The carry of an asset is the return obtained from holding it (if positive), or the cost of holding it (if negative) (see also Cost of carry).[1] For instance, commodities are usually negative carry assets, as they incur storage costs or may suffer from depreciation. (Imagine corn or wheat sitting in a silo somewhere, not being sold or eaten.) But in some circumstances, appropriately hedged commodities can be positive carry assets if the forward/futures market is willing to pay sufficient premium for future delivery. This can also refer to a trade with more than one leg, where you earn the spread between borrowing a low carry asset and lending a high carry one; such as gold during financial crisis, due to its safe haven quality.

Carry trades are not usually arbitrages: pure arbitrages make money no matter what; carry trades make money only if nothing changes against the carry's favor.

For instance, the traditional revenue stream from commercial banks is to borrow cheap (at the low overnight rate, i.e., the rate at which they pay depositors) and lend expensive (at the long-term rate, which is usually higher than the short-term rate). This works with an upward-sloping yield curve, but it loses money if the curve becomes inverted. Many investment banks, such as Bear Stearns, have failed because they borrowed cheap short-term money to fund higher interest bearing long-term positions. When the long-term positions default, or the short-term interest rate rises too high (or there are simply no lenders), the bank cannot meet its short-term liabilities and goes under.[2]

The currency carry trade is an uncovered interest arbitrage. The term carry trade, without further modification, refers to currency carry trade: investors borrow low-yielding currencies and lend (invest in) high-yielding currencies. It is thought to correlate with global financial and exchange rate stability and retracts in use during global liquidity shortages,[3] but the carry trade is often blamed for rapid currency value collapse and appreciation.

A risk in carry trading is that foreign exchange rates may change in such a way that the investor would have to pay back more expensive currency with less valuable currency. In theory, according to uncovered interest rate parity, carry trades should not yield a predictable profit because the difference in interest rates between two countries should equal the rate at which investors expect the low-interest-rate currency to rise against the high-interest-rate one. However, carry trades weaken the currency that is borrowed, because investors sell the borrowed money by converting it to other currencies.

By early year 2007, it was estimated that some US$1 trillion may have been staked on the yen carry trade.[4] Since the mid-1990s, the Bank of Japan has set Japanese interest rates at very low levels making it profitable to borrow Japanese yen to fund activities in other currencies.[5] These activities include subprime lending in the US, and funding of emerging markets, especially BRIC countries and resource rich countries. The trade largely collapsed in 2008 particularly in regard to the yen.

The European Central Bank extended its quantitative easing programme in December 2015. Accommodative ECB monetary policy made low-yielding EUR an often used funding currency for investment in risk assets. The EUR was gaining in times of market stress (such as falls in China stocks in January 2016), although it was not a traditional safe-haven currency.[6]

Most research on carry trade profitability was done using a large sample size of currencies.[7] However, small retail traders have access to limited currency pairs, which are mostly composed of the major G20 currencies, and experience reductions in yields after factoring in various costs and spreads.[8]

Known risks

The 2008–2011 Icelandic financial crisis has among its origins the undisciplined use of the carry trade. Particular attention has been focused on the use of Euro denominated loans to purchase homes and other assets within Iceland. Most of these loans defaulted when the relative value of the Icelandic currency depreciated dramatically, causing loan payment to be unaffordable.

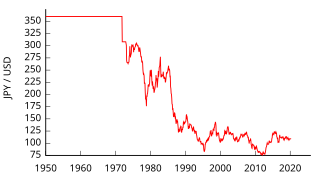

The US dollar and the Japanese yen have been the currencies most heavily used in carry trade transactions since the 1990s. There is some substantial mathematical evidence in macroeconomics that larger economies have more immunity to the disruptive aspects of the carry trade mainly due to the sheer quantity of their existing currency compared to the limited amount used for FOREX carry trades,[citation needed] but the collapse of the carry trade in 2008 is often blamed within Japan for a rapid appreciation of the yen. As a currency appreciates, there is pressure to cover any debts in that currency by converting foreign assets into that currency. This cycle can have an accelerating effect on currency valuation changes. When a large swing occurs, this can cause a carry reversal. The timing of the carry reversal in 2008 contributed substantially to the credit crunch which caused the 2008 global financial crisis, though relative size of impact of the carry trade with other factors is debatable. A similar rapid appreciation of the US dollar occurred at the same time, and the carry trade is rarely discussed as a factor for this appreciation.

Carry Trades and Speculative Dynamics by Guillaume Plantin and Hyun Song Shin, May 2010. Explains the dynamics of the carry trade by the example of Iceland and then goes on to develop a mathematical model for the exchange rate movements caused by carry trades.

Further reading

Lee, Tim; Lee, Jamie; Coldiron, Kevin (2020). The rise of carry: the dangerous consequences of volatility suppression and the new financial order of decaying growth and recurring crisis. New York. ISBN978-1-260-45841-1. OCLC1107844536.{{cite book}}: CS1 maint: location missing publisher (link)

Read, Charles (2022). Calming the storms: the carry trade, the banking school and British financial crises since 1825. Cham, Switzerland. ISBN978-3-031-11914-9. OCLC1360456914.{{cite book}}: CS1 maint: location missing publisher (link)

In economics and finance, arbitrage is the practice of taking advantage of a difference in prices in two or more markets; striking a combination of matching deals to capitalise on the difference, the profit being the difference between the market prices at which the unit is traded. When used by academics, an arbitrage is a transaction that involves no negative cash flow at any probabilistic or temporal state and a positive cash flow in at least one state; in simple terms, it is the possibility of a risk-free profit after transaction costs. For example, an arbitrage opportunity is present when there is the possibility to instantaneously buy something for a low price and sell it for a higher price.

Long-Term Capital Management L.P. (LTCM) was a highly leveraged hedge fund. In 1998, it received a $3.6 billion bailout from a group of 14 banks, in a deal brokered and put together by the Federal Reserve Bank of New York.

An interest rate is the amount of interest due per period, as a proportion of the amount lent, deposited, or borrowed. The total interest on an amount lent or borrowed depends on the principal sum, the interest rate, the compounding frequency, and the length of time over which it is lent, deposited, or borrowed.

In finance, an exchange rate is the rate at which one currency will be exchanged for another currency. Currencies are most commonly national currencies, but may be sub-national as in the case of Hong Kong or supra-national as in the case of the euro.

The money market is a component of the economy that provides short-term funds. The money market deals in short-term loans, generally for a period of a year or less.

In finance, a forward contract or simply a forward is a non-standardized contract between two parties to buy or sell an asset at a specified future time at a price agreed on at the time of conclusion of the contract, making it a type of derivative instrument. The party agreeing to buy the underlying asset in the future assumes a long position, and the party agreeing to sell the asset in the future assumes a short position. The price agreed upon is called the delivery price, which is equal to the forward price at the time the contract is entered into.

The foreign exchange market is a global decentralized or over-the-counter (OTC) market for the trading of currencies. This market determines foreign exchange rates for every currency. It includes all aspects of buying, selling and exchanging currencies at current or determined prices. In terms of trading volume, it is by far the largest market in the world, followed by the credit market.

Foreign exchange reserves are cash and other reserve assets such as gold held by a central bank or other monetary authority that are primarily available to balance payments of the country, influence the foreign exchange rate of its currency, and to maintain confidence in financial markets. Reserves are held in one or more reserve currencies, nowadays mostly the United States dollar and to a lesser extent the euro.

The impossible trinity is a concept in international economics and international political economy which states that it is impossible to have all three of the following at the same time:

Covered interest arbitrage is an arbitrage trading strategy whereby an investor capitalizes on the interest rate differential between two countries by using a forward contract to cover exchange rate risk. Using forward contracts enables arbitrageurs such as individual investors or banks to make use of the forward premium to earn a riskless profit from discrepancies between two countries' interest rates. The opportunity to earn riskless profits arises from the reality that the interest rate parity condition does not constantly hold. When spot and forward exchange rate markets are not in a state of equilibrium, investors will no longer be indifferent among the available interest rates in two countries and will invest in whichever currency offers a higher rate of return. Economists have discovered various factors which affect the occurrence of deviations from covered interest rate parity and the fleeting nature of covered interest arbitrage opportunities, such as differing characteristics of assets, varying frequencies of time series data, and the transaction costs associated with arbitrage trading strategies.

Interest rate parity is a no-arbitrage condition representing an equilibrium state under which investors interest rates available on bank deposits in two countries. The fact that this condition does not always hold allows for potential opportunities to earn riskless profits from covered interest arbitrage. Two assumptions central to interest rate parity are capital mobility and perfect substitutability of domestic and foreign assets. Given foreign exchange market equilibrium, the interest rate parity condition implies that the expected return on domestic assets will equal the exchange rate-adjusted expected return on foreign currency assets. Investors then cannot earn arbitrage profits by borrowing in a country with a lower interest rate, exchanging for foreign currency, and investing in a foreign country with a higher interest rate, due to gains or losses from exchanging back to their domestic currency at maturity. Interest rate parity takes on two distinctive forms: uncovered interest rate parity refers to the parity condition in which exposure to foreign exchange risk is uninhibited, whereas covered interest rate parity refers to the condition in which a forward contract has been used to cover exchange rate risk. Each form of the parity condition demonstrates a unique relationship with implications for the forecasting of future exchange rates: the forward exchange rate and the future spot exchange rate.

The Japanese asset price bubble was an economic bubble in Japan from 1986 to 1991 in which real estate and stock market prices were greatly inflated. In early 1992, this price bubble burst and Japan's economy stagnated. The bubble was characterized by rapid acceleration of asset prices and overheated economic activity, as well as an uncontrolled money supply and credit expansion. More specifically, over-confidence and speculation regarding asset and stock prices were closely associated with excessive monetary easing policy at the time. Through the creation of economic policies that cultivated the marketability of assets, eased the access to credit, and encouraged speculation, the Japanese government started a prolonged and exacerbated Japanese asset price bubble.

A financial crisis is any of a broad variety of situations in which some financial assets suddenly lose a large part of their nominal value. In the 19th and early 20th centuries, many financial crises were associated with banking panics, and many recessions coincided with these panics. Other situations that are often called financial crises include stock market crashes and the bursting of other financial bubbles, currency crises, and sovereign defaults. Financial crises directly result in a loss of paper wealth but do not necessarily result in significant changes in the real economy.

The following outline is provided as an overview of and topical guide to finance:

A structured investment vehicle (SIV) is a non-bank financial institution established to earn a credit spread between the longer-term assets held in its portfolio and the shorter-term liabilities it issues. They are simple credit spread lenders, frequently "lending" by investing in securitizations, but also by investing in corporate bonds and funding by issuing commercial paper and medium term notes, which were usually rated AAA until the onset of the financial crisis. They did not expose themselves to either interest rate or currency risk and typically held asset to maturity. SIVs differ from asset-backed securities and collateralized debt obligations in that they are permanently capitalized and have an active management team.

Endaka or Endaka Fukyo is a state in which the value of the Japanese yen is high compared to other currencies. Since the economy of Japan is highly dependent on exports, this can cause Japan to fall into an economic recession.

Currency intervention, also known as foreign exchange market intervention or currency manipulation, is a monetary policy operation. It occurs when a government or central bank buys or sells foreign currency in exchange for its own domestic currency, generally with the intention of influencing the exchange rate and trade policy.

Fixed-Income Relative-Value Investing (FI-RV) is a hedge fund investment strategy made popular by the failed hedge fund Long-Term Capital Management. FI-RV Investors most commonly exploit interest-rate anomalies in the large, liquid markets of North America, Europe and the Pacific Rim. The financial instruments traded include government bonds, interest rate swaps and futures contracts.

Leverage is defined as the ratio of the asset value to the cash needed to purchase it. The leverage cycle can be defined as the procyclical expansion and contraction of leverage over the course of the business cycle. The existence of procyclical leverage amplifies the effect on asset prices over the business cycle.

Mrs. Watanabe is a term that gained prominence in the early 2000s, representing a stereotype associated with Japanese retail traders, particularly housewives. These individuals became notable for their active participation in currency trading (Forex), which had a significant impact on global currency markets and garnered attention on a worldwide scale.

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.