In time series analysis, a fan chart is a chart that joins a simple line chart for observed past data, by showing ranges for possible values of future data together with a line showing a central estimate or most likely value for the future outcomes. As predictions become increasingly uncertain the further into the future one goes, these forecast ranges spread out, creating distinctive wedge or "fan" shapes, hence the term. Alternative forms of the chart can also include uncertainty for past data, such as preliminary data that is subject to revision.

A time series is a series of data points indexed in time order. Most commonly, a time series is a sequence taken at successive equally spaced points in time. Thus it is a sequence of discrete-time data. Examples of time series are heights of ocean tides, counts of sunspots, and the daily closing value of the Dow Jones Industrial Average.

A line chart or line plot or line graph is a type of chart which displays information as a series of data points called 'markers' connected by straight line segments. It is a basic type of chart common in many fields. It is similar to a scatter plot except that the measurement points are ordered and joined with straight line segments. A line chart is often used to visualize a trend in data over intervals of time – a time series – thus the line is often drawn chronologically. In these cases they are known as run charts.

Contents

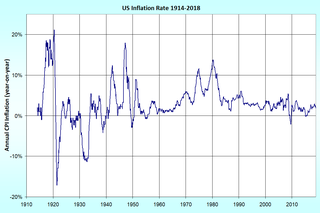

The term "fan chart" was coined by the Bank of England, which has been using these charts and this term since 1997 in its "Inflation Report" [1] [2] to describe its best prevision of future inflation to the general public. Fan charts have been used extensively in finance and monetary policy, for instance to represent forecasts of inflation.

The Bank of England is the central bank of the United Kingdom and the model on which most modern central banks have been based. Established in 1694 to act as the English Government's banker, and still one of the bankers for the Government of the United Kingdom, it is the world's eighth-oldest bank. It was privately owned by stockholders from its foundation in 1694 until it was nationalised in 1946.

In economics, inflation is a sustained increase in the general price level of goods and services in an economy over a period of time. When the general price level rises, each unit of currency buys fewer goods and services; consequently, inflation reflects a reduction in the purchasing power per unit of money – a loss of real value in the medium of exchange and unit of account within the economy. The measure of inflation is the inflation rate, the annualized percentage change in a general price index, usually the consumer price index, over time. The opposite of inflation is deflation, a sustained decrease in the general price level of goods and services.

Finance is a field that is concerned with the allocation (investment) of assets and liabilities over space and time, often under conditions of risk or uncertainty. Finance can also be defined as the art of money management. Participants in the market aim to price assets based on their risk level, fundamental value, and their expected rate of return. Finance can be split into three sub-categories: public finance, corporate finance and personal finance.