a portion of their current liabilities. In addition to other regulations intended to ensure liquidity, banks are generally subject to minimum capital requirements based on an international set of capital standards, known as the Basel Accords.

An alternative financial service (AFS) is a financial service provided outside traditional banking institutions, on which many low-income individuals depend. In developing countries, these services often take the form of microfinance. In developed countries, the services may be similar to those provided by banks and include payday loans, rent-to-own agreements, pawnshops, refund anticipation loans, some subprime mortgage loans and car title loans, and non-bank check cashing, money orders, and money transfers. It also includes traditional moneylending by door-to-door collection. In New York City, these are called check-cashing stores, and they are legally exempted from the 25 percent criminal usury cap.

Gibraltar benefits from an extensive shipping trade, offshore banking, and its position as an international conference center. It is a well known and regulated international finance centre and has been a popular jurisdiction for European offshore companies. The financial sector, tourism, shipping services fees, and duties on consumer goods generate revenue.