Finance is the study and discipline of money, currency and capital assets. It is related to, but not synonymous with economics, which is the study of production, distribution, and consumption of money, assets, goods and services . Finance activities take place in financial systems at various scopes; thus, the field can be roughly divided into personal, corporate, and public finance.

A financial market is a market in which people trade financial securities and derivatives at low transaction costs. Some of the securities include stocks and bonds, raw materials and precious metals, which are known in the financial markets as commodities.

In financial accounting, a balance sheet is a summary of the financial balances of an individual or organization, whether it be a sole proprietorship, a business partnership, a corporation, private limited company or other organization such as government or not-for-profit entity. Assets, liabilities and ownership equity are listed as of a specific date, such as the end of its financial year. A balance sheet is often described as a "snapshot of a company's financial condition". It is the summary of each and every financial statement of an organization.

The money market is a component of the economy that provides short-term funds. The money market deals in short-term loans, generally for a period of a year or less.

Debits and credits in double-entry bookkeeping are entries made in account ledgers to record changes in value resulting from business transactions. A debit entry in an account represents a transfer of value to that account, and a credit entry represents a transfer from the account. Each transaction transfers value from credited accounts to debited accounts. For example, a tenant who writes a rent cheque to a landlord would enter a credit for the bank account on which the cheque is drawn, and a debit in a rent expense account. Similarly, the landlord would enter a credit in the rent income account associated with the tenant and a debit for the bank account where the cheque is deposited.

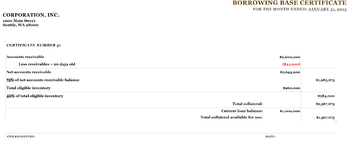

Factoring is a financial transaction and a type of debtor finance in which a business sells its accounts receivable to a third party at a discount. A business will sometimes factor its receivable assets to meet its present and immediate cash needs. Forfaiting is a factoring arrangement used in international trade finance by exporters who wish to sell their receivables to a forfaiter. Factoring is commonly referred to as accounts receivable factoring, invoice factoring, and sometimes accounts receivable financing. Accounts receivable financing is a term more accurately used to describe a form of asset based lending against accounts receivable. The Commercial Finance Association is the leading trade association of the asset-based lending and factoring industries.

In financial accounting, a cash flow statement, also known as statement of cash flows, is a financial statement that shows how changes in balance sheet accounts and income affect cash and cash equivalents, and breaks the analysis down to operating, investing and financing activities. Essentially, the cash flow statement is concerned with the flow of cash in and out of the business. As an analytical tool, the statement of cash flows is useful in determining the short-term viability of a company, particularly its ability to pay bills. International Accounting Standard 7 is the International Accounting Standard that deals with cash flow statements.

In financial accounting, free cash flow (FCF) or free cash flow to firm (FCFF) is the amount by which a business's operating cash flow exceeds its working capital needs and expenditures on fixed assets. It is that portion of cash flow that can be extracted from a company and distributed to creditors and securities holders without causing issues in its operations. As such, it is an indicator of a company's financial flexibility and is of interest to holders of the company's equity, debt, preferred stock and convertible securities, as well as potential lenders and investors.

Cash and cash equivalents (CCE) are the most liquid current assets found on a business's balance sheet. Cash equivalents are short-term commitments "with temporarily idle cash and easily convertible into a known cash amount". An investment normally counts as a cash equivalent when it has a short maturity period of 90 days or less, and can be included in the cash and cash equivalents balance from the date of acquisition when it carries an insignificant risk of changes in the asset value. If it has a maturity of more than 90 days, it is not considered a cash equivalent. Equity investments mostly are excluded from cash equivalents, unless they are essentially cash equivalents.

Asset-based lending is any kind of lending secured by an asset. This means, if the loan is not repaid, the asset is taken. In this sense, a mortgage is an example of an asset-based loan. More commonly however, the phrase is used to describe lending to business and large corporations using assets not normally used in other loans. Typically, the different types of asset-based loans include accounts receivable financing, inventory financing, equipment financing, or real estate financing. Asset-based lending in this more specific sense is possible only in certain countries whose legal systems allow borrowers to pledge such assets to lenders as collateral for loans.

Commercial paper, in the global financial market, is an unsecured promissory note with a fixed maturity of rarely more than 270 days. In layperson terms, it is like an "IOU" but can be bought and sold because its buyers and sellers have some degree of confidence that it can be successfully redeemed later for cash, based on their assessment of the creditworthiness of the issuing company.

A mortgage-backed security (MBS) is a type of asset-backed security which is secured by a mortgage or collection of mortgages. The mortgages are aggregated and sold to a group of individuals that securitizes, or packages, the loans together into a security that investors can buy. Bonds securitizing mortgages are usually treated as a separate class, termed residential; another class is commercial, depending on whether the underlying asset is mortgages owned by borrowers or assets for commercial purposes ranging from office space to multi-dwelling buildings.

Working capital (WC) is a financial metric which represents operating liquidity available to a business, organisation, or other entity, including governmental entities. Along with fixed assets such as plant and equipment, working capital is considered a part of operating capital. Gross working capital is equal to current assets. Working capital is calculated as current assets minus current liabilities. If current assets are less than current liabilities, an entity has a working capital deficiency, also called a working capital deficit and negative working capital.

An asset-backed security (ABS) is a security whose income payments, and hence value, are derived from and collateralized by a specified pool of underlying assets.

Credit is the trust which allows one party to provide money or resources to another party wherein the second party does not reimburse the first party immediately, but promises either to repay or return those resources at a later date. The resources provided by the first party can be either property, fulfillment of promises, or performances. In other words, credit is a method of making reciprocity formal, legally enforceable, and extensible to a large group of unrelated people.

The vast majority of all second lien loans are senior secured obligations of the borrower. Second lien loans differ from both unsecured debt and subordinated debt.

Venture debt or venture lending is a type of debt financing provided to venture-backed companies by specialized banks or non-bank lenders to fund working capital or capital expenses, such as purchasing equipment. Venture debt can complement venture capital and provide value to fast growing companies and their investors. Unlike traditional bank lending, venture debt is available to startups and growth companies that do not have positive cash flows or significant assets to give as collateral. Venture debt providers combine their loans with warrants, or rights to purchase equity, to compensate for the higher risk of default, although this is not always the case.

Asset Back Lending (ABL) typically provides collateralized credit facilities to borrowers with high financial leverage and marginal cash flows.

Distressed lending typically provides credit facilities to borrowers with good cash generation capacity but short-term liquidity issues.

A financial ratio or accounting ratio is a relative magnitude of two selected numerical values taken from an enterprise's financial statements. Often used in accounting, there are many standard ratios used to try to evaluate the overall financial condition of a corporation or other organization. Financial ratios may be used by managers within a firm, by current and potential shareholders (owners) of a firm, and by a firm's creditors. Financial analysts use financial ratios to compare the strengths and weaknesses in various companies. If shares in a company are traded in a financial market, the market price of the shares is used in certain financial ratios.