Related Research Articles

The Low-Income Housing Tax Credit (LIHTC) is a federal program in the United States that awards tax credits to housing developers in exchange for agreeing to reserve a certain fraction of rent-restricted units for lower-income households. The program was created under the Tax Reform Act of 1986 (TRA86) to incentivize the use of private equity in developing affordable housing. Projects developed with LIHTC credits must maintain a certain percentage of affordable units for a set period of time, typically 30 years, though there is a "qualified contract" process that can allow property owners to opt out after 15 years. The maximum rent that can be charged for designated affordable units is based on Area Median Income (AMI); over 50% of residents in LIHTC properties are considered Extremely Low-Income. Less than 10% of current credit expenditures are claimed by individual investors.

Section 8 of the Housing Act of 1937, often called Section 8, as repeatedly amended, authorizes the payment of rental housing assistance to private landlords on behalf of low-income households in the United States. 68% of total rental assistance in the United States goes to seniors, children, and those with disabilities. The U.S. Department of Housing and Urban Development manages Section 8 programs.

An FHA insured loan is a US Federal Housing Administration mortgage insurance backed mortgage loan that is provided by an FHA-approved lender. FHA mortgage insurance protects lenders against losses. They have historically allowed lower-income Americans to borrow money to purchase a home that they would not otherwise be able to afford. Because this type of loan is more geared towards new house owners than real estate investors, FHA loans are different from conventional loans in the sense that the house must be owner-occupant for at least a year. Since loans with lower down-payments usually involve more risk to the lender, the home-buyer must pay a two-part mortgage insurance that involves a one-time bulk payment and a monthly payment to compensate for the increased risk. Frequently, individuals "refinance" or replace their FHA loan to remove their monthly mortgage insurance premium. Removing mortgage insurance premium by paying down the loan has become more difficult with FHA loans as of 2013.

Canada Mortgage and Housing Corporation is Canada's federal crown corporation responsible for administering the National Housing Act, with the mandate to improve housing by living conditions in the country.

The Rural Housing Service (RHS) is an agency of the United States Department of Agriculture (USDA). Located within the Department's Rural Development mission area. RHS operates a broad range of programs to provide moderate- low- and very-low-income Americans in rural communities with:

Subsidized housing is government sponsored economic assistance aimed towards alleviating housing costs and expenses for impoverished people with low to moderate incomes. In the United States, subsidized housing is often called "affordable housing". Forms of subsidies include direct housing subsidies, non-profit housing, public housing, rent supplements/vouchers, and some forms of co-operative and private sector housing. According to some sources, increasing access to housing may contribute to lower poverty rates.

Public housing in Hong Kong is a set of mass housing programmes through which the Government of Hong Kong provides affordable housing for lower-income residents. It is a major component of housing in Hong Kong, with nearly half of the population now residing in some form of public housing. The public housing policy dates to 1954, after a fire in Shek Kip Mei destroyed thousands of shanty homes and prompted the government to begin constructing homes for the poor.

The HOME Investment Partnerships Program (HOME) is a type of United States federal assistance that the U.S. Department of Housing and Urban Development (HUD) provides to states to create decent and affordable housing, particularly housing for low and very low income Americans. It is the largest Federal block grant to states and local governments designed exclusively to create affordable housing for low-income families, providing approximately US$2 billion each year.

An individual development account (IDA) is an asset building tool designed to enable low-income families to save towards a targeted amount usually used for building assets in the form of home ownership, post-secondary education and small business ownership. In principle IDAs work as matched savings accounts that supplement the savings of low-income households with matching funds drawn from a variety of private and public sources.

The California Housing Finance Agency (CalHFA), established in 1975, is an independent California state agency within the California Department of Housing and Community Development that makes low-rate housing loans through the sale of taxable and tax exempt bonds.

In the United States, subsidized housing is administered by federal, state and local agencies to provide subsidized rental assistance for low-income households. Public housing is priced much below the market rate, allowing people to live in more convenient locations rather than move away from the city in search of lower rents. In most federally-funded rental assistance programs, the tenants' monthly rent is set at 30% of their household income. Now increasingly provided in a variety of settings and formats, originally public housing in the U.S. consisted primarily of one or more concentrated blocks of low-rise and/or high-rise apartment buildings. These complexes are operated by state and local housing authorities which are authorized and funded by the United States Department of Housing and Urban Development (HUD). In 2020, there were one million public housing units. In 2022, about 5.2 million American households that received some form of federal rental assistance.

Section 524 loans are land acquisition and development loans in the United States that are authorized under Section 524 of the federal Housing Act of 1949.

Section 502 loans are a rural housing loan program, administered by the Rural Housing Service (RHS), authorized under Section 502 of the Housing Act of 1949. Borrowers may obtain loans for purchasing or repairing new or existing single-family housing. Loans are made directly by RHS or by private lenders with a USDA guarantee. Borrowers with income of 80% or less of the area median may be eligible for 33- year direct loans and may receive payment assistance to bring the interest rate to as low as 1%. In a given fiscal year, at least 40% of the units financed under this section must be made available only to very low-income families or individuals. In addition, families or individuals at or below 60% of the area median may qualify for loan terms up to 38 years. Borrowers must have the means to repay the loans, but be unable to secure reasonable credit terms elsewhere. Borrowers with income of up to 115% of the area median may be eligible for 30-year guaranteed loans from private lenders. Priority is given to first-time home buyers, and the RHS may require that borrowers complete a home ownership counseling program.

Kentucky Housing Corporation (KHC), the Kentucky state housing agency, was created by the 1972 Kentucky General Assembly to provide affordable housing opportunities. KHC is a self-supporting, public corporation.

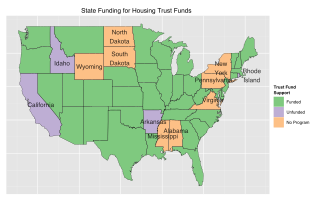

Housing trust funds are established sources of funding for affordable housing construction and other related purposes created by governments in the United States (U.S.). Housing Trust Funds (HTF) began as a way of funding affordable housing in the late 1970s. Since then, elected government officials from all levels of government in the U.S. have established housing trust funds to support the construction, acquisition, and preservation of affordable housing and related services to meet the housing needs of low-income households. Ideally, HTFs are funded through dedicated revenues like real estate transfer taxes or document recording fees to ensure a steady stream of funding rather than being dependent on regular budget processes. As of 2016, 400 state, local and county trust funds existed across the U.S.

Non-profit housing developers build affordable housing for individuals under-served by the private market. The non-profit housing sector is composed of community development corporations (CDC) and national and regional non-profit housing organizations whose mission is to provide for the needy, the elderly, working households, and others that the private housing market does not adequately serve. Of the total 4.6 million units in the social housing sector, non-profit developers have produced approximately 1.547 million units, or roughly one-third of the total stock. Since non-profit developers seldom have the financial resources or access to capital that for-profit entities do, they often use multiple layers of financing, usually from a variety of sources for both development and operation of these affordable housing units.

A USDA Home Loan from the USDA loan program, also known as the USDA Rural Development Guaranteed Housing Loan Program, is a mortgage loan offered to rural property owners by the United States Department of Agriculture, Rural Development.

Howard County Housing is the umbrella organization for the Howard County Department of Housing and Community Development and the Howard County Housing Commission. The Department is Howard County Government’s housing agency, and the Commission is a public housing authority and non-profit. Both have boards that meet monthly.

Pradhan Mantri Awas Yojana (PMAY) is a credit-linked subsidy scheme by the Government of India to facilitate access to affordable housing for the low and moderate-income residents of the country. It envisaged a target of building 2 crore (20 million) affordable houses by 31 March 2022. It has two components: Pradhan Mantri Awas Yojana(Urban) (PMAY-U) for the urban poor and Pradhan Mantri Awaas Yojana (Gramin) (PMAY-G and also PMAY-R) for the rural poor, the former administered by Ministry of Housing and Urban Affairs and the latter by Ministry of Rural Development. This scheme converges with other schemes to ensure that houses have a toilet, Saubhagya Scheme for universal electricity connection, Ujjwala Yojana LPG connection, access to drinking water and Jan Dhan banking facilities, etc.

Affordable housing is housing that is deemed affordable to those with a median household income as rated by the national government or a local government by a recognized housing affordability index. A general rule is no more than 30% of gross monthly income should be spent on housing, to be considered affordable as the challenges of promoting affordable housing varies by location.

References

This article incorporates public domain material from Jasper Womach. Report for Congress: Agriculture: A Glossary of Terms, Programs, and Laws, 2005 Edition (PDF). Congressional Research Service.

This article incorporates public domain material from Jasper Womach. Report for Congress: Agriculture: A Glossary of Terms, Programs, and Laws, 2005 Edition (PDF). Congressional Research Service.