Related Research Articles

Insurance is a means of protection from financial loss in which, in exchange for a fee, a party agrees to compensate another party in the event of a certain loss, damage, or injury. It is a form of risk management, primarily used to protect against the risk of a contingent or uncertain loss.

Article One of the United States Constitution establishes the legislative branch of the federal government, the United States Congress. Under Article One, Congress is a bicameral legislature consisting of the House of Representatives and the Senate. Article One grants Congress various enumerated powers and the ability to pass laws "necessary and proper" to carry out those powers. Article One also establishes the procedures for passing a bill and places various limits on the powers of Congress and the states from abusing their powers.

McCulloch v. Maryland, 17 U.S. 316 (1819), was a landmark U.S. Supreme Court decision that defined the scope of the U.S. Congress's legislative power and how it relates to the powers of American state legislatures. The dispute in McCulloch involved the legality of the national bank and a tax that the state of Maryland imposed on it. In its ruling, the Supreme Court established firstly that the "Necessary and Proper" Clause of the U.S. Constitution gives the U.S. federal government certain implied powers necessary and proper for the exercise of the powers enumerated explicitly in the Constitution, and secondly that the American federal government is supreme over the states, and so states' ability to interfere with the federal government is restricted. Since the legislature has the authority to tax and spend, the court held that it therefore has authority to establish a national bank, as being "necessary and proper" to that end.

Obstruction of justice, in United States jurisdictions, is an act that involves unduly influencing, impeding, or otherwise interfering with the justice system, especially the legal and procedural tasks of prosecutors, investigators, or other government officials. Common law jurisdictions other than the United States tend to use the wider offense of perverting the course of justice.

The president of the Republic of Costa Rica is the head of state and head of government of Costa Rica. The president is currently elected in direct elections for a period of four years, which is not immediately renewable. Two vice presidents are elected in the same ticket with the president. The president appoints the Council of Ministers. Due to the abolition of the military of Costa Rica in 1948, the president is not a commander-in-chief, unlike the norm in most other countries, although the Constitution does describe him as commander-in-chief of the civil defense public forces.

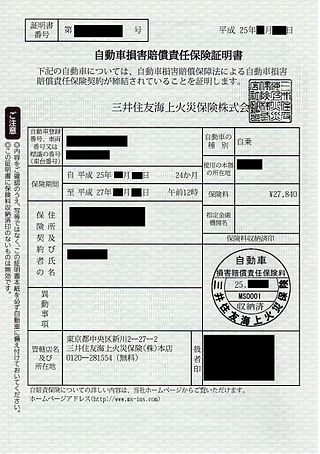

Vehicle insurance is insurance for cars, trucks, motorcycles, and other road vehicles. Its primary use is to provide financial protection against physical damage or bodily injury resulting from traffic collisions and against liability that could also arise from incidents in a vehicle. Vehicle insurance may additionally offer financial protection against theft of the vehicle, and against damage to the vehicle sustained from events other than traffic collisions, such as keying, weather or natural disasters, and damage sustained by colliding with stationary objects. The specific terms of vehicle insurance vary with legal regulations in each region.

The Privileges and Immunities Clause prevents a state from treating citizens of other states in a discriminatory manner. Additionally, a right of interstate travel is associated with the clause.

Marine insurance covers the physical loss or damage of ships, cargo, terminals, and any transport by which the property is transferred, acquired, or held between the points of origin and the final destination. Cargo insurance is the sub-branch of marine insurance, though marine insurance also includes onshore and offshore exposed property,, hull, marine casualty, and marine losses. When goods are transported by mail or courier or related post, shipping insurance is used instead.

An uninsured motorist clause is a provision commonly found in United States automobile insurance policies that provides for a driver to receive damages for any injury he or she receives from an uninsured, negligent driver. The owner of the policy pays a premium to the insurance company to include this clause. Although not exclusive, this coverage is typically added to an automobile insurance policy. In the event of a qualifying accident, the insurance company pays the difference between what the uninsured driver can pay and what the injured driver would be entitled to as if the uninsured motorist had proper insurance.

In law, severability refers to a provision in a contract or piece of legislation which states that if some of the terms are held to be illegal or otherwise unenforceable, the remainder should still apply. Sometimes, severability clauses will state that some provisions to the contract are so essential to the contract's purpose that if they are illegal or unenforceable, the contract as a whole will be voided. However, in many legal jurisdictions, a severability clause will not be applied if it changes the fundamental nature of the contract, and that instead the contract will be void; thus, often this is not explicitly stated in the severability clause.

In the law of the United States, federal preemption is the invalidation of a U.S. state law that conflicts with federal law.

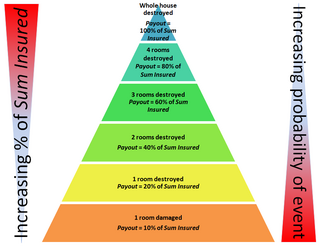

Condition of average is the insurance term used when calculating a payout against a claim where the policy undervalues the sum insured. In the event of partial loss, the amount paid against a claim will be in the same proportion as the value of the underinsurance.

In Canada, the term quasi-constitutional is used for laws which remain paramount even when subsequent statutes, which contradict them, are enacted by the same legislature. This is the reverse of the normal practice, under which newer laws trump any contradictory provisions in any older statute.

United States v. Munoz-Flores, 495 U.S. 385 (1990), was a United States Supreme Court case that interpreted the Origination Clause of the United States Constitution. The Court was asked to rule on whether a statute that imposed mandatory monetary penalties on persons convicted of federal misdemeanors was enacted in violation of that clause, as the lower court had held.

The Nonadmitted and Reinsurance Reform Act of 2010 is a United States law regulating the sale of insurance in states where the insurer is usually not authorized to sell insurance. It prevents states other than the home state of a U.S. insurance company from imposing regulations or taxes on the sale of nonadmitted insurance.

The administration of justice is the process by which the legal system of a government is executed. The presumed goal of such an administration is to provide justice for all those accessing the legal system.

Seaworthiness is a concept that runs through maritime law in at least four contractual relationships. In a marine insurance voyage policy, the assured warrants that the vessel is seaworthy. A carrier of goods by sea owes a duty to a shipper of cargo that the vessel is seaworthy at the start of the voyage. A shipowner warrants to a charterer that the vessel under charter is seaworthy; and similarly, a shipbuilder warrants that the vessel under construction will be seaworthy.

Yates v. United States, 574 U.S. 528 (2015), was a United States Supreme Court case in which the Court construed 18 U.S.C. § 1519, a provision added to the federal criminal code by the Sarbanes-Oxley Act, to criminalize the destruction or concealment of "any record, document, or tangible object" to obstruct a federal investigation. By a 5-to-4 vote, the Court stated that the term "tangible object" as used in this section means an object used to record or preserve information, and that this did not include fish.

Espinoza v. Montana Department of Revenue, 591 U.S. ___ (2020), was a landmark United States Supreme Court case in which the Court ruled that a state-based scholarship program that provides public funds to allow students to attend private schools cannot discriminate against religious schools under the Free Exercise Clause of the Constitution.

Corruptly obstructing, influencing, or impeding an official proceeding is a felony under U.S. federal law. It was enacted as part of the Sarbanes–Oxley Act of 2002 in reaction to the Enron scandal, and closed a legal loophole on who could be charged with evidence tampering by defining the new crime very broadly.

References

- Protection

- eVB Nummern (in German)