A tax is a compulsory financial charge or some other type of levy imposed on a taxpayer by a governmental organization in order to collectively fund government spending, public expenditures, or as a way to regulate and reduce negative externalities. Tax compliance refers to policy actions and individual behaviour aimed at ensuring that taxpayers are paying the right amount of tax at the right time and securing the correct tax allowances and tax relief. The first known taxation took place in Ancient Egypt around 3000–2800 BC. Taxes consist of direct or indirect taxes and may be paid in money or as its labor equivalent.

A flat tax is a tax with a single rate on the taxable amount, after accounting for any deductions or exemptions from the tax base. It is not necessarily a fully proportional tax. Implementations are often progressive due to exemptions, or regressive in case of a maximum taxable amount. There are various tax systems that are labeled "flat tax" even though they are significantly different. The defining characteristic is the existence of only one tax rate other than zero, as opposed to multiple non-zero rates that vary depending on the amount subject to taxation.

In addition to federal income tax collected by the United States, most individual U.S. states collect a state income tax. Some local governments also impose an income tax, often based on state income tax calculations. Forty-two states and many localities in the United States impose an income tax on individuals. Eight states impose no state income tax, and a ninth, New Hampshire, imposes an individual income tax on dividends and interest income but not other forms of income. Forty-seven states and many localities impose a tax on the income of corporations.

A use tax is a type of tax levied in the United States by numerous state governments. It is essentially the same as a sales tax but is applied not where a product or service was sold but where a merchant bought a product or service and then converted it for its own use, without having paid tax when it was initially purchased. Use taxes are functionally equivalent to sales taxes. They are typically levied upon the use, storage, enjoyment, or other consumption in the state of tangible personal property that has not been subjected to a sales tax.

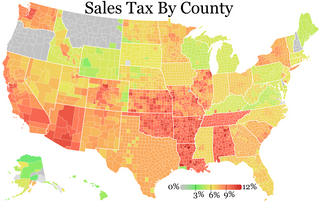

Sales taxes in the United States are taxes placed on the sale or lease of goods and services in the United States. Sales tax is governed at the state level and no national general sales tax exists. 45 states, the District of Columbia, the territories of Puerto Rico, and Guam impose general sales taxes that apply to the sale or lease of most goods and some services, and states also may levy selective sales taxes on the sale or lease of particular goods or services. States may grant local governments the authority to impose additional general or selective sales taxes.

As of January 1, 2013, the state of Ohio no longer imposes an estate tax on the transfer of assets from resident decedents. In previous years the rates and amounts varied. The 2012 tax rates are shown in the table below. Because of tax credits, the effective lower limit on taxable estates was $338,333. Ohio also allowed a "marital deduction" equal to the net value of any asset passing to the surviving spouse.

With God, all things are possible is the motto of the U.S. state of Ohio. Quoted from the Gospel of Matthew, verse 19:26, it is the only state motto taken directly from the Bible. It is defined in section 5.06 of the Ohio Revised Code and sometimes appears beneath the Seal of Ohio. The motto was adopted in 1959 and survived a federal constitutional challenge in 2001. The state maintains that it is a generic expression of optimism rather than an endorsement of a particular religion.

The New York State Department of Taxation and Finance (NYSDTF) is the department of the New York state government responsible for taxation and revenue, including handling all tax forms and publications, and dispersing tax revenue to other agencies and counties within New York State. The department also has a law enforcement division, the New York State Office of Tax Enforcement. Its regulations are compiled in title 20 of the New York Codes, Rules and Regulations.

Income taxes are the most significant form of taxation in Australia, and collected by the federal government through the Australian Taxation Office. Australian GST revenue is collected by the Federal government, and then paid to the states under a distribution formula determined by the Commonwealth Grants Commission.

A hotel tax or lodging tax is charged in most of the United States, to travelers when they rent accommodations in a hotel, inn, tourist home or house, motel, or other lodging, generally unless the stay is for a period of 30 days or more. In addition to sales tax, it is collected when payment is made for the accommodation, and it is then remitted by the lodging operator to the city or county. It can also be called hotel occupancy tax in places like New York City and Texas. Despite its name, it generally applies to the same range of accommodations.

Taxes in India are levied by the Central Government and the State Governments by virtue of powers conferred to them from the Constitution of India. Some minor taxes are also levied by the local authorities such as the Municipality.

A gross receipts tax or gross excise tax is a tax on the total gross revenues of a company, regardless of their source. A gross receipts tax is often compared to a sales tax; the difference is that a gross receipts tax is levied upon the seller of goods or services, while a sales tax is nominally levied upon the buyer. This is compared to other taxes listed as separate line items on billings, are not directly included in the listed price of the item, and are not a factor in markup or profit on company sales. A gross receipts tax has a pyramid effect that increases the actual taxable percentage as it passes through the product or service lifecycle.

The State Taxation Administration is a ministerial-level department within the government of the People's Republic of China. It is under the direction of the State Council, and is responsible for the collection of taxes and enforces the state revenue laws. Previously known as State Administration of Taxation.

The business and occupation tax is a type of tax levied by the U.S. states of Washington, West Virginia, and, as of 2010, Ohio, and by municipal governments in West Virginia and Kentucky.

Tax protester Sixteenth Amendment arguments are assertions that the imposition of the U.S. federal income tax is illegal because the Sixteenth Amendment to the United States Constitution, which reads "The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration", was never properly ratified, or that the amendment provides no power to tax income. Proper ratification of the Sixteenth Amendment is disputed by tax protesters who argue that the quoted text of the Amendment differed from the text proposed by Congress, or that Ohio was not a State during ratification, despite its admission to the Union on March 1, 1803, more than a century prior. Sixteenth Amendment ratification arguments have been rejected in every court case where they have been raised and have been identified as legally frivolous.

The Institute on Taxation and Economic Policy (ITEP) is a non-profit, liberal think tank that works on state and federal tax policy issues. ITEP was founded in 1980, and is a 501(c)(3) tax-exempt organization.

Taxation in Bhutan is conducted by the national government and by its subsidiary local governments. All taxation is ultimately overseen by the Bhutan Ministry of Finance, Department of Revenue and Customs, which is part of the executive Lhengye Zhungtshog (cabinet). The modern legal basis for taxation in Bhutan derives from legislation. Several acts provide for taxation and enforcement only germane to their subject matter and at various levels of government, while a smaller number provide more comprehensive substantive tax law. As a result, the tax scheme of Bhutan is highly decentralized.

The administrative divisions of Ohio are counties, municipalities, townships, special districts, and school districts.

Miller v. Korns (1923) is a significant legal case in the U.S. state of Ohio. It was one of the first Ohio Supreme Court cases to challenge the Ohio State General Assembly's system of school financing.