Austerity is a set of political-economic policies that aim to reduce government budget deficits through spending cuts, tax increases, or a combination of both. There are three primary types of austerity measures: higher taxes to fund spending, raising taxes while cutting spending, and lower taxes and lower government spending. Austerity measures are often used by governments that find it difficult to borrow or meet their existing obligations to pay back loans. The measures are meant to reduce the budget deficit by bringing government revenues closer to expenditures. Proponents of these measures state that this reduces the amount of borrowing required and may also demonstrate a government's fiscal discipline to creditors and credit rating agencies and make borrowing easier and cheaper as a result.

Kenneth Saul Rogoff is an American economist and chess Grandmaster. He is the Thomas D. Cabot Professor of Public Policy and professor of economics at Harvard University.

In economics, an optimum currency area (OCA) or optimal currency region (OCR) is a geographical region in which it would maximize economic efficiency to have the entire region share a single currency.

The Great Recession was a period of marked general decline, i.e., a recession, observed in national economies globally that occurred from late 2007 into 2009. The scale and timing of the recession varied from country to country. At the time, the International Monetary Fund (IMF) concluded that it was the most severe economic and financial meltdown since the Great Depression. One result was a serious disruption of normal international relations.

Following the global financial crisis of 2007–2008, there was a worldwide resurgence of interest in Keynesian economics among prominent economists and policy makers. This included discussions and implementation of economic policies in accordance with the recommendations made by John Maynard Keynes in response to the Great Depression of the 1930s, most especially fiscal stimulus and expansionary monetary policy.

The European debt crisis, often also referred to as the eurozone crisis or the European sovereign debt crisis, is a multi-year debt crisis that took place in the European Union (EU) from 2009 until the mid to late 2010s. Several eurozone member states were unable to repay or refinance their government debt or to bail out over-indebted banks under their national supervision without the assistance of third parties like other eurozone countries, the European Central Bank (ECB), or the International Monetary Fund (IMF).

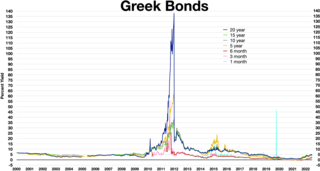

Greece faced a sovereign debt crisis in the aftermath of the financial crisis of 2007–2008. Widely known in the country as The Crisis, it reached the populace as a series of sudden reforms and austerity measures that led to impoverishment and loss of income and property, as well as a small-scale humanitarian crisis. In all, the Greek economy suffered the longest recession of any advanced mixed economy to date. As a result, the Greek political system has been upended, social exclusion increased, and hundreds of thousands of well-educated Greeks have left the country.

From late 2009, fears of a sovereign debt crisis in some European states developed, with the situation becoming particularly tense in early 2010. Greece was most acutely affected, but fellow Eurozone members Cyprus, Ireland, Italy, Portugal, and Spain were also significantly affected. In the EU, especially in countries where sovereign debt has increased sharply due to bank bailouts, a crisis of confidence has emerged with the widening of bond yield spreads and risk insurance on credit default swaps between these countries and other EU members, most importantly Germany.

Debt crisis is a situation in which a government loses the ability of paying back its governmental debt. When the expenditures of a government are more than its tax revenues for a prolonged period, the government may enter into a debt crisis. Various forms of governments finance their expenditures primarily by raising money through taxation. When tax revenues are insufficient, the government can make up the difference by issuing debt.

End This Depression Now! is a non-fiction book by the American economist Paul Krugman. The book is intended for a general audience and was published by W. W. Norton & Company in April 2012. Krugman has presented his book at the London School of Economics, on fora.tv, and elsewhere.

The Return of Depression Economics and the Crisis of 2008 is a non-fiction book by American economist and Nobel Prize winner Paul Krugman, written in response to growing socio-political discourse on the return of economic conditions similar to The Great Depression. The book was first published in 1999 and later updated in 2008 following his Nobel Prize of Economics. The Return of Depression Economics uses Keynesian analysis of past economics crisis, drawing parallels between the 2008 financial crisis and the Great Depression. Krugman challenges orthodox economic notions of restricted government spending, deregulation of markets and the efficient market hypothesis. Krugman offers policy recommendations for the prevention of future financial crises and suggests that policymakers "relearn the lessons our grandfathers were taught by the Great Depression" and prop up spending and enable broader access to credit.

The 2010–2014 Portuguese financial crisis was part of the wider downturn of the Portuguese economy that started in 2001 and possibly ended between 2016 and 2017. The period from 2010 to 2014 was probably the hardest and more challenging part of the entire economic crisis; this period includes the 2011–14 international bailout to Portugal and was marked by intense austerity policies, more intense than the wider 2001-2017 crisis. Economic growth stalled in Portugal between 2001 and 2002, and following years of internal economic crisis, the worldwide Great Recession started to hit Portugal in 2008 and eventually led to the country being unable to repay or refinance its government debt without the assistance of third parties. To prevent an insolvency situation in the debt crisis, Portugal applied in April 2011 for bail-out programs and drew a cumulated €78 billion from the IMF, the EFSM, and the EFSF. Portugal exited the bailout in May 2014, the same year that positive economic growth re-appeared following three years of recession. The government achieved a 2.1% budget deficit in 2016 and in 2017 the economy grew 2.7%.

European debt crisis contagion refers to the possible spread of the ongoing European sovereign-debt crisis to other Eurozone countries. This could make it difficult or impossible for more countries to repay or re-finance their government debt without the assistance of third parties. By 2012 the debt crisis forced 5 out of 17 Eurozone countries to seek help from other nations. Some believed that negative effects could spread further possibly forcing one or more countries into default.

The 2012–2013 Cypriot financial crisis was an economic crisis in the Republic of Cyprus that involved the exposure of Cypriot banks to overleveraged local property companies, the Greek government-debt crisis, the downgrading of the Cypriot government's bond credit rating to junk status by international credit rating agencies, the consequential inability to refund its state expenses from the international markets and the reluctance of the government to restructure the troubled Cypriot financial sector.

The European debt crisis is an ongoing financial crisis that has made it difficult or impossible for some countries in the euro area to repay or re-finance their government debt without the assistance of third parties.

The eurozone crisis is an ongoing financial crisis that has made it difficult or impossible for some countries in the euro area to repay or re-finance their government debt without the assistance of third parties.

The eurozone crisis is an ongoing financial crisis that has made it difficult or impossible for some countries in the euro area to repay or re-finance their government debt without the assistance of third parties.

The Greek government-debt crisis began in 2009 and, as of November 2017, was still ongoing. During this period, many changes had occurred in Greece. The income of many Greeks has declined, levels of unemployment have increased, elections and resignations of politicians have altered the country's political landscape radically, the Greek parliament has passed many austerity bills, and protests have become common sights throughout the country.

This article details the fourteen austerity packages passed by the Government of Greece between 2010 and 2017. These austerity measures were a result of the Greek government-debt crisis and other economic factors. All of the legislation listed remains in force.

A referendum to decide whether Greece should accept the bailout conditions in the country's government-debt crisis proposed jointly by the European Commission (EC), the International Monetary Fund (IMF) and the European Central Bank (ECB) on 25 June 2015 took place on 5 July 2015. The referendum was announced by Prime Minister Alexis Tsipras in the early morning of 27 June 2015 and ratified the following day by the Parliament and the President. It was the first referendum to be held since the republic referendum of 1974 and the only one in modern Greek history not to concern the form of government.