In finance and economics, interest is payment from a borrower or deposit-taking financial institution to a lender or depositor of an amount above repayment of the principal sum, at a particular rate. It is distinct from a fee which the borrower may pay to the lender or some third party. It is also distinct from dividend which is paid by a company to its shareholders (owners) from its profit or reserve, but not at a particular rate decided beforehand, rather on a pro rata basis as a share in the reward gained by risk taking entrepreneurs when the revenue earned exceeds the total costs.

The time value of money is the widely accepted conjecture that there is greater benefit to receiving a sum of money now rather than an identical sum later. It may be seen as an implication of the later-developed concept of time preference.

In finance, a loan is the transfer of money by one party to another with an agreement to pay it back. The recipient, or borrower, incurs a debt and is usually required to pay interest for the use of the money.

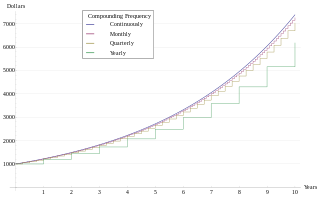

Compound interest is interest accumulated from a principal sum and previously accumulated interest. It is the result of reinvesting or retaining interest that would otherwise be paid out, or of the accumulation of debts from a borrower.

A variable-rate mortgage, adjustable-rate mortgage (ARM), or tracker mortgage is a mortgage loan with the interest rate on the note periodically adjusted based on an index which reflects the cost to the lender of borrowing on the credit markets. The loan may be offered at the lender's standard variable rate/base rate. There may be a direct and legally defined link to the underlying index, but where the lender offers no specific link to the underlying market or index, the rate can be changed at the lender's discretion. The term "variable-rate mortgage" is most common outside the United States, whilst in the United States, "adjustable-rate mortgage" is most common, and implies a mortgage regulated by the Federal government, with caps on charges. In many countries, adjustable rate mortgages are the norm, and in such places, may simply be referred to as mortgages.

The term annual percentage rate of charge (APR), corresponding sometimes to a nominal APR and sometimes to an effective APR (EAPR), is the interest rate for a whole year (annualized), rather than just a monthly fee/rate, as applied on a loan, mortgage loan, credit card, etc. It is a finance charge expressed as an annual rate. Those terms have formal, legal definitions in some countries or legal jurisdictions, but in the United States:

An FHA insured loan is a US Federal Housing Administration mortgage insurance backed mortgage loan that is provided by an FHA-approved lender. FHA mortgage insurance protects lenders against losses. They have historically allowed lower-income Americans to borrow money to purchase a home that they would not otherwise be able to afford. Because this type of loan is more geared towards new house owners than real estate investors, FHA loans are different from conventional loans in the sense that the house must be owner-occupant for at least a year. Since loans with lower down-payments usually involve more risk to the lender, the home-buyer must pay a two-part mortgage insurance that involves a one-time bulk payment and a monthly payment to compensate for the increased risk. Frequently, individuals "refinance" or replace their FHA loan to remove their monthly mortgage insurance premium. Removing mortgage insurance premium by paying down the loan has become more difficult with FHA loans as of 2013.

In finance, negative amortization occurs whenever the loan payment for any period is less than the interest charged over that period so that the outstanding balance of the loan increases. As an amortization method the shorted amount is then added to the total amount owed to the lender. Such a practice would have to be agreed upon before shorting the payment so as to avoid default on payment. This method is generally used in an introductory period before loan payments exceed interest and the loan becomes self-amortizing. The term is most often used for mortgage loans; corporate loans with negative amortization are called PIK loans.

Also known as the "Sum of the Digits" method, the Rule of 78s is a term used in lending that refers to a method of yearly interest calculation. The name comes from the total number of months' interest that is being calculated in a year. This is an accurate interest model only based on the assumption that the borrower pays only the amount due each month. The outcome is that more of the interest is apportioned to the first part or early repayments than the later repayments. As such, the borrower pays a larger part of the total interest earlier in the term.

A balloon payment mortgage is a mortgage that does not fully amortize over the term of the note, thus leaving a balance due at maturity. The final payment is called a balloon payment because of its large size. Balloon payment mortgages are more common in commercial real estate than in residential real estate today due to the prevalence of mortgages with longer periods of amortization, in particular, the 30-year fixed-rate mortgages. A balloon payment mortgage may have a fixed or a floating interest rate. The most common way of describing a balloon loan uses the terminology X due in Y, where X is the number of years over which the loan is amortized, and Y is the year in which the principal balance is due.

An amortization calculator is used to determine the periodic payment amount due on a loan, based on the amortization process.

This article gives descriptions of mortgage terminology in the United Kingdom.

Mortgage calculators are automated tools that enable users to determine the financial implications of changes in one or more variables in a mortgage financing arrangement. Mortgage calculators are used by consumers to determine monthly repayments, and by mortgage providers to determine the financial suitability of a home loan applicant. Mortgage calculators are frequently on for-profit websites, though the Consumer Financial Protection Bureau has launched its own public mortgage calculator.

In the United States, a mortgage note is a promissory note secured by a specified mortgage loan.

In banking and finance, an amortizing loan is a loan where the principal of the loan is paid down over the life of the loan according to an amortization schedule, typically through equal payments.

A mortgage loan or simply mortgage, in civil law jurisdictions known also as a hypothec loan, is a loan used either by purchasers of real property to raise funds to buy real estate, or by existing property owners to raise funds for any purpose while putting a lien on the property being mortgaged. The loan is "secured" on the borrower's property through a process known as mortgage origination. This means that a legal mechanism is put into place which allows the lender to take possession and sell the secured property to pay off the loan in the event the borrower defaults on the loan or otherwise fails to abide by its terms. The word mortgage is derived from a Law French term used in Britain in the Middle Ages meaning "death pledge" and refers to the pledge ending (dying) when either the obligation is fulfilled or the property is taken through foreclosure. A mortgage can also be described as "a borrower giving consideration in the form of a collateral for a benefit (loan)".

Terms pertaining to American mortgages include:

Analogous to continuous compounding, a continuous annuity is an ordinary annuity in which the payment interval is narrowed indefinitely. A (theoretical) continuous repayment mortgage is a mortgage loan paid by means of a continuous annuity.

An equated monthly installment (EMI) is defined by Investopedia as "A fixed payment amount made by a borrower to a lender at a specified date each calendar month. Equated monthly installments are used to pay off both interest and principal each month, so that over a specified number of years, the loan is fully paid off along with interest."

In investment, an annuity is a series of payments made at equal intervals. Examples of annuities are regular deposits to a savings account, monthly home mortgage payments, monthly insurance payments and pension payments. Annuities can be classified by the frequency of payment dates. The payments (deposits) may be made weekly, monthly, quarterly, yearly, or at any other regular interval of time. Annuities may be calculated by mathematical functions known as "annuity functions".