A commodity market is a market that trades in the primary economic sector rather than manufactured products, such as cocoa, fruit and sugar. Hard commodities are mined, such as gold and oil. Futures contracts are the oldest way of investing in commodities. Commodity markets can include physical trading and derivatives trading using spot prices, forwards, futures, and options on futures. Farmers have used a simple form of derivative trading in the commodities market for centuries for price risk management.

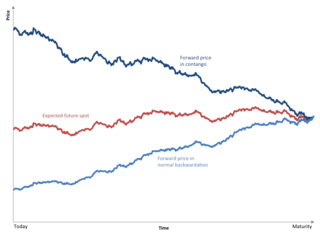

Normal backwardation, also sometimes called backwardation, is the market condition where the price of a commodity's forward or futures contract is trading below the expected spot price at contract maturity. The resulting futures or forward curve would typically be downward sloping, since contracts for further dates would typically trade at even lower prices. In practice, the expected future spot price is unknown, and the term "backwardation" may refer to "positive basis", which occurs when the current spot price exceeds the price of the future.

Contango is a situation in which the futures price of a commodity is higher than the expected spot price of the contract at maturity. In a contango situation, arbitrageurs or speculators are "willing to pay more [now] for a commodity [to be received] at some point in the future than the actual expected price of the commodity [at that future point]. This may be due to people's desire to pay a premium to have the commodity in the future rather than paying the costs of storage and carry costs of buying the commodity today." On the other side of the trade, hedgers are happy to sell futures contracts and accept the higher-than-expected returns. A contango market is also known as a normal market or carrying-cost market.

In finance, a futures contract is a standardized legal contract to buy or sell something at a predetermined price for delivery at a specified time in the future, between parties not yet known to each other. The item transacted is usually a commodity or financial instrument. The predetermined price of the contract is known as the forward price or delivery price. The specified time in the future when delivery and payment occur is known as the delivery date. Because it derives its value from the value of the underlying asset, a futures contract is a derivative.

In finance, a forward contract, or simply a forward, is a non-standardized contract between two parties to buy or sell an asset at a specified future time at a price agreed on in the contract, making it a type of derivative instrument. The party agreeing to buy the underlying asset in the future assumes a long position, and the party agreeing to sell the asset in the future assumes a short position. The price agreed upon is called the delivery price, which is equal to the forward price at the time the contract is entered into.

A hedge is an investment position intended to offset potential losses or gains that may be incurred by a companion investment. A hedge can be constructed from many types of financial instruments, including stocks, exchange-traded funds, insurance, forward contracts, swaps, options, gambles, many types of over-the-counter and derivative products, and futures contracts.

An exchange-traded fund (ETF) is a type of investment fund that is also an exchange-traded product, i.e., it is traded on stock exchanges. ETFs own financial assets such as stocks, bonds, currencies, debts, futures contracts, and/or commodities such as gold bars. Many ETFs provide some level of diversification compared to owning an individual stock.

West Texas Intermediate (WTI) is a grade or mix of crude oil; the term is also used to refer to the spot price, the futures price, or assessed price for that oil. In colloquial usage, WTI usually refers to the WTI Crude Oil futures contract traded on the New York Mercantile Exchange (NYMEX). The WTI oil grade is also known as Texas light sweet. Oil produced from any location can be considered WTI if the oil meets the required qualifications. Spot and futures prices of WTI are used as a benchmark in oil pricing. This grade is described as light crude oil because of its low density and sweet because of its low sulfur content.

In finance, a single-stock future (SSF) is a type of futures contract between two parties to exchange a specified number of stocks in a company for a price agreed today with delivery occurring at a specified future date, the delivery date. The contracts can be later traded on a futures exchange.

National Commodity & Derivatives Exchange Limited (NCDEX) is an Indian online commodity and derivative exchange based in India. It has an independent board of directors and provides a commodity exchange platform for market participants to trade in commodity derivatives. It is an online technology-driven trading exchange. It is a private limited company, its original shareholders were National Stock Exchange of India (NSE), National Bank for Agriculture and Rural Development (NABARD), CRISIL, Life Insurance Corporation (LIC) ICICI Bank. Current shareholders include IFFCO, Jaypee Capital Services, Punjab National Bank,Canara Bank, Build India Capital Advisors, Shree Renuka sugars and Star Agri warehousing.

The Bloomberg Commodity Index (BCOM) is a broadly diversified commodity price index distributed by Bloomberg Index Services Limited. The index was originally launched in 1998 as the Dow Jones-AIG Commodity Index (DJ-AIGCI) and renamed to Dow Jones-UBS Commodity Index (DJ-UBSCI) in 2009, when UBS acquired the index from AIG. On July 1, 2014, the index was rebranded under its current name.

The FTSE/CoreCommodity CRB Index is a commodity futures price index. It was first calculated by Commodity Research Bureau, Inc. in 1957 and made its inaugural appearance in the 1958 CRB Commodity Year Book.

A benchmark crude or marker crude is a crude oil that serves as a reference price for buyers and sellers of crude oil. There are three primary benchmarks, West Texas Intermediate (WTI), Brent Blend, and Dubai Crude. Other well-known blends include the OPEC Reference Basket used by OPEC, Tapis Crude which is traded in Singapore, Western Canadian Select used in Canada, Bonny Light used in Nigeria, Urals oil used in Russia and Mexico's Isthmus. Energy Intelligence Group publishes a handbook which identified 195 major crude streams or blends in its 2011 edition.

The spot market or cash market is a public financial market in which financial instruments or commodities are traded for immediate delivery. It contrasts with a futures market, in which delivery is due at a later date. In a spot market, settlement normally happens in T+2 working days, i.e., delivery of cash and commodity must be done after two working days of the trade date. A spot market can be through an exchange or over-the-counter (OTC). Spot markets can operate wherever the infrastructure exists to conduct the transaction.

Lean Hog is a type of hog (pork) futures contract that can be used to hedge and to speculate on pork prices in the US.

The Deutsche Bank Liquid Commodity Index (DBLCI) is a commodity price index operated by German based Deutsche Bank. It was launched in February 2003 and tracks the performance of six commodities in the energy, precious metals, industrial metals and grain sectors. The DBLCI has constant weightings for each of the six commodities and the index is rebalanced annually in the first week of November. Consequently, the weights fluctuate during the year according to the price movement of the underlying commodity futures.

An exchange, bourse, trading exchange or trading venue is an organized market where (especially) tradable securities, commodities, foreign exchange, futures, and options contracts are bought and sold.

Axis Direct is the flagship brand under Axis Securities Limited, a subsidiary of Axis Bank in India. Providing Demat and Trading services. Its main offices are in Mumbai. The company employs over 2,100 people.

Live cattle is a type of futures contract that can be used to hedge and to speculate on fed cattle prices. Cattle producers, feedlot operators, and merchant exporters can hedge future selling prices for cattle through trading live cattle futures, and such trading is a common part of a producer's price risk management program. Conversely, meat packers, and merchant importers can hedge future buying prices for cattle. Producers and buyers of live cattle can also enter into production and marketing contracts for delivering live cattle in cash or spot markets that include futures prices as part of a reference price formula. Businesses that purchase beef as an input could also hedge beef price risk by purchasing live cattle futures contracts.