A local exchange trading system is a locally initiated, democratically organised, not-for-profit community enterprise that provides a community information service and records transactions of members exchanging goods and services by using locally created currency. LETS allow people to negotiate the value of their own hours or services, and to keep wealth in the locality where it is created.

Mobile payment, also referred to as mobile money, mobile money transfer and mobile wallet, is any of various payment processing services operated under financial regulations and performed from or via a mobile device. Instead of paying with cash, cheque, or credit card, a consumer can use a payment app on a mobile device to pay for a wide range of services and digital or hard goods. Although the concept of using non-coin-based currency systems has a long history, it is only in the 21st century that the technology to support such systems has become widely available.

A micropayment is a financial transaction involving a very small sum of money and usually one that occurs online. A number of micropayment systems were proposed and developed in the mid-to-late 1990s, all of which were ultimately unsuccessful. A second generation of micropayment systems emerged in the 2010s.

Online banking, also known as internet banking, virtual banking, web banking or home banking, is a system that enables customers of a bank or other financial institution to conduct a range of financial transactions through the financial institution's website or mobile app. Since the early 2000s this has become the most common way that customers access their bank accounts.

An e-commerce payment system facilitates the acceptance of electronic payment for offline transfer, also known as a subcomponent of electronic data interchange (EDI), e-commerce payment systems have become increasingly popular due to the widespread use of the internet-based shopping and banking.

A complementary currency is a currency or medium of exchange that is not necessarily a national currency, but that is thought of as supplementing or complementing national currencies. Complementary currencies are usually not legal tender and their use is based on agreement between the parties exchanging the currency. According to Jérôme Blanc of Laboratoire d'Économie de la Firme et des Institutions, complementary currencies aim to protect, stimulate or orientate the economy. They may also be used to advance particular social, environmental, or political goals.

Fiserv, Inc. is an American multinational company headquartered in Milwaukee, Wisconsin, that provides financial technology and services to clients across the financial services sector, including banks, thrifts, credit unions, securities broker dealers, mortgage, insurance, leasing and finance companies, and retailers.

Mobile banking is a service provided by a bank or other financial institution that allows its customers to conduct financial transactions remotely using a mobile device such as a smartphone or tablet. Unlike the related internet banking it uses software, usually called an app, provided by the financial institution for the purpose. Mobile banking is usually available on a 24-hour basis. Some financial institutions have restrictions on which accounts may be accessed through mobile banking, as well as a limit on the amount that can be transacted. Mobile banking is dependent on the availability of an internet or data connection to the mobile device.

Gemalto was an international digital security company providing software applications, secure personal devices such as smart cards and tokens, e-wallets and managed services. It was formed in June 2006 by the merger of two companies, Axalto and Gemplus International. Gemalto N.V.'s revenue in 2018 was €2.969 billion.

The Malaysian Electronic Payment System (MEPS) is an interbank network service provider in Malaysia. In August 2017, MEPS merged with Malaysian Electronic Clearing Corporation Sdn Bhd (MyClear) to form Payments Network Malaysia Sdn Bhd (PayNet).

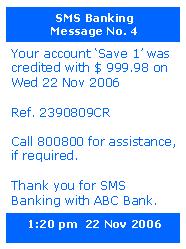

SMS banking' is a form of mobile banking. It is a facility used by some banks or other financial institutions to send messages to customers' mobile phones using SMS messaging, or a service provided by them which enables customers to perform some financial transactions using SMS.

Instrodi is a branch of the Social Trade Organization (STRO) in Brazil. STRO is an NGO from the Netherlands.

Man-in-the-browser, a form of Internet threat related to man-in-the-middle (MITM), is a proxy Trojan horse that infects a web browser by taking advantage of vulnerabilities in browser security to modify web pages, modify transaction content or insert additional transactions, all in a covert fashion invisible to both the user and host web application. A MitB attack will be successful irrespective of whether security mechanisms such as SSL/PKI and/or two- or three-factor authentication solutions are in place. A MitB attack may be countered by using out-of-band transaction verification, although SMS verification can be defeated by man-in-the-mobile (MitMo) malware infection on the mobile phone. Trojans may be detected and removed by antivirus software;, but a 2011 report concluded that additional measures on top of antivirus software were needed.

A payment processor is a system that enables financial transactions, commonly employed by a merchant, to handle transactions with customers from various channels such as credit cards and debit cards or bank accounts. They are usually broken down into two types: front-end and back-end.

M-PESA is a mobile phone-based money transfer service, payments and micro-financing service, launched in 2007 by Vodafone and Safaricom, the largest mobile network operator in Kenya. It has since expanded to Tanzania, Mozambique, DRC, Lesotho, Ghana, Egypt, Afghanistan, South Africa and Ethiopia. The rollouts in India, Romania, and Albania were terminated amid low market uptake. M-PESA allows users to deposit, withdraw, transfer money, pay for goods and services, access credit and savings, all with a mobile device.

The National Payments Corporation of India (NPCI) is an organization that operates retail payments and settlement systems in India. The organization is an initiative of the Reserve Bank of India (RBI) and the Indian Banks' Association (IBA) under the provisions of the Payment and Settlement Systems Act, 2007, for creating a robust payment and settlement infrastructure in India.

Natech is a global technology company specializing in software and services for the financial sector.

ACI Worldwide Inc. is a payment systems company headquartered in Miami, Florida. ACI develops a broad line of software focused on facilitating real-time electronic payments. These products and services are used globally by banks, financial intermediaries such as third-party electronic payment processors, payment associations, switch interchanges, merchants, corporations, and a wide range of transaction-generating endpoints, including automated teller machines ("ATM"), merchant point of sale ("POS") terminals, bank branches, mobile phones, tablet computers, corporations, and internet commerce sites.

KlickEx is a New Zealand fintech company that provides a payment system for domestic, low value electronic foreign exchange transactions to Polynesian countries using a smart market retail system.

Stellar, or Stellar Lumens, is an open-source, decentralized protocol for digital currency to fiat money low-cost transfers which allows cross-border transactions between any pair of currencies. The Stellar protocol is supported by a Delaware nonprofit corporation, the Stellar Development Foundation, though this organization does not enjoy 501(c)(3) tax-exempt status with the IRS.