A poll tax, also known as head tax or capitation, is a tax levied as a fixed sum on every liable individual, without reference to income or resources. Poll is an archaic term for "head" or "top of the head". The sense of "counting heads" is found in phrases like polling place and opinion poll.

A tax is a compulsory financial charge or some other type of levy imposed on a taxpayer by a governmental organization in order to collectively fund government spending, public expenditures, or as a way to regulate and reduce negative externalities. Tax compliance refers to policy actions and individual behaviour aimed at ensuring that taxpayers are paying the right amount of tax at the right time and securing the correct tax allowances and tax reliefs. The first known taxation took place in Ancient Egypt around 3000–2800 BC. Taxes consist of direct or indirect taxes and may be paid in money or as its labor equivalent.

The Sixteenth Amendment to the United States Constitution allows Congress to levy an income tax without apportioning it among the states on the basis of population. It was passed by Congress in 1909 in response to the 1895 Supreme Court case of Pollock v. Farmers' Loan & Trust Co. The Sixteenth Amendment was ratified by the requisite number of states on February 3, 1913, and effectively overruled the Supreme Court's ruling in Pollock.

The Twenty-fourth Amendment of the United States Constitution prohibits both Congress and the states from conditioning the right to vote in federal elections on payment of a poll tax or other types of tax. The amendment was proposed by Congress to the states on August 27, 1962, and was ratified by the states on January 23, 1964.

Jizya is a per capita yearly taxation historically levied in the form of financial charge on dhimmis, that is, permanent non-Muslim subjects of a state governed by Islamic law. The Quran and hadiths mention jizya without specifying its rate or amount, and the application of jizya varied in the course of Islamic history. However, scholars largely agree that early Muslim rulers adapted existing systems of taxation and tribute that were established under previous rulers of the conquered lands, such as those of the Byzantine and Sasanian empires.

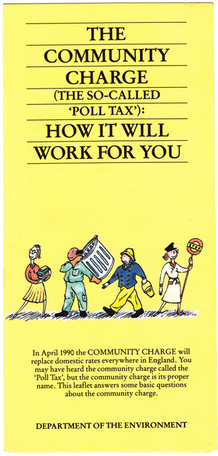

The Community Charge, commonly known as the poll tax, was a system of taxation introduced by Margaret Thatcher's government in replacement of domestic rates in Scotland from 1989, prior to its introduction in England and Wales from 1990. It provided for a single flat-rate, per-capita tax on every adult, at a rate set by the local authority. The charge was replaced by Council Tax in 1993, two years after its abolition was announced.

Corvée is a form of unpaid forced labour that is intermittent in nature, lasting for limited periods of time, typically only a certain number of days' work each year.

This article discusses Chinatowns in Oceania.

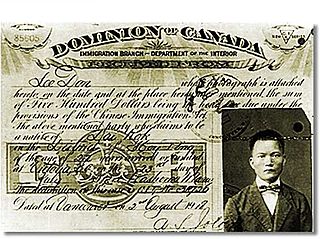

The Chinese Head Tax was a fixed fee charged to each Chinese person entering Canada. The head tax was first levied after the Canadian parliament passed the Chinese Immigration Act of 1885 and it was meant to discourage Chinese people from entering Canada after the completion of the Canadian Pacific Railway (CPR). The tax was abolished by the Chinese Immigration Act of 1923, which outright prevented all Chinese immigration except for that of business people, clergy, educators, students, and some others.

The poll tax riots were a series of riots in British towns and cities during protests against the Community Charge, introduced by the Conservative government of Prime Minister Margaret Thatcher. The largest protest occurred in central London on Saturday 31 March 1990, shortly before the tax was due to come into force in England and Wales.

Although the actual definitions vary between jurisdictions, in general, a direct tax or income tax is a tax imposed upon a person or property as distinct from a tax imposed upon a transaction, which is described as an indirect tax. There is a distinction between direct and indirect tax depending on whether the tax payer is the actual taxpayer or if the amount of tax is supported by a third party, usually a client. The term may be used in economic and political analyses, but does not itself have any legal implications. However, in the United States, the term has special constitutional significance because of a provision in the U.S. Constitution that any direct taxes imposed by the national government be apportioned among the states on the basis of population. In the European Union direct taxation remains the sole responsibility of member states.

Kharāj is a type of individual Islamic tax on agricultural land and its produce, developed under Islamic law.

The Leibzoll was a special toll that Jews had to pay in most European states from the Middle Ages to the 19th century.

Colegrove is a surname that developed in England between the 12th and 15th centuries. The name may have originated from a grove along the River Cole, Wiltshire, a tributary of the River Thames in England. Another explanation as to the origin of the name is from the Middle English cole ‘coal’ + grave ‘pit’, ‘grave’. Other forms of spelling in the past include ‘Colgrove’, ‘Colegrave’, ‘Colgrave’, ‘Coulgrove’. The first records of the Colegrove name were in 14th century England.

New Zealand imposed a poll tax on Chinese immigrants during the 19th and early 20th centuries. The poll tax was effectively lifted in the 1930s following the invasion of China by Japan, and was finally repealed in 1944. Following efforts to recognise its impact, an apology for the tax was issued in English and Mandarin under prime minister Helen Clark in 2002, and was later delivered in Cantonese in 2023.

An excise, or excise tax, is any duty on manufactured goods that is normally levied at the moment of manufacture for internal consumption rather than at sale. Excises are often associated with customs duties, which are levied on pre-existing goods when they cross a designated border in a specific direction; customs are levied on goods that become taxable items at the border, while excise is levied on goods that came into existence inland.

The history of taxation in the United States begins with the colonial protest against British taxation policy in the 1760s, leading to the American Revolution. The independent nation collected taxes on imports ("tariffs"), whiskey, and on glass windows. States and localities collected poll taxes on voters and property taxes on land and commercial buildings. In addition, there were the state and federal excise taxes. State and federal inheritance taxes began after 1900, while the states began collecting sales taxes in the 1930s. The United States imposed income taxes briefly during the Civil War and the 1890s. In 1913, the 16th Amendment was ratified, however, the United States Constitution Article 1, Section 9 defines a direct tax. The Sixteenth Amendment to the United States Constitution did not create a new tax.

Breedlove v. Suttles, 302 U.S. 277 (1937), is an overturned United States Supreme Court decision which upheld the constitutionality of requiring the payment of a poll tax in order to vote in state elections.

The Royal Commission on Chinese Immigration was a commission of inquiry appointed to establish whether or not imposing restrictions to Chinese immigration to Canada was in the country's best interest. Ordered on 4 July 1884 by Prime Minister John A. Macdonald, the inquiry was appointed two commissioners were: the Honorable Joseph-Adolphe Chapleau, LL.D., who was the Secretary of State for Canada; and the Honorable John Hamilton Gray, DCL, a Justice on the Supreme Court of British Columbia.