In production, research, retail, and accounting, a cost is the value of money that has been used up to produce something or deliver a service, and hence is not available for use anymore. In business, the cost may be one of acquisition, in which case the amount of money expended to acquire it is counted as cost. In this case, money is the input that is gone in order to acquire the thing. This acquisition cost may be the sum of the cost of production as incurred by the original producer, and further costs of transaction as incurred by the acquirer over and above the price paid to the producer. Usually, the price also includes a mark-up for profit over the cost of production.

Environmental full-cost accounting (EFCA) is a method of cost accounting that traces direct costs and allocates indirect costs by collecting and presenting information about the possible environmental, social and economical costs and benefits or advantages – in short, about the "triple bottom line" – for each proposed alternative. It is also known as true-cost accounting (TCA), but, as definitions for "true" and "full" are inherently subjective, experts consider both terms problematical.

An expense is an item requiring an outflow of money, or any form of fortune in general, to another person or group as payment for an item, service, or other category of costs. For a tenant, rent is an expense. For students or parents, tuition is an expense. Buying food, clothing, furniture, or an automobile is often referred to as an expense. An expense is a cost that is "paid" or "remitted", usually in exchange for something of value. Something that seems to cost a great deal is "expensive". Something that seems to cost little is "inexpensive". "Expenses of the table" are expenses for dining, refreshments, a feast, etc.

In finance, valuation is the process of determining the present value (PV) of an asset. In a business context, it is often the hypothetical price that a third party would pay for a given asset. Valuations can be done on assets or on liabilities. Valuations are needed for many reasons such as investment analysis, capital budgeting, merger and acquisition transactions, financial reporting, taxable events to determine the proper tax liability.

Total cost of ownership (TCO) is a financial estimate intended to help buyers and owners determine the direct and indirect costs of a product or service. It is a management accounting concept that can be used in full cost accounting or even ecological economics where it includes social costs.

Total benefits of ownership (TBO) is a calculation that tries to summarise the positive effects of the acquisition of a plan. It is an estimate of all the values that will affect a business.

Capital expenditure or capital expense is the money an organization or corporate entity spends to buy, maintain, or improve its fixed assets, such as buildings, vehicles, equipment, or land. It is considered a capital expenditure when the asset is newly purchased or when money is used towards extending the useful life of an existing asset, such as repairing the roof.

Consumption of fixed capital (CFC) is a term used in business accounts, tax assessments and national accounts for depreciation of fixed assets. CFC is used in preference to "depreciation" to emphasize that fixed capital is used up in the process of generating new output, and because unlike depreciation it is not valued at historic cost but at current market value ; CFC may also include other expenses incurred in using or installing fixed assets beyond actual depreciation charges. Normally the term applies only to producing enterprises, but sometimes it applies also to real estate assets.

A business case captures the reasoning for initiating a project or task. It is often presented in a well-structured written document, but may also come in the form of a short verbal agreement or presentation. The logic of the business case is that, whenever resources such as money or effort are consumed, they should be in support of a specific business need. An example could be that a software upgrade might improve system performance, but the "business case" is that better performance would improve customer satisfaction, require less task processing time, or reduce system maintenance costs. A compelling business case adequately captures both the quantifiable and non-quantifiable characteristics of a proposed project.

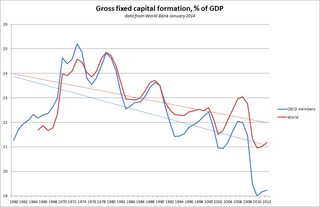

Gross fixed capital formation (GFCF) is a macroeconomic concept used in official national accounts such as the United Nations System of National Accounts (UNSNA), National Income and Product Accounts (NIPA) and the European System of Accounts (ESA). The concept dates back to the National Bureau of Economic Research (NBER) studies of Simon Kuznets of capital formation in the 1930s, and standard measures for it were adopted in the 1950s. Statistically it measures the value of acquisitions of new or existing fixed assets by the business sector, governments and "pure" households less disposals of fixed assets. GFCF is a component of the expenditure on gross domestic product (GDP), and thus shows something about how much of the new value added in the economy is invested rather than consumed.

Integrated logistic support (ILS) is a technology in the system engineering to lower a product life cycle cost and decrease demand for logistics by the maintenance system optimization to ease the product support. Although originally developed for military purposes, it is also widely used in commercial customer service organisations.

ISO 15686 is the in development ISO standard dealing with service life planning. It is a decision process which addresses the development of the service life of a building component, building or other constructed work like a bridge or tunnel. Its approach is to ensure a proposed design life has a structured response in establishing its service life normally from a reference or estimated service life framework. Then in turn secure a life-cycle cost profile whilst addressing environmental factors like life cycle assessment and service life care and end of life considerations including obsolescence and embodied energy recovery. Service life planning is increasingly being linked with sustainable development and wholelife value.

Intellectual property assets such as patents are the core of many organizations and transactions related to technology. Licenses and assignments of intellectual property rights are common operations in the technology markets, as well as the use of these types of assets as loan security. These uses give rise to the growing importance of financial valuation of intellectual property, since knowing the economic value of patents is a critical factor in order to define their trading conditions.

Asset management is a systematic approach to the governance and realization of value from the things that a group or entity is responsible for, over their whole life cycles. It may apply both to tangible assets and to intangible assets. Asset management is a systematic process of developing, operating, maintaining, upgrading, and disposing of assets in the most cost-effective manner.

For the application of engineering economics in the practice of civil engineering see Engineering economics.

IT Application Portfolio Management (APM) is a practice that has emerged in mid to large-size information technology (IT) organizations since the mid-1990s. Application Portfolio Management attempts to use the lessons of financial portfolio management to justify and measure the financial benefits of each application in comparison to the costs of the application's maintenance and operations.

An asset management plan (AMP) is a tactical plan for managing an organisation's infrastructure and other assets to deliver an agreed standard of service. Typically, an asset management plan will cover more than a single asset, taking a system approach - especially where a number of assets are co-dependent and are required to work together to deliver an agreed standard of service.

A reserve study is a long-term capital budget planning tool which identifies the current status of the reserve fund and a stable and equitable funding plan to offset ongoing deterioration, resulting in sufficient funds when those anticipated major common area expenditures actually occur. The reserve study consists of two parts: the physical analysis and the financial analysis. This document is often prepared by an outside independent consultant for the benefit of administrators of a property with multiple owners, such as a condominium association or homeowners' association (HOA), strata, containing an assessment of the state of the commonly owned property components as determined by the particular association's covenants, conditions, and restrictions (CC&Rs) and bylaws. Reserve studies however are not limited only to condominiums and can be created for any "common interest community" (CIC) properties such as resort properties, community/neighborhood associations, coops, etc.

IT risk management is the application of risk management methods to information technology in order to manage IT risk, i.e.:

Triple bottom line cost-benefit analysis (TBL-CBA) is an evidence-based economic method that combines cost–benefit analysis (CBA) and life-cycle cost analysis (LCCA) across the triple bottom line (TBL) to weigh costs and benefits to project stakeholders. The TBL-CBA process quantifies total net present value, return on investment, and project payback. TBL-CBA uses location-specific data to give asset owners and design professionals the flexibility and capability to provide a rigorous analysis of investment alternatives through all stages of planning and design.