The Armenian economy contracted sharply in 2020, by 5.7%, mainly due to the 2020 Armenia-Azerbaijan war. In contrast it grew by 7.6 per cent in 2019, the largest recorded growth since 2007, while between 2012 and 2018 GDP grew 40.7%, and key banking indicators like assets and credit exposures almost doubled.

The economy of Bulgaria functions on the principles of the free market, having a large private sector and a smaller public one. Bulgaria is an industrialised high-income country according to the World Bank, and is a member of the European Union (EU), the World Trade Organization (WTO), the Organization for Security and Co-operation in Europe (OSCE) and the Organization of the Black Sea Economic Cooperation (BSEC). The Bulgarian economy has experienced significant growth (538%), starting from $13.15 billion and reaching estimated gross domestic product (GDP) of $86 billion or $203 billion, GDP per capita of $31,148, average gross monthly salary of 1,771 leva, and average net monthly salary of $1,838 (2021). The national currency is the lev, pegged to the euro at a rate of 1.95583 leva for 1 euro. The lev is the strongest and most stable currency in Eastern Europe.

The balance of trade, commercial balance, or net exports, is the difference between the monetary value of a nation's exports and imports over a certain time period. Sometimes a distinction is made between a balance of trade for goods versus one for services. The balance of trade measures a flow of exports and imports over a given period of time. The notion of the balance of trade does not mean that exports and imports are "in balance" with each other.

The economy of Indonesia is the largest in Southeast Asia and is one of the emerging market economies. As a middle income country & member of the G20, Indonesia is classified as a newly industrialized country. It is the 17th largest economy in the world by nominal GDP and the 7th largest in terms of GDP (PPP). Estimated at US$40 billion in 2019, Indonesia's Internet economy is expected to cross the US$130 billion mark by 2025. Indonesia depends on domestic market and government budget spending and its ownership of state-owned enterprises. The administration of prices of a range of basic goods also plays a significant role in Indonesia's market economy. However, since the 1990s, the majority of the economy has been controlled by individual Indonesians and foreign companies.

The economy of Nicaragua is focused primarily on the agricultural sector. Nicaragua itself is the least developed country in Central America, and the second poorest in the Americas by nominal GDP. In recent years, under the administrations of Daniel Ortega, the Nicaraguan economy has expanded somewhat, following the Great Recession, when the country's economy actually contracted by 1.5%, due to decreased export demand in the American and Central American markets, lower commodity prices for key agricultural exports, and low remittance growth. The economy saw 4.5% growth in 2010 thanks to a recovery in export demand and growth in its tourism industry. Nicaragua's economy continues to post growth, with preliminary indicators showing the Nicaraguan economy growing an additional 5% in 2011. Consumer Price inflation have also curtailed since 2008, when Nicaragua's inflation rate hovered at 19.82%. In 2009 and 2010, the country posted lower inflation rates, 3.68% and 5.45%, respectively. Remittances are a major source of income, equivalent to 15% of the country's GDP, which originate primarily from Costa Rica, the United States, and European Union member states. Approximately one million Nicaraguans contribute to the remittance sector of the economy.

The economy of Paraguay is a market economy that is highly dependent on agriculture products. In recent years, Paraguay's economy has grown as a result of increased agricultural exports, especially soybeans. Paraguay has the economic advantages of a young population and vast hydroelectric power. Its disadvantages include the few available mineral resources, and political instability. The government welcomes foreign investment.

The economy of Yemen is one of the poorest and least-developed in the world. At the time of unification, South Yemen and North Yemen had vastly different but equally struggling underdeveloped economic systems. Since unification, the economy has been forced to sustain the consequences of Yemen's support for Iraq during the 1990–91 Persian Gulf War: Saudi Arabia expelled almost 1 million Yemeni workers, and both Saudi Arabia and Kuwait significantly reduced economic aid to Yemen. The 1994 civil war further drained Yemen's economy. As a consequence, Yemen has relied heavily on aid from multilateral agencies to sustain its economy for the past 24 years. In return, it has pledged to implement significant economic reforms. In 1997 the International Monetary Fund (IMF) approved two programs to increase Yemen's credit significantly: the enhanced structural adjustment facility and the extended funding facility (EFF). In the ensuing years, Yemen's government attempted to implement recommended reforms: reducing the civil service payroll, eliminating diesel and other subsidies, lowering defense spending, introducing a general sales tax, and privatizing state-run industries. However, limited progress led the IMF to suspend funding between 1999 and 2001.

In international economics, the balance of payments of a country is the difference between all money flowing into the country in a particular period of time and the outflow of money to the rest of the world. These financial transactions are made by individuals, firms and government bodies to compare receipts and payments arising out of trade of goods and services.

The trade policy of Japan related to Japan's approach to import and export with other countries.

In its balance of payments accounts, Japan has traditionally run a deficit in services. Trade in services includes transportation, insurance, travel expenditures, royalties, licensing fees, and income from investments. The deficit in services rose steadily from US$99 million in 1960, to nearly US$1.8 billion in 1970 and to more than US$11.3 billion in 1980 which can be attributed to rising royalty and licensing payments for Japan's acquisition of technology from other industrial countries and to rising deficits in the trade-related services of transportation and insurance. The transportation deficit rose after the 1960s, as rapidly climbing labor costs made Japanese-flag vessels less competitive, leading to greater use of foreign-flag carriers.

Capital began to flow in and out of Japan following the Meiji Restoration of 1868, but policy restricted loans from overseas. In the aftermath of World War II, Japan was a debtor nation until the mid-1960s. Subsequently, capital controls were progressively removed, in part as a result of agreements with the United States. This process led to rapid expansion of capital flows during the 1970s and especially the 1980s, when Japan became a creditor nation and the largest net investor in the world. This credit position resulted both from foreign direct investment by Japanese corporations, and portfolio investment. In particular, the rapid increase of Japan's direct investments overseas, much exceeding foreign investment in Japan, led to some tension with the US at the end of the 1980s.

The economic history of the Republic of Turkey may be studied according to sub-periods signified with major changes in economic policy:

- 1923–1929, when development policy emphasised private accumulation;

- 1929–1945, when development policy emphasised state accumulation in a period of global crises;

- 1950–1980, a period of state guided industrialisation based on import substituting protectionism;

- 1980 onwards, opening of the Turkish economy to liberal trade in goods, services and financial market transactions.

Soviet foreign trade played only a minor role in the Soviet economy. In 1985, for example, exports and imports each accounted for only 4 percent of the Soviet gross national product. The Soviet Union maintained this low level because it could draw upon a large energy and raw material base, and because it historically had pursued a policy of self-sufficiency. Other foreign economic activity included economic aid programs, which primarily benefited the less developed Council for Mutual Economic Assistance (COMECON) countries of Cuba, Mongolia, and Vietnam.

Trade is a key factor of the economy of China. In the three decades following the formation of the Communist Chinese state in 1949, China's trade institutions at first developed into a partially modern but somewhat inefficient system. The drive to modernize the economy that began in 1978 required a sharp acceleration in commodity flows and greatly improved efficiency in economic transactions. In the ensuing years economic reforms were adopted by the government to develop a socialist market economy. This type of economy combined central planning with market mechanisms. The changes resulted in the decentralization and expansion of domestic and foreign trade institutions, as well as a greatly enlarged role for free market in the distribution of goods, and a prominent role for foreign trade and investment in economic development.

The economy of Algeria expanded by 1.4% in 2018, up from 4.1% in 2016 with growth driven mainly by the recovering oil and gas sector.

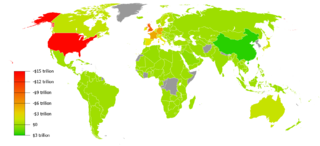

Foreign trade of the United States comprises the international imports and exports of the United States. The country is among the top three global importers and exporters.

The economic history of Ecuador covers the period of the economy of Ecuador in Ecuadoran history beginning with colonization by the Spanish Empire, through independence and up to modern-day.

Argentina is a developing country. Its economy is the second-largest national economy in South America, behind Brazil.

This article is intended to give an overview of the trade policy of South Korea. In 1945 Korea was liberated from the Empire of Japan at the end of World War II. A destructive drought in 1958 forced Korea to import large amounts of food grains. In 1950, the Korean war broke out, which destroyed more than two-thirds of the nation's production facilities and most of its infrastructure. Trade policy of South Korea has taken many shifts, from import substitution to globalization and there has been significant impact on the economy for the same.

This article is about the foreign trade of Sudan.