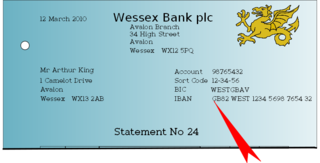

The International Bank Account Number (IBAN) is an internationally agreed upon system of identifying bank accounts across national borders to facilitate the communication and processing of cross border transactions with a reduced risk of transcription errors. An IBAN uniquely identifies the account of a customer at a financial institution. It was originally adopted by the European Committee for Banking Standards (ECBS) and since 1997 as the international standard ISO 13616 under the International Organization for Standardization (ISO). The current version is ISO 13616:2020, which indicates the Society for Worldwide Interbank Financial Telecommunication (SWIFT) as the formal registrar. Initially developed to facilitate payments within the European Union, it has been implemented by most European countries and numerous countries in other parts of the world, mainly in the Middle East and the Caribbean. By July 2024, 88 countries were using the IBAN numbering system.

A telephone card, calling card or phone card for short, is a credit card-size plastic or paper card used to pay for telephone services. It is not necessary to have the physical card except with a stored-value system; knowledge of the access telephone number to dial and the PIN is sufficient. Standard cards which can be purchased and used without any sort of account facility give a fixed amount of credit and are discarded when used up; rechargeable cards can be topped up, or collect payment in arrears. The system for payment and the way in which the card is used to place a telephone call vary from card to card.

A smart card (SC), chip card, or integrated circuit card, is a card used to control access to a resource. It is typically a plastic credit card-sized card with an embedded integrated circuit (IC) chip. Many smart cards include a pattern of metal contacts to electrically connect to the internal chip. Others are contactless, and some are both. Smart cards can provide personal identification, authentication, data storage, and application processing. Applications include identification, financial, public transit, computer security, schools, and healthcare. Smart cards may provide strong security authentication for single sign-on (SSO) within organizations. Numerous nations have deployed smart cards throughout their populations.

Identity theft, identity piracy or identity infringement occurs when someone uses another's personal identifying information, like their name, identifying number, or credit card number, without their permission, to commit fraud or other crimes. The term identity theft was coined in 1964. Since that time, the definition of identity theft has been legally defined throughout both the U.K. and the U.S. as the theft of personally identifiable information. Identity theft deliberately uses someone else's identity as a method to gain financial advantages or obtain credit and other benefits. The person whose identity has been stolen may suffer adverse consequences, especially if they are falsely held responsible for the perpetrator's actions. Personally identifiable information generally includes a person's name, date of birth, social security number, driver's license number, bank account or credit card numbers, PINs, electronic signatures, fingerprints, passwords, or any other information that can be used to access a person's financial resources.

Remote Authentication Dial-In User Service (RADIUS) is a networking protocol that provides centralized authentication, authorization, and accounting (AAA) management for users who connect and use a network service. RADIUS was developed by Livingston Enterprises in 1991 as an access server authentication and accounting protocol. It was later brought into IEEE 802 and IETF standards.

A SIMcard is an integrated circuit (IC) intended to securely store an international mobile subscriber identity (IMSI) number and its related key, which are used to identify and authenticate subscribers on mobile telephone devices. SIMs are also able to store address book contacts information, and may be protected using a PIN code to prevent unauthorized use.

An identity document is a document proving a person's identity.

The Fair Credit Reporting Act (FCRA), 15 U.S.C. § 1681 et seq., is federal legislation enacted to promote the accuracy, fairness, and privacy of consumer information contained in the files of consumer reporting agencies. It was intended to shield consumers from the willful and/or negligent inclusion of erroneous data in their credit reports. To that end, the FCRA regulates the collection, dissemination, and use of consumer information, including consumer credit information. Together with the Fair Debt Collection Practices Act (FDCPA), the FCRA forms the foundation of consumer rights law in the United States. It was originally passed in 1970, and is enforced by the U.S. Federal Trade Commission, the Consumer Financial Protection Bureau, and private litigants.

A background check is a process used by an organisation or person to verify that an individual is who they claim to be, and check their past record to confirm education, employment history, and other activities, and for a criminal record. The frequency, purpose, and legitimacy of background checks vary among countries, industries, and individuals. An employment background check typically takes place when someone applies for a job, but it can also happen at any time the employer deems necessary. A variety of methods are used to complete these checks, including comprehensive database search and letters of reference.

A check verification service provides businesses or individuals with either the ability to check the validity of the actual check or draft being presented, or the ability to verify the history of the account holder, or both.

A credit history is a record of a borrower's responsible repayment of debts. A credit report is a record of the borrower's credit history from a number of sources, including banks, credit card companies, collection agencies, and governments. A borrower's credit score is the result of a mathematical algorithm applied to a credit report and other sources of information to predict future delinquency.

A national identification number, national identity number, or national insurance number or JMBG/EMBG is used by the governments of many countries as a means of tracking their citizens, permanent residents, and temporary residents for the purposes of work, taxation, government benefits, health care, and other governmentally-related functions.

Personal data, also known as personal information or personally identifiable information (PII), is any information related to an identifiable person.

A bank code is a code assigned by a central bank, a bank supervisory body or a Bankers Association in a country to all its licensed member banks or financial institutions. The rules vary to a great extent between the countries. Also the name of bank codes varies. In some countries the bank codes can be viewed over the internet, but mostly in the local language.

The National Registration Identity Card (NRIC), colloquially known as "IC", is a compulsory identity document issued to citizens and permanent residents of Singapore. People must register for an NRIC within one year of attaining the age of 15, or upon becoming a citizen or permanent resident. Re-registrations are required for persons attaining the ages of 30 and 55, unless the person has been issued with an NRIC within ten years prior to the re-registration ages.

Payment cards are part of a payment system issued by financial institutions, such as a bank, to a customer that enables its owner to access the funds in the customer's designated bank accounts, or through a credit account and make payments by electronic transfer with a payment terminal and access automated teller machines (ATMs). Such cards are known by a variety of names, including bank cards, ATM cards, client cards, key cards or cash cards.

A contactless smart card is a contactless credential whose dimensions are credit card size. Its embedded integrated circuits can store data and communicate with a terminal via NFC. Commonplace uses include transit tickets, bank cards and passports.

Credit card fraud is an inclusive term for fraud committed using a payment card, such as a credit card or debit card. The purpose may be to obtain goods or services or to make payment to another account, which is controlled by a criminal. The Payment Card Industry Data Security Standard is the data security standard created to help financial institutions process card payments securely and reduce card fraud.

A credit card is a payment card, usually issued by a bank, allowing its users to purchase goods or services, or withdraw cash, on credit. Using the card thus accrues debt that has to be repaid later. Credit cards are one of the most widely used forms of payment across the world.

The term digital card can refer to a physical item, such as a memory card on a camera, or, increasingly since 2017, to the digital content hosted as a virtual card or cloud card, as a digital virtual representation of a physical card. They share a common purpose: identity management, credit card, debit card or driver's license. A non-physical digital card, unlike a magnetic stripe card, can emulate (imitate) any kind of card.