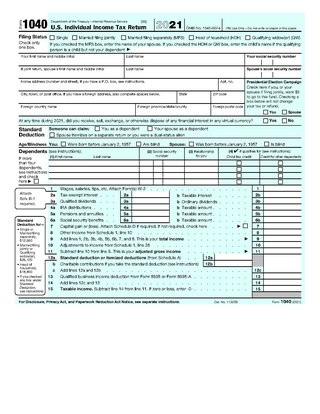

Form 1040, officially, the U.S. Individual Income Tax Return, is an IRS tax form used for personal federal income tax returns filed by United States residents. The form calculates the total taxable income of the taxpayer and determines how much is to be paid to or refunded by the government.

Tax returns in the United States are reports filed with the Internal Revenue Service (IRS) or with the state or local tax collection agency containing information used to calculate income tax or other taxes. Tax returns are generally prepared using forms prescribed by the IRS or other applicable taxing authority.

Tax returns in Canada refer to the obligatory forms that must be submitted to the Canada Revenue Agency (CRA) each financial year for individuals or corporations earning an income in Canada. The return paperwork reports the sum of the previous year's taxable income, tax credits, and other information relating to those two items. The return is the method by which the Canadian government determines the appropriate amount of tax that should be paid by individuals and corporations. The result of filing a return with the federal government can result in either a refund, or an amount due to be paid. There is a penalty for not filing a tax return.

The Canada Revenue Agency is the revenue service of the Canadian federal government, and most provincial and territorial governments. The CRA collects taxes, administers tax law and policy, and delivers benefit programs and tax credits. Legislation administered by the CRA includes the Income Tax Act, parts of the Excise Tax Act, and parts of laws relating to the Canada Pension Plan, employment insurance (EI), tariffs and duties. The agency also oversees the registration of charities in Canada, and enforces much of the country's tax laws.

A tax refund is a payment to the taxpayer due because the taxpayer has paid more tax than owed.

In the United Kingdom, a tax return is a document that must be filed with HM Revenue & Customs declaring liability for taxation. Different bodies must file different returns with respect to various forms of taxation. The main returns currently in use are:

An Individual Taxpayer Identification Number (ITIN) is a United States tax processing number issued by the Internal Revenue Service (IRS). It is a nine-digit number beginning with the number “9”, has a range of numbers from "50" to "65", "70" to "88", “90” to “92” and “94” to “99” for the fourth and fifth digits, and is formatted like a SSN. ITIN numbers are issued by the IRS to individuals who do not have and are not eligible to obtain a valid U.S. Social Security Number, but who are required by law to file a U.S. Individual Income Tax Return.

Form W-2 is an Internal Revenue Service (IRS) tax form used in the United States to report wages paid to employees and the taxes withheld from them. Employers must complete a Form W-2 for each employee to whom they pay a salary, wage, or other compensation as part of the employment relationship. An employer must mail out the Form W-2 to employees on or before January 31 of any year in which an employment relationship existed and which was not contractually independent. This deadline gives these taxpayers about 2 months to prepare their returns before the April 15 income tax due date. The form is also used to report FICA taxes to the Social Security Administration. Form W-2 along with Form W-3 generally must be filed by the employer with the Social Security Administration by the end of February following employment the previous year. Relevant amounts on Form W-2 are reported by the Social Security Administration to the Internal Revenue Service. In US territories, the W-2 is issued with a two letter territory code, such as W-2GU for Guam. Corrections can be filed using Form W-2c.

Form 1099 is one of several IRS tax forms used in the United States to prepare and file an information return to report various types of income other than wages, salaries, and tips. The term information return is used in contrast to the term tax return although the latter term is sometimes used colloquially to describe both kinds of returns.

Tax withholding, also known as tax retention, pay-as-you-earn tax or tax deduction at source, is income tax paid to the government by the payer of the income rather than by the recipient of the income. The tax is thus withheld or deducted from the income due to the recipient. In most jurisdictions, tax withholding applies to employment income. Many jurisdictions also require withholding taxes on payments of interest or dividends. In most jurisdictions, there are additional tax withholding obligations if the recipient of the income is resident in a different jurisdiction, and in those circumstances withholding tax sometimes applies to royalties, rent or even the sale of real estate. Governments use tax withholding as a means to combat tax evasion, and sometimes impose additional tax withholding requirements if the recipient has been delinquent in filing tax returns, or in industries where tax evasion is perceived to be common.

Tax preparation is the process of preparing tax returns, often income tax returns, often for a person other than the taxpayer, and generally for compensation. Tax preparation may be done by the taxpayer with or without the help of tax preparation software and online services. Tax preparation may also be done by a licensed professional such as an attorney, certified public accountant or enrolled agent, or by an unlicensed tax preparation business. Because United States income tax laws are considered to be complicated, many taxpayers seek outside assistance with taxes.

NETFILE is a transmission service that allows eligible Canadians to submit their personal income tax return to the Canada Revenue Agency using the Internet. Tax returns filed via NETFILE must first be prepared using a NETFILE-certified product. The software or Web application produces a .tax file, which must then be uploaded to the CRA independently to constitute a tax filing. NETFILE was introduced in 2001.

The United States Internal Revenue Service (IRS) uses forms for taxpayers and tax-exempt organizations to report financial information, such as to report income, calculate taxes to be paid to the federal government, and disclose other information as required by the Internal Revenue Code (IRC). There are over 800 various forms and schedules. Other tax forms in the United States are filed with state and local governments.

E-file is a system for submitting tax documents to the US Internal Revenue Service through the Internet or direct connection, usually without the need to submit any paper documents. Tax preparation software with e-filing capabilities includes stand-alone programs or websites. Tax professionals use tax preparation software from major software vendors for commercial use.

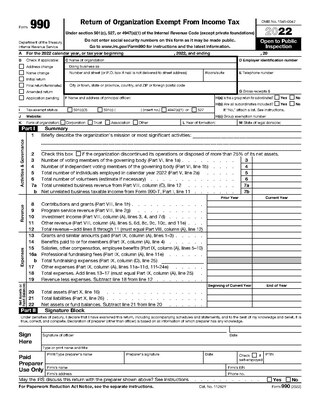

Form 990 is a United States Internal Revenue Service (IRS) form that provides the public with information about a nonprofit organization. It is also used by government agencies to prevent organizations from abusing their tax-exempt status. Some nonprofits, such as hospitals and other healthcare organizations, have more comprehensive reporting requirements.

Electronic tax filing, or e-filing, is a system for submitting tax documents to a revenue service electronically, often without the need to submit any paper documents.

The Preparer Tax Identification Number (PTIN) is an identification number that all paid tax return preparers must use on U.S. federal tax returns or claims for refund submitted to the Internal Revenue Service (IRS). Anyone who, for compensation, prepares all or substantially all of any federal tax return or claim for refund must obtain a PTIN issued by the IRS.

The IRS Free File Program is a service that allows U.S. taxpayers to prepare and e-file their federal income tax returns for free. Through the program, commercial tax software companies that are part of the Free File Alliance offer free tax preparation software to tax filers with annual adjusted gross income (AGI) below $73,000 for Tax Year 2022. The AGI is adjusted and typically increases slightly for each tax-filing season. The service is available through the IRS's website at www.irs.gov/freefile. Free fillable forms also are available to all taxpayers as part of the Free File Program.

CalFile is the current tax preparation program/service of the California Franchise Tax Board (FTB).