An interest rate is the amount of interest due per period, as a proportion of the amount lent, deposited or borrowed. The total interest on an amount lent or borrowed depends on the principal sum, the interest rate, the compounding frequency, and the length of time over which it is lent, deposited or borrowed.

The money market is a component of the economy which provides short-term funds. The money market deals in short-term loans, generally for a period of a year or less.

A bank account is a financial account maintained by a bank or other financial institution in which the financial transactions between the bank and a customer are recorded. Each financial institution sets the terms and conditions for each type of account it offers, which are classified in commonly understood types, such as deposit accounts, credit card accounts, current accounts, loan accounts or many other types of account. A customer may have more than one account. Once an account is opened, funds entrusted by the customer to the financial institution on deposit are recorded in the account designated by the customer. Funds can be withdrawn from loan loaders.

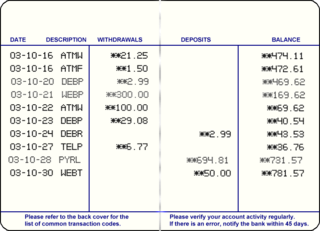

A transaction account, also called a checking account, chequing account, current account, demand deposit account, or share draft account at credit unions, is a deposit account held at a bank or other financial institution. It is available to the account owner "on demand" and is available for frequent and immediate access by the account owner or to others as the account owner may direct. Access may be in a variety of ways, such as cash withdrawals, use of debit cards, cheques (checks) and electronic transfer. In economic terms, the funds held in a transaction account are regarded as liquid funds. In accounting terms they are considered as cash.

Bank fraud is the use of potentially illegal means to obtain money, assets, or other property owned or held by a financial institution, or to obtain money from depositors by fraudulently posing as a bank or other financial institution. In many instances, bank fraud is a criminal offence. While the specific elements of particular banking fraud laws vary depending on jurisdictions, the term bank fraud applies to actions that employ a scheme or artifice, as opposed to bank robbery or theft. For this reason, bank fraud is sometimes considered a white-collar crime.

A repurchase agreement, also known as a repo, RP, or sale and repurchase agreement, is a form of short-term borrowing, mainly in government securities. The dealer sells the underlying security to investors and, by agreement between the two parties, buys them back shortly afterwards, usually the following day, at a slightly higher price.

Eurodollars are time deposits denominated in U.S. dollars at banks outside the United States, and thus are not under the jurisdiction of the Federal Reserve. Consequently, such deposits are subject to much less regulation than similar deposits within the U.S. The term was originally coined for U.S. dollars in European banks, but it expanded over the years to its present definition. A U.S. dollar-denominated deposit in Tokyo or Beijing would be likewise deemed a Eurodollar deposit. There is no connection with the euro currency or the eurozone. The offshore locations of Eurodollar make it exposed to potential country risk and economic risk.

Cash and cash equivalents (CCE) are the most liquid current assets found on a business's balance sheet. Cash equivalents are short-term commitments "with temporarily idle cash and easily convertible into a known cash amount". An investment normally counts to be a cash equivalent when it has a short maturity period of 90 days or less, and can be included in the cash and cash equivalents balance from the date of acquisition when it carries an insignificant risk of changes in the asset value; with more than 90 days maturity, the asset is not considered as cash and cash equivalents. Equity investments mostly are excluded from cash equivalents, unless they are essentially cash equivalents, for instance, if the preferred shares acquired within a short maturity period and with specified recovery date.

A savings account is a bank account at a retail bank whose features include the requirements that only a limited number of withdrawals can take place, it does not have cheque facilities and usually do not have a linked debit card facility, it has limited transfer facilities and cannot be overdrawn. Traditionally, transactions on savings accounts were widely recorded in a passbook, and were sometimes called passbook savings accounts, and bank statements were not provided; however, currently such transactions are commonly recorded electronically and accessible online.

A money market fund is an open-ended mutual fund that invests in short-term debt securities such as US Treasury bills and commercial paper. Money market funds are managed with the goal of maintaining a highly stable asset value through liquid investments, while paying income to investors in the form of dividends. Although they are not insured against loss, actual losses have been quite rare in practice.

Prime brokerage is the generic name for a bundled package of services offered by investment banks, wealth management firms, and securities dealers to hedge funds which need the ability to borrow securities and cash in order to be able to invest on a netted basis and achieve an absolute return. The prime broker provides a centralized securities clearing facility for the hedge fund so the hedge fund's collateral requirements are netted across all deals handled by the prime broker. These two features are advantageous to their clients.

Cash management refers to a broad area of finance involving the collection, handling, and usage of cash. It involves assessing market liquidity, cash flow, and investments.

An overdraft occurs when money is withdrawn from a bank account and the available balance goes below zero. In this situation the account is said to be "overdrawn". If there is a prior agreement with the account provider for an overdraft, and the amount overdrawn is within the authorized overdraft limit, then interest is normally charged at the agreed rate. If the negative balance exceeds the agreed terms, then additional fees may be charged and higher interest rates may apply.

A non-banking financial institution (NBFI) or non-bank financial company (NBFC) is a financial institution that does not have a full banking license or is not supervised by a national or international banking regulatory agency. NBFC facilitate bank-related financial services, such as investment, risk pooling, contractual savings, and market brokering. Examples of these include insurance firms, pawn shops, cashier's check issuers, check cashing locations, payday lending, currency exchanges, and microloan organizations. Alan Greenspan has identified the role of NBFIs in strengthening an economy, as they provide "multiple alternatives to transform an economy's savings into capital investment which act as backup facilities should the primary form of intermediation fail."

A bank is a financial institution that accepts deposits from the public and creates a demand deposit while simultaneously making loans. Lending activities can be directly performed by the bank or indirectly through capital markets.

The interbank lending market is a market in which banks lend funds to one another for a specified term. Most interbank loans are for maturities of one week or less, the majority being over day. Such loans are made at the interbank rate. A sharp decline in transaction volume in this market was a major contributing factor to the collapse of several financial institutions during the financial crisis of 2007–2008.

A deposit account is a bank account maintained by a financial institution in which a customer can deposit and withdraw money. Deposit accounts can be savings accounts, current accounts or any of several other types of accounts explained below.

A fixed deposit (FD) is a financial instrument provided by banks or NBFCs which provides investors a higher rate of interest than a regular savings account, until the given maturity date. It may or may not require the creation of a separate account. It is known as a term deposit or time deposit in Canada, Australia, New Zealand, India and The United States, and as a bond in the United Kingdom and for a fixed deposit is that the money cannot be withdrawn from the FD as compared to a recurring deposit or a demand deposit before maturity. Some banks may offer additional services to FD holders such as loans against FD certificates at competitive interest rates. It's important to note that banks may offer lesser interest rates under uncertain economic conditions. The interest rate varies between 4 and 7.50 percent. The tenure of an FD can vary from 7, 15 or 45 days to 1.5 years and can be as high as 10 years. These investments are safer than Post Office Schemes as they are covered by the Deposit Insurance and Credit Guarantee Corporation (DICGC). However, DICGC guarantees amount up to ₹ 500000(about $6850) per depositor per bank. They also offer income tax and wealth tax benefits.

Kasasa Ltd. is a wholesale financial services company headquartered in Austin, Texas. Kasasa sells branded, community-powered products designed to drive profit and growth for community financial institutions. Kasasa also supports community banks and credit unions by providing them with marketing, consulting, and web-based solutions in order to market their products more effectively.

The Insured Network Deposits (IND) service is a deposit sweep service for broker-dealers and other custodians of funds. Using the service, broker-dealers automatically transfer, or “sweep,” unused cash balances from customer brokerage accounts to interest-bearing deposit accounts at banks insured by the Federal Deposit Insurance Corporation (FDIC) and savings associations. The banks may be affiliated or unaffiliated with the broker-dealer.