Exempt property, under the law of property in many jurisdictions, is property that can neither be passed by will nor claimed by creditors of the deceased in the event that a decedent leaves a surviving spouse or surviving descendants. Typically, exempt property includes a family car, and a certain amount of cash (perhaps $10,000-$20,000), or the equivalent value in personal property.

Exempt property calculations and provisions are determined on a state-by-state basis. This is important within the bankruptcy process, and may affect an individual's decision to file Chapter 7 or Chapter 13bankruptcy. State exemptions vary from strict to generous. For example, Texas is more lenient in allowing your homestead and up to $60,000 in personal property.[1] Texas also exempts certain investments and insurance policies. Other states, such as Arizona, are more strict and may exempt only $150 in a checking account comparatively speaking. Even further, other states have more moderate policies, with California's homestead exemption law providing between $300,000 to $600,000 of exempt equity in a homestead, depending on the county where the debtor is located.[2]

Bankruptcy is a legal process through which people or other entities who cannot repay debts to creditors may seek relief from some or all of their debts. In most jurisdictions, bankruptcy is imposed by a court order, often initiated by the debtor.

The United States of America has separate federal, state, and local governments with taxes imposed at each of these levels. Taxes are levied on income, payroll, property, sales, capital gains, dividends, imports, estates and gifts, as well as various fees. In 2010, taxes collected by federal, state, and municipal governments amounted to 24.8% of GDP. In the OECD, only Chile and Mexico are taxed less as a share of their GDP.

Chapter 7 of Title 11 of the United States Code governs the process of liquidation under the bankruptcy laws of the United States, in contrast to Chapters 11 and 13, which govern the process of reorganization of a debtor. Chapter 7 is the most common form of bankruptcy in the United States.

Personal bankruptcy law allows, in certain jurisdictions, an individual to be declared bankrupt. Virtually every country with a modern legal system features some form of debt relief for individuals. Personal bankruptcy is distinguished from corporate bankruptcy.

An estate, in common law, is the net worth of a person at any point in time alive or dead. It is the sum of a person's assets – legal rights, interests and entitlements to property of any kind – less all liabilities at that time. The issue is of special legal significance on a question of bankruptcy and death of the person.

Tax exemption is the reduction or removal of a liability to make a compulsory payment that would otherwise be imposed by a ruling power upon persons, property, income, or transactions. Tax-exempt status may provide complete relief from taxes, reduced rates, or tax on only a portion of items. Examples include exemption of charitable organizations from property taxes and income taxes, veterans, and certain cross-border or multi-jurisdictional scenarios.

In the United States, bankruptcy is largely governed by federal law, commonly referred to as the "Bankruptcy Code" ("Code"). The United States Constitution authorizes Congress to enact "uniform Laws on the subject of Bankruptcies throughout the United States". Congress has exercised this authority several times since 1801, including through adoption of the Bankruptcy Reform Act of 1978, as amended, codified in Title 11 of the United States Code and the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 (BAPCPA).

Allodial title constitutes ownership of real property that is independent of any superior landlord. Allodial title is related to the concept of land held "in allodium", or land ownership by occupancy and defense of the land.

The homestead exemption is a legal regime to protect the value of the homes of residents from property taxes, creditors, and circumstances that arise from the death of the homeowner's spouse.

A use tax is a type of tax levied in the United States by numerous state governments. It is essentially the same as a sales tax but is applied not where a product or service was sold but where a merchant bought a product or service and then converted it for its own use, without having paid tax when it was initially purchased. Use taxes are functionally equivalent to sales taxes. They are typically levied upon the use, storage, enjoyment, or other consumption in the state of tangible personal property that has not been subjected to a sales tax.

The Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 (BAPCPA) is a legislative act that made several significant changes to the United States Bankruptcy Code. Referred to colloquially as the "New Bankruptcy Law", the Act of Congress attempts to, among other things, make it more difficult for some consumers to file bankruptcy under Chapter 7; some of these consumers may instead utilize Chapter 13.

The homestead exemption in Florida may refer to three different types of homestead exemptions under Florida law:

exemption from forced sale before and at death per Art. X, Section 4(a)-(b) of the Florida Constitution;

restrictions on devise and alienation, Art. X, Section 4(c) of the Florida Constitution;

and exemption from taxation per Art. VII, Section 6 of the Florida Constitution.

Sales taxes in the United States are taxes placed on the sale or lease of goods and services in the United States. Sales tax is governed at the state level and no national general sales tax exists. 45 states, the District of Columbia, the territories of Puerto Rico, and Guam impose general sales taxes that apply to the sale or lease of most goods and some services, and states also may levy selective sales taxes on the sale or lease of particular goods or services. States may grant local governments the authority to impose additional general or selective sales taxes.

Attachment of earnings is a legal process in civil litigation by which a defendant's wages or other earnings are taken to pay for a debt. This collections process is used in the common law system, especially Britain and the United States, but in other legal regimes as well.

The 2007 Texas Constitutional Amendment Election took place 6 November 2007.

Asset protection is a set of legal techniques and a body of statutory and common law dealing with protecting assets of individuals and business entities from civil money judgments. The goal of asset protection planning is to insulate assets from claims of creditors without perjury or tax evasion.

The estate tax in the United States is a federal tax on the transfer of the estate of a person who dies. The tax applies to property that is transferred by will or, if the person has no will, according to state laws of intestacy. Other transfers that are subject to the tax can include those made through a trust and the payment of certain life insurance benefits or financial accounts. The estate tax is part of the federal unified gift and estate tax in the United States. The other part of the system, the gift tax, applies to transfers of property during a person's life.

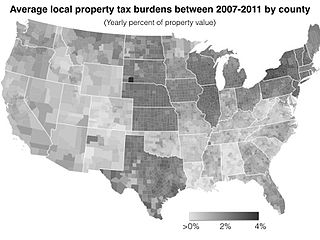

Most local governments in the United States impose a property tax, also known as a millage rate, as a principal source of revenue. This tax may be imposed on real estate or personal property. The tax is nearly always computed as the fair market value of the property times an assessment ratio times a tax rate, and is generally an obligation of the owner of the property. Values are determined by local officials, and may be disputed by property owners. For the taxing authority, one advantage of the property tax over the sales tax or income tax is that the revenue always equals the tax levy, unlike the other taxes. The property tax typically produces the required revenue for municipalities' tax levies. A disadvantage to the taxpayer is that the tax liability is fixed, while the taxpayer's income is not.

Law v. Siegel, 571 U.S. 415 (2014), is a ruling of the Supreme Court of the United States that describes the extent of the powers of bankruptcy courts in dealing with the bad faith of debtors.

Bankruptcy in Florida is made under title 11 of the United States Code, which is referred to as the Bankruptcy Code. Although bankruptcy is a federal procedure, in certain regards, it looks to state law, such as to exemptions and to define property rights. The Bankruptcy Code provides that each state has the choice whether to "opt in" and use the federal exemptions or to "opt out" and to apply the state law exemptions. Florida is an "opt out" state in regard to exemptions. Bankruptcy in the United States is provided for under federal law as provided in the United States Constitution. Under the federal constitution, there are no state bankruptcy courts. The bankruptcy laws are primarily contained in 11 U.S.C. 101, et seq. The Bankruptcy Code underwent a substantial amendment in 2005 with the "Bankruptcy Abuse Prevention and Consumer Protection Act of 2005", often referred to as "BAPCPA". The Bankruptcy Code provides for a set of federal bankruptcy exemptions, but each states is allowed is choose whether it will "opt in" or "opt out" of the federal exemptions. In the event that a state opts out of the federal exemptions, the exemptions are provided for the particular exemption laws of the state with the application with certain federal exemptions.

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.