Related Research Articles

"The Nature of the Firm" (1937) is an article by Ronald Coase. It offered an economic explanation of why individuals choose to form partnerships, companies, and other business entities rather than trading bilaterally through contracts on a market. The author was awarded the Nobel Memorial Prize in Economic Sciences in 1991 in part due to this paper. Despite the honor, the paper was written when Coase was an undergraduate and he described it later in life as "little more than an undergraduate essay."

In economics and related disciplines, a transaction cost is a cost in making any economic trade when participating in a market. The idea that transactions form the basis of economic thinking was introduced by the institutional economist John R. Commons in 1931, and Oliver E. Williamson's Transaction Cost Economics article, published in 2008, popularized the concept of transaction costs. Douglass C. North argues that institutions, understood as the set of rules in a society, are key in the determination of transaction costs. In this sense, institutions that facilitate low transaction costs, boost economic growth.

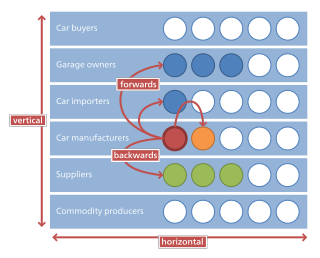

In microeconomics, management and international political economy, vertical integration is an arrangement in which the supply chain of a company is integrated and owned by that company. Usually each member of the supply chain produces a different product or (market-specific) service, and the products combine to satisfy a common need. It contrasts with horizontal integration, wherein a company produces several items that are related to one another. Vertical integration has also described management styles that bring large portions of the supply chain not only under a common ownership but also into one corporation.

From a legal point of view, a contract is an institutional arrangement for the way in which resources flow, which defines the various relationships between the parties to a transaction or limits the rights and obligations of the parties.

A complete contract is an important concept from contract theory.

In law and economics, the Coase theorem describes the economic efficiency of an economic allocation or outcome in the presence of externalities. The theorem is significant because, if true, the conclusion is that it is possible for private individuals to make choices that can solve the problem of market externalities. The theorem states that if the provision of a good or service results in an externality and trade in that good or service is possible, then bargaining will lead to a Pareto efficient outcome regardless of the initial allocation of property. A key condition for this outcome is that there are sufficiently low transaction costs in the bargaining and exchange process. This 'theorem' is commonly attributed to Nobel Prize laureate Ronald Coase.

State ownership, also called public ownership or government ownership, is the ownership of an industry, asset, or enterprise by the state or a public body representing a community, as opposed to an individual or private party. Public ownership specifically refers to industries selling goods and services to consumers and differs from public goods and government services financed out of a government's general budget. Public ownership can take place at the national, regional, local, or municipal levels of government; or can refer to non-governmental public ownership vested in autonomous public enterprises. Public ownership is one of the three major forms of property ownership, differentiated from private, collective/cooperative, and common ownership.

Build–operate–transfer (BOT) or build–own–operate–transfer (BOOT) is a form of project delivery method, usually for large-scale infrastructure projects, wherein a private entity receives a concession from the public sector to finance, design, construct, own, and operate a facility stated in the concession contract. The private entity will have the right to operate it for a set period of time. This enables the project proponent to recover its investment and operating and maintenance expenses in the project.

An option contract, or simply option, is defined as "a promise which meets the requirements for the formation of a contract and limits the promisor's power to revoke an offer". Option contracts are common in relation to property and in professional sports.

The theory of the firm consists of a number of economic theories that explain and predict the nature of the firm, company, or corporation, including its existence, behaviour, structure, and relationship to the market. Firms are key drivers in economics, providing goods and services in return for monetary payments and rewards. Organisational structure, incentives, employee productivity, and information all influence the successful operation of a firm in the economy and within itself. As such major economic theories such as transaction cost theory, managerial economics and behavioural theory of the firm will allow for an in-depth analysis on various firm and management types.

In economics, the hold-up problem is central to the theory of incomplete contracts, and shows the difficulty in writing complete contracts. A hold-up problem arises when two factors are present:

- Parties to a future transaction must make noncontractible relationship-specific investments before the transaction takes place.

- The specific form of the optimal transaction cannot be determined with certainty beforehand.

Common ownership refers to holding the assets of an organization, enterprise or community indivisibly rather than in the names of the individual members or groups of members as common property.

Sanford "Sandy" Jay Grossman is an American economist and hedge fund manager specializing in quantitative finance. Grossman’s research has spanned the analysis of information in securities markets, corporate structure, property rights, and optimal dynamic risk management. He has published widely in leading economic and business journals, including American Economic Review, Journal of Econometrics, Econometrica, and Journal of Finance. His research in macroeconomics, finance, and risk management has earned numerous awards. Grossman is currently Chairman and CEO of QFS Asset Management, an affiliate of which he founded in 1988. QFS Asset Management shut down its sole remaining hedge fund in January 2014.

Sir Oliver Simon D'Arcy Hart is a British-born American economist, currently the Lewis P. and Linda L. Geyser University Professor at Harvard University. Together with Bengt R. Holmström, he received the Nobel Memorial Prize in Economic Sciences in 2016.

New Institutional Economics (NIE) is an economic perspective that attempts to extend economics by focusing on the institutions that underlie economic activity and with analysis beyond earlier institutional economics and neoclassical economics. Unlike neoclassical economics, it also considers the role of culture and classical political economy in economic development.

Bengt Robert Holmström is a Finnish economist who is currently Paul A. Samuelson Professor of Economics (Emeritus) at the Massachusetts Institute of Technology. Together with Oliver Hart, he received the Central Bank of Sweden Nobel Memorial Prize in Economic Sciences in 2016.

Property rights are constructs in economics for determining how a resource or economic good is used and owned, which have developed over ancient and modern history, from Abrahamic law to Article 17 of the Universal Declaration of Human Rights. Resources can be owned by individuals, associations, collectives, or governments.

Innovation management is a combination of the management of innovation processes, and change management. It refers to product, business process, marketing and organizational innovation. Innovation management is the subject of ISO 56000 series standards being developed by ISO TC 279.

Organizational economics involves the use of economic logic and methods to understand the existence, nature, design, and performance of organizations, especially managed ones.

Yeon-Koo Che (Korean: 최연구) is a Korean American economist. He is the Kelvin J. Lancaster Professor of Economic Theory at Columbia University, a position he held since 2009. Prior to joining Columbia in 2005, he was a professor at University of Wisconsin-Madison.

References

- 1 2 Eisenberg, Melvin A. (2018), "Incomplete Contracts", Foundational Principles of Contract Law, New York: Oxford University Press, doi:10.1093/oso/9780199731404.003.0036, ISBN 978-0-19-973140-4 , retrieved 2022-04-25

- ↑ Karen Eggleston, Eric A Posner and Richard Zeckhauser (2000). "The Design and Interpretation of Contracts: Why Complexity Matters". 95 Northwestern University Law Review 91.

- 1 2 Aghion, Philippe; Holden, Richard (2011-05-01). "Incomplete Contracts and the Theory of the Firm: What Have We Learned over the Past 25 Years?". Journal of Economic Perspectives. 25 (2): 181–197. doi: 10.1257/jep.25.2.181 . ISSN 0895-3309.

- 1 2 Sanga, Sarath (2018-11-01). "Incomplete Contracts: An Empirical Approach". The Journal of Law, Economics, and Organization. 34 (4): 650–679. doi: 10.1093/jleo/ewy012 . ISSN 8756-6222.

- ↑ "Keay, Andrew; Zhang, Hao --- "Incomplete Contracts, Contingent Fiduciaries and a Director's Duty to Creditors" [2008] MelbULawRw 5; (2008) 32(1) Melbourne University Law Review 141". www5.austlii.edu.au. Retrieved 2022-04-25.

- ↑ Grossman, Sanford J.; Hart, Oliver D. (1986). "The costs and benefits of ownership: A theory of vertical and lateral integration". Journal of Political Economy. 94 (4): 691–719. doi:10.1086/261404. hdl: 1721.1/63378 .

- ↑ Hart, Oliver D.; Moore, John (1990). "Property Rights and the Nature of the Firm". Journal of Political Economy. 98 (6): 1119–58. CiteSeerX 10.1.1.472.9089 . doi:10.1086/261729.

- ↑ Hart, Oliver (1995). Firms, Contracts, and Financial Structure. Oxford University Press.

- ↑ Schmitz, Patrick W. (2001). "The Hold-Up Problem and Incomplete Contracts: A Survey of Recent Topics in Contract Theory" (PDF). Bulletin of Economic Research. 53 (1): 1–17. doi:10.1111/1467-8586.00114. ISSN 1467-8586.

- ↑ Coase, R. H. (1937). "The Nature of the Firm". Economica. 4 (16): 386–405. doi:10.1111/j.1468-0335.1937.tb00002.x. ISSN 1468-0335.

- ↑ Maskin, Eric; Tirole, Jean (1999). "Unforeseen Contingencies and Incomplete Contracts". The Review of Economic Studies. 66 (1): 83–114. doi:10.1111/1467-937X.00079. ISSN 0034-6527.

- ↑ Hart, Oliver; Moore, John (1999). "Foundations of Incomplete Contracts" (PDF). The Review of Economic Studies. 66 (1): 115–138. doi:10.1111/1467-937X.00080. ISSN 0034-6527.

- ↑ Tirole, Jean (1999). "Incomplete Contracts: Where do We Stand?". Econometrica. 67 (4): 741–781. CiteSeerX 10.1.1.465.9450 . doi:10.1111/1468-0262.00052. ISSN 1468-0262.

- ↑ Schmitz, Patrick W. (2005). "Allocating Control in Agency Problems with Limited Liability and Sequential Hidden Actions". RAND Journal of Economics. 36 (2): 318–336. JSTOR 4135244.

- ↑ Williamson, Oliver E (2000). "The New Institutional Economics: Taking Stock, Looking Ahead". Journal of Economic Literature. 38 (3): 595–613. CiteSeerX 10.1.1.128.7824 . doi:10.1257/jel.38.3.595. ISSN 0022-0515.

- ↑ Schmitz, Patrick W (2006). "Information Gathering, Transaction Costs, and the Property Rights Approach". American Economic Review. 96 (1): 422–434. doi:10.1257/000282806776157722. ISSN 0002-8282.

- ↑ Chiu, Y. Stephen (1998). "Noncooperative Bargaining, Hostages, and Optimal Asset Ownership". American Economic Review. 88 (4): 882–901. JSTOR 117010.

- ↑ Meza, David de; Lockwood, Ben (1998). "Does Asset Ownership Always Motivate Managers? Outside Options and the Property Rights Theory of the Firm". The Quarterly Journal of Economics. 113 (2): 361–386. doi:10.1162/003355398555621. ISSN 0033-5533.

- ↑ Hart, Oliver; Moore, John (2008). "Contracts as Reference Points". Quarterly Journal of Economics. 123 (1): 1–48. CiteSeerX 10.1.1.486.3894 . doi:10.1162/qjec.2008.123.1.1. JSTOR 25098893.

- ↑ Hart, Oliver; Shleifer, Andrei; Vishny, Robert W. (1997). "The Proper Scope of Government: Theory and an Application to Prisons". The Quarterly Journal of Economics. 112 (4): 1127–1161. doi:10.1162/003355300555448. ISSN 0033-5533.

- ↑ Hoppe, Eva I.; Schmitz, Patrick W. (2010). "Public versus private ownership: Quantity contracts and the allocation of investment tasks". Journal of Public Economics. 94 (3–4): 258–268. doi:10.1016/j.jpubeco.2009.11.009.

- ↑ Antràs, Pol; Staiger, Robert W (2012). "Offshoring and the Role of Trade Agreements". American Economic Review. 102 (7): 3140–3183. doi:10.1257/aer.102.7.3140. ISSN 0002-8282.

- ↑ Ornelas, Emanuel; Turner, John L. (2012). "Protection and International Sourcing*" (PDF). The Economic Journal. 122 (559): 26–63. doi:10.1111/j.1468-0297.2011.02462.x. ISSN 1468-0297.

- ↑ Aghion, Philippe; Tirole, Jean (1994). "The Management of Innovation". The Quarterly Journal of Economics. 109 (4): 1185–1209. doi:10.2307/2118360. ISSN 0033-5533. JSTOR 2118360.

- ↑ Rosenkranz, Stephanie; Schmitz, Patrick W. (2003). "Optimal allocation of ownership rights in dynamic R&D alliances". Games and Economic Behavior. 43 (1): 153–173. doi:10.1016/S0899-8256(02)00553-5.

- ↑ Aghion, Philippe; Tirole, Jean (1997). "Formal and Real Authority in Organizations". Journal of Political Economy. 105 (1): 1–29. CiteSeerX 10.1.1.558.3199 . doi:10.1086/262063. ISSN 0022-3808.

- ↑ Dewatripont, Mathias; Tirole, Jean (1999). "Advocates". Journal of Political Economy. 107 (1): 1–39. doi:10.1086/250049. JSTOR 10.1086/250049.

- ↑ "The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2016".

- ↑ Moore, John; Hart, Oliver (2007). "Incomplete Contracts and Ownership: Some New Thoughts". American Economic Review. 97 (2): 182–186. doi:10.1257/aer.97.2.182.

- ↑ Moore, John (2016), Aghion, Philippe; Dewatripont, Mathias; Legros, Patrick; Zingales, Luigi (eds.), "Introductory Remarks on Grossman and Hart (1986)", The Impact of Incomplete Contracts on Economics, New York: Oxford University Press, doi:10.1093/acprof:oso/9780199826223.001.0001, ISBN 978-0-19-982622-3 , retrieved 2022-04-27

- 1 2 Holmström, Bengt (2016), Aghion, Philippe; Dewatripont, Mathias; Legros, Patrick; Zingales, Luigi (eds.), "Grossman-Hart (1986) as a Theory of Markets", The Impact of Incomplete Contracts on Economics, New York: Oxford University Press, doi:10.1093/acprof:oso/9780199826223.001.0001, ISBN 978-0-19-982622-3 , retrieved 2022-04-26

- ↑ Hart, Oliver (2017). "Incomplete Contracts and Control". American Economic Review. 107 (7): 1731–1752. doi:10.1257/aer.107.7.1731. ISSN 0002-8282.

- ↑ Hart, Oliver; Moore, John (1990). "Property Rights and the Nature of the Firm". Journal of Political Economy. 98 (6): 1119–1158. doi:10.1086/261729. ISSN 0022-3808. JSTOR 2937753.

- ↑ Hart, Oliver; Moore, John (1990-12-01). "Property Rights and the Nature of the Firm". Journal of Political Economy. 98 (6): 1119–1158. doi:10.1086/261729. hdl: 1721.1/64099 . ISSN 0022-3808.

- ↑ Nickolas James (2014). BUSINESS LAW 4E. Wiley. p. 293.

- ↑ Seed annual 1906. Detroit, Mich: D.M. Ferry & Co. 1906. doi:10.5962/bhl.title.78573.

- ↑ Nickolas James (2014). BUSINESS LAW 4E. Wiley. p. 301.

- ↑ "Valid contracts—contracts which can be enforced against a minor Necessaries", Cavendish: Contract Lawcards, Routledge-Cavendish, pp. 123–128, 2004-01-09, doi:10.4324/9781843145493-34, ISBN 978-1-84314-549-3 , retrieved 2022-04-27

- ↑ "Bevins, Kenneth Milton, (2 Nov. 1918–30 June 2001), Director: Royal Insurance Co. Ltd, then Royal Insurance plc, 1970–88; Royal Insurance Holdings, 1988–89", Who Was Who, Oxford University Press, 2007-12-01, doi:10.1093/ww/9780199540884.013.u7462 , retrieved 2022-04-27

- ↑ "Parkinson, Frank, (1887–28 Jan. 1946), Chairman: Crompton Parkinson Ltd, British Electric Transformer Co. Ltd, and Derby Cables Ltd", Who Was Who, Oxford University Press, 2007-12-01, doi:10.1093/ww/9780199540884.013.u230160 , retrieved 2022-04-27

- ↑ "Pagan, Brig. Sir John (Ernest), (13 May 1914–26 June 1986), Chairman: P. Rowe Holdings Pty Ltd, since 1958; Associated National Insurance Co. Ltd, since 1973; Medicine Journal Pty Ltd; Nationale-Nederlanden (Aust.) Ltd; Deputy Chairman: NSW Permanent Building Society Ltd; Mercantile Mutual Holdings Ltd (Group); Director: Angus & Coote (Holdings) Ltd; H. M. Bates Pty Ltd; Rowetex Pty Ltd", Who Was Who, Oxford University Press, 2007-12-01, doi:10.1093/ww/9780199540884.013.u167807 , retrieved 2022-04-27

- ↑ Mcalevey, Lynn; Sibbald, Alexander; Tripe, David (2010-08-16). "New Zealand Credit Union Mergers". Annals of Public and Cooperative Economics. 81 (3): 423–444. doi:10.1111/j.1467-8292.2010.00414.x. ISSN 1370-4788.

- ↑ A.), Butler, D. A. (Des (7 February 2013). Contract law : case book. OUP Australia & New Zealand. ISBN 978-0-19-557847-8. OCLC 812861789.

{{cite book}}: CS1 maint: multiple names: authors list (link) - ↑ "Anderson, Janet, (born 6 Dec. 1949), Associate Consultant, Pandic (Political and Industrial Connections) Ltd, since 2012; Director, Pearson-Anderson Communications Ltd, since 2015", Who's Who, Oxford University Press, 2007-12-01, doi:10.1093/ww/9780199540884.013.u5459 , retrieved 2022-04-27

This article needs additional or more specific categories .(May 2021) |

| Authority control databases: National |

|---|