External links

| | This economic term article is a stub. You can help Wikipedia by expanding it. |

The written-down value (abbreviated as WDV) is the depreciated value of an asset (movable or immovable) for purposes of taxation. WDV is a method of depreciation in which a fixed rate of depreciation is charged on the book value of the asset, over its useful life

| | This economic term article is a stub. You can help Wikipedia by expanding it. |

Cash flow, in general, refers to payments made into or out of a business, project, or financial product. It can also refer more specifically to a real or virtual movement of money.

The historical cost of an asset at the time it is acquired or created is the value of the costs incurred in acquiring or creating the asset, comprising the consideration paid to acquire or create the asset plus transaction costs. Historical cost accounting involves reporting assets and liabilities at their historical costs, which are not updated for changes in the items' values. Consequently, the amounts reported for these balance sheet items often differ from their current economic or market values.

In accounting, fixed capital is any kind of real, physical asset that is used repeatedly in the production of a product. In economics, fixed capital is a type of capital good that as a real, physical asset is used as a means of production which is durable or isn't fully consumed in a single time period. It contrasts with circulating capital such as raw materials, operating expenses etc.

In accounting, book value is the value of an asset according to its balance sheet account balance. For assets, the value is based on the original cost of the asset less any depreciation, amortization or impairment costs made against the asset. Traditionally, a company's book value is its total assets minus intangible assets and liabilities. However, in practice, depending on the source of the calculation, book value may variably include goodwill, intangible assets, or both. The value inherent in its workforce, part of the intellectual capital of a company, is always ignored. When intangible assets and goodwill are explicitly excluded, the metric is often specified to be tangible book value.

An expense is an item requiring an outflow of money, or any form of fortune in general, to another person or group as payment for an item, service, or other category of costs. For a tenant, rent is an expense. For students or parents, tuition is an expense. Buying food, clothing, furniture, or an automobile is often referred to as an expense. An expense is a cost that is "paid" or "remitted", usually in exchange for something of value. Something that seems to cost a great deal is "expensive". Something that seems to cost little is "inexpensive". "Expenses of the table" are expenses for dining, refreshments, a feast, etc.

In accountancy, depreciation is a term that refers to two aspects of the same concept: first, an actual reduction in the fair value of an asset, such as the decrease in value of factory equipment each year as it is used and wears, and second, the allocation in accounting statements of the original cost of the assets to periods in which the assets are used.

A company's earnings before interest, taxes, depreciation, and amortization is a measure of a company's profitability of the operating business only, thus before any effects of indebtedness, state-mandated payments, and costs required to maintain its asset base. It is derived by subtracting from revenues all costs of the operating business but not decline in asset value, cost of borrowing, lease expenses, and obligations to governments.

In finance, a revaluation of fixed assets is an action that may be required to accurately describe the true value of the capital goods a business owns. This should be distinguished from planned depreciation, where the recorded decline in the value of an asset is tied to its age.

Return on capital (ROC), or return on invested capital (ROIC), is a ratio used in finance, valuation and accounting, as a measure of the profitability and value-creating potential of companies relative to the amount of capital invested by shareholders and other debtholders. It indicates how effective a company is at turning capital into profits.

A fixed asset, also known as long-lived assets or property, plant and equipment (PP&E), is a term used in accounting for assets and property that may not easily be converted into cash. Fixed assets are different from current assets, such as cash or bank accounts, because the latter are liquid assets. In most cases, only tangible assets are referred to as fixed.

Consumption of fixed capital (CFC) is a term used in business accounts, tax assessments and national accounts for depreciation of fixed assets. CFC is used in preference to "depreciation" to emphasize that fixed capital is used up in the process of generating new output, and because unlike depreciation it is not valued at historic cost but at current market value ; CFC may also include other expenses incurred in using or installing fixed assets beyond actual depreciation charges. Normally the term applies only to producing enterprises, but sometimes it applies also to real estate assets.

In accounting, amortization is a method of obtaining the expenses incurred by an intangible asset arising from a decline in value as a result of use or the passage of time. Amortisation is the acquisition cost minus the residual value of an asset, calculated in a systematic manner over an asset's useful economic life. Depreciation is a corresponding concept for tangible assets.

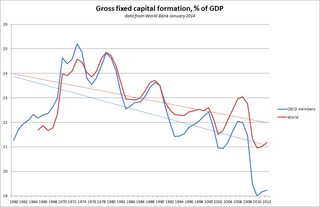

Capital formation is a concept used in macroeconomics, national accounts and financial economics. Occasionally it is also used in corporate accounts. It can be defined in three ways:

Return on capital employed is an accounting ratio used in finance, valuation, and accounting. It is a useful measure for comparing the relative profitability of companies after taking into account the amount of capital used.

Deferred tax is a notional asset or liability to reflect corporate income taxation on a basis that is the same or more similar to recognition of profits than the taxation treatment. Deferred tax liabilities can arise as a result of corporate taxation treatment of capital expenditure being more rapid than the accounting depreciation treatment. Deferred tax assets can arise due to net loss carry-overs, which are only recorded as asset if it is deemed more likely than not that the asset will be used in future fiscal periods. Different countries may also allow or require discounting of the assets or particularly liabilities. There are often disclosure requirements for potential liabilities and assets that are not actually recognised as an asset or liability.

Currency depreciation is the loss of value of a country's currency with respect to one or more foreign reference currencies, typically in a floating exchange rate system in which no official currency value is maintained. Currency appreciation in the same context is an increase in the value of the currency. Short-term changes in the value of a currency are reflected in changes in the exchange rate.

Depreciation recapture is the USA Internal Revenue Service (IRS) procedure for collecting income tax on a gain realized by a taxpayer when the taxpayer disposes of an asset that had previously provided an offset to ordinary income for the taxpayer through depreciation. In other words, because the IRS allows a taxpayer to deduct the depreciation of an asset from the taxpayer's ordinary income, the taxpayer has to report any gain from the disposal of the asset as ordinary income, not as a capital gain.

In financial accounting, an asset is any resource owned or controlled by a business or an economic entity. It is anything that can be used to produce positive economic value. Assets represent value of ownership that can be converted into cash . The balance sheet of a firm records the monetary value of the assets owned by that firm. It covers money and other valuables belonging to an individual or to a business. Total assets can also be called the balance sheet total.

In economics, depreciation is the gradual decrease in the economic value of the capital stock of a firm, nation or other entity, either through physical depreciation, obsolescence or changes in the demand for the services of the capital in question. If the capital stock is in one period , gross (total) investment spending on newly produced capital is and depreciation is , the capital stock in the next period, , is . The net increment to the capital stock is the difference between gross investment and depreciation, and is called net investment.

International Accounting Standard 16 Property, Plant and Equipment or IAS 16 is an international financial reporting standard adopted by the International Accounting Standards Board (IASB). It concerns accounting for property, plant and equipment, including recognition, determination of their carrying amounts, and the depreciation charges and impairment losses to be recognised in relation to them.