Related Research Articles

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by a country or countries. GDP is most often used by the government of a single country to measure its economic health. Due to its complex and subjective nature, this measure is often revised before being considered a reliable indicator.

A variety of measures of national income and output are used in economics to estimate total economic activity in a country or region, including gross domestic product (GDP), gross national product (GNP), net national income (NNI), and adjusted national income. All are specially concerned with counting the total amount of goods and services produced within the economy and by various sectors. The boundary is usually defined by geography or citizenship, and it is also defined as the total income of the nation and also restrict the goods and services that are counted. For instance, some measures count only goods & services that are exchanged for money, excluding bartered goods, while other measures may attempt to include bartered goods by imputing monetary values to them.

This aims to be a complete article list of economics topics:

Productivity is the efficiency of production of goods or services expressed by some measure. Measurements of productivity are often expressed as a ratio of an aggregate output to a single input or an aggregate input used in a production process, i.e. output per unit of input, typically over a specific period of time. The most common example is the (aggregate) labour productivity measure, one example of which is GDP per worker. There are many different definitions of productivity and the choice among them depends on the purpose of the productivity measurement and data availability. The key source of difference between various productivity measures is also usually related to how the outputs and the inputs are aggregated to obtain such a ratio-type measure of productivity.

In economics, output is the quantity and quality of goods or services produced in a given time period, within a given economic network, whether consumed or used for further production. The economic network may be a firm, industry, or nation. The concept of national output is essential in the field of macroeconomics. It is national output that makes a country rich, not large amounts of money.

The national income and product accounts (NIPA) are part of the national accounts of the United States. They are produced by the Bureau of Economic Analysis of the Department of Commerce. They are one of the main sources of data on general economic activity in the United States.

Value added is a term in financial economics for calculating the difference between market value of a product or service, and the sum value of its constituents. It is relatively expressed to the supply-demand curve for specific units of sale. It represents a market equilibrium view of production economics and financial analysis. Value added is distinguished from the accounting term added value which measures only the financial profits earned upon transformational processes for specific items of sale that are available on the market.

In national income accounting, net national income (NNI) is net national product (NNP) minus indirect taxes. Net national income encompasses the income of households, businesses, and the government. Net national income is defined as gross domestic product plus net receipts of wages, salaries and property income from abroad, minus the depreciation of fixed capital assets through wear and tear and obsolescence.

National accounts or national account systems (NAS) are the implementation of complete and consistent accounting techniques for measuring the economic activity of a nation. These include detailed underlying measures that rely on double-entry accounting. By design, such accounting makes the totals on both sides of an account equal even though they each measure different characteristics, for example production and the income from it. As a method, the subject is termed national accounting or, more generally, social accounting. Stated otherwise, national accounts as systems may be distinguished from the economic data associated with those systems. While sharing many common principles with business accounting, national accounts are based on economic concepts. One conceptual construct for representing flows of all economic transactions that take place in an economy is a social accounting matrix with accounts in each respective row-column entry.

The net domestic product (NDP) equals the gross domestic product (GDP) minus depreciation on a country's capital goods.

Consumption of fixed capital (CFC) is a term used in business accounts, tax assessments and national accounts for depreciation of fixed assets. CFC is used in preference to "depreciation" to emphasize that fixed capital is used up in the process of generating new output, and because unlike depreciation it is not valued at historic cost but at current market value ; CFC may also include other expenses incurred in using or installing fixed assets beyond actual depreciation charges. Normally the term applies only to producing enterprises, but sometimes it applies also to real estate assets.

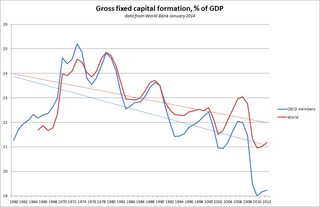

Gross fixed capital formation (GFCF) is a component of the expenditure on gross domestic product (GDP) that indicates how much of the new value added in an economy is invested rather than consumed. It measures the value of acquisitions of new or existing fixed assets by the business sector, governments, and "pure" households minus disposals of fixed assets.

The value product (VP) is an economic concept formulated by Karl Marx in his critique of political economy during the 1860s, and used in Marxian social accounting theory for capitalist economies. Its annual monetary value is approximately equal to the netted sum of six flows of income generated by production:

Intermediate consumption is an economic concept used in national accounts, such as the United Nations System of National Accounts (UNSNA), the US National Income and Product Accounts (NIPA) and the European System of Accounts (ESA).

Operating surplus is an accounting concept used in national accounts statistics and in corporate and government accounts. It is the balancing item of the Generation of Income Account in the UNSNA. It may be used in macro-economics as a proxy for total pre-tax profit income, although entrepreneurial income may provide a better measure of business profits. According to the 2008 SNA, it is the measure of the surplus accruing from production before deducting property income, e.g., land rent and interest.

Net output is an accounting concept used in national accounts such as the United Nations System of National Accounts (UNSNA) and the NIPAs, and sometimes in corporate or government accounts. The concept was originally invented to measure the total net addition to a country's stock of wealth created by production during an accounting interval. The concept of net output is basically "gross revenue from production less the value of goods and services used up in that production". The idea is that if one deducts intermediate expenditures from the annual flow of income generated by production, one obtains a measure of the net new value in the new products created.

Aggregate income is the total of all incomes in an economy without adjustments for inflation, taxation, or types of double counting. Aggregate income is a form of GDP that is equal to Consumption expenditure plus net profits. 'Aggregate income' in economics is a broad conceptual term. It may express the proceeds from total output in the economy for producers of that output. There are a number of ways to measure aggregate income, but GDP is one of the best known and most widely used.

The Gross Domestic Income (GDI) is the total income received by all sectors of an economy within a state. It includes the sum of all wages, profits, and taxes, minus subsidies. Since all income is derived from production, the gross domestic income of a country should exactly equal its gross domestic product (GDP). The GDP is a very commonly cited statistic measuring the economic activity of countries, and the GDI is quite uncommon.

The annual United Kingdom National Accounts records and describes economic activity in the United Kingdom and as such is used by government, banks, academics and industries to formulate the economic and social policies and monitor the economic progress of the United Kingdom. It also allows international comparisons to be made. The Blue Book is published by the UK Office for National Statistics alongside the United Kingdom Balance of Payments – The Pink Book.

In Marxian economics, surplus value is the difference between the amount raised through a sale of a product and the amount it cost to manufacture it: i.e. the amount raised through sale of the product minus the cost of the materials, plant and labour power. The concept originated in Ricardian socialism, with the term "surplus value" itself being coined by William Thompson in 1824; however, it was not consistently distinguished from the related concepts of surplus labor and surplus product. The concept was subsequently developed and popularized by Karl Marx. Marx's formulation is the standard sense and the primary basis for further developments, though how much of Marx's concept is original and distinct from the Ricardian concept is disputed. Marx's term is the German word "Mehrwert", which simply means value added, and is cognate to English "more worth".

References

- 1 2 OECD Glossary of Statistical Terms.

- ↑ Kramer, Leslie (March 20, 2020). "What is GDP and Why is It So Important to Economists and Investors?".

- ↑ Ivanov; Webster (September 1, 2007). "Measuring the Impact of Tourism on Economic Growth". Tourism Economics. 13 (3): 21–30. doi:10.5367/000000007781497773. S2CID 153597825.

{{cite journal}}: CS1 maint: multiple names: authors list (link) - ↑ "Guide to Gross Value Added (GVA)". Office for National Statistics. 2002-11-15. Retrieved 2012-07-08.

- ↑ "Productivity measures in the OECD Productivity Database". OECD Compendium of Productivity Indicators. 2019: 122 – via Google scholar.

- ↑ Kenton, Will (March 20, 2020). "Gross Value Added – GVA Definition".

| Authority control databases: National |

|---|