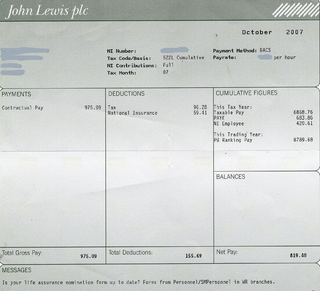

National Insurance (NI) is a fundamental component of the welfare state in the United Kingdom. It acts as a form of social security, since payment of NI contributions establishes entitlement to certain state benefits for workers and their families.

Factoring is a financial transaction and a type of debtor finance in which a business sells its accounts receivable to a third party at a discount. A business will sometimes factor its receivable assets to meet its present and immediate cash needs. Forfaiting is a factoring arrangement used in international trade finance by exporters who wish to sell their receivables to a forfaiter. Factoring is commonly referred to as accounts receivable factoring, invoice factoring, and sometimes accounts receivable financing. Accounts receivable financing is a term more accurately used to describe a form of asset based lending against accounts receivable. The Commercial Finance Association is the leading trade association of the asset-based lending and factoring industries.

A pay-as-you-earn tax (PAYE), or pay-as-you-go (PAYG) in Australia, is a withholding of taxes on income payments to employees. Amounts withheld are treated as advance payments of income tax due. They are refundable to the extent they exceed tax as determined on tax returns. PAYE may include withholding the employee portion of insurance contributions or similar social benefit taxes. In most countries, they are determined by employers but subject to government review. PAYE is deducted from each paycheck by the employer and must be remitted promptly to the government. Most countries refer to income tax withholding by other terms, including pay-as-you-go tax.

A payroll is a list of employees of a company who are entitled to receive compensation as well as other work benefits, as well as the amounts that each should obtain. Along with the amounts that each employee should receive for time worked or tasks performed, payroll can also refer to a company's records of payments that were previously made to employees, including salaries and wages, bonuses, and withheld taxes, or the company's department that deals with compensation. A company may handle all aspects of the payroll process in-house or can outsource aspects to a payroll processing company.

Freelance, freelancer, or freelance worker, are terms commonly used for a person who is self-employed and not necessarily committed to a particular employer long-term. Freelance workers are sometimes represented by a company or a temporary agency that resells freelance labor to clients; others work independently or use professional associations or websites to get work.

HM Revenue and Customs is a non-ministerial department of the UK Government responsible for the collection of taxes, the payment of some forms of state support, the administration of other regulatory regimes including the national minimum wage and the issuance of national insurance numbers. HMRC was formed by the merger of the Inland Revenue and HM Customs and Excise, which took effect on 18 April 2005. The department's logo is the Tudor Crown enclosed within a circle.

In the United Kingdom, and formerly the Republic of Ireland, a P45 is the reference code of a document titled Details of employee leaving work. The term is used in British and Irish slang as a metonym for termination of employment. The equivalent slang term in the United States is "pink slip".

A tax refund or tax rebate is a payment to the taxpayer due to the taxpayer having paid more tax than they owed.

In the United Kingdom, a tax return is a document that must be filed with HM Revenue & Customs declaring liability for taxation. Different bodies must file different returns with respect to various forms of taxation. The main returns currently in use are:

Per diem or daily allowance is a specific amount of money that an organization gives an individual, typically an employee, per day to cover living expenses when travelling on the employer's business.

IR35 is the United Kingdom's anti-avoidance tax legislation, the intermediaries legislation contained in Chapter 8 of Income Tax Act 2003. The legislation is designed to tax 'disguised' employment at a rate similar to employment. In this context, "disguised employees" means workers who receive payments from a client via an intermediary, i.e. their own limited company, and whose relationship with their client is such that had they been paid directly they would be employees of the client.

The Student Loans Company (SLC) is an executive non-departmental public body company in the United Kingdom that provides student loans. It is owned by the UK Government's Department for Education (85%), the Scottish Government (5%), the Welsh Government (5%) and the Northern Ireland Executive (5%). The SLC is funded entirely by the UK taxpayer. It is responsible for both providing loans to students, and collecting loan repayments alongside HM Revenue and Customs (HMRC). The SLC's head office is in Glasgow, with other offices in Darlington and Llandudno.

An employment agency is an organization which matches employers to employees. In developed countries, there are multiple private businesses which act as employment agencies and a publicly funded employment agency.

A managed service company (MSC) is a form of company structure in the United Kingdom designed to reduce the individual tax liabilities of the directors and shareholders.

Liberty Accounts is an integrated online accounting and payroll system designed specifically for small and medium enterprises, not-for-profit organisation and charities in the UK. Also described as a software as a service or SaaS cloud computing application, Liberty is available to business owners, treasurers and accountants.

Cable & Wireless plc v Muscat [2006] EWCA Civ 220 is a UK labour law case, concerning the test for an implied contract between an employee and a place they work through an employment agency. It holds that with reference to the reality of the relationship, an implied contract should be found according to the ordinary rules of construction.

ContractorUK, is a news and community website for independent contractors in the UK. It has been online since 1999, since the early days of IR35 and the initial inflation of the dot-com bubble.

The Apprenticeship Levy is a UK tax on employers which is used to fund apprenticeship training.

False self-employment is a situation in which a person registered as self-employed, a freelancer, or a temp is de facto an employee carrying out a professional activity under the authority and subordination of another company. Such false self-employment is often a way to circumvent social welfare and employment legislation, for example by avoiding employer's social security and income tax contributions. While a modern "gig economy" encourages more casual employment practices in the interests of labour flexibility, the extent to which this disguises precarious employment and denial of rights is of growing concern to authorities.

Making Tax Digital (MTD) is a UK government initiative that sets out a vision for the 'end of the tax return' and a 'transformed tax system', announced in 2015 and originally intended to be in place by 2020. HM Revenue and Customs (HMRC) states that the main goal of MTD is to make tax administration more effective, more efficient and simpler for taxpayers.