The Federal Reserve System is the central banking system of the United States. It was created on December 23, 1913, with the enactment of the Federal Reserve Act, after a series of financial panics led to the desire for central control of the monetary system in order to alleviate financial crises. Over the years, events such as the Great Depression in the 1930s and the Great Recession during the 2000s have led to the expansion of the roles and responsibilities of the Federal Reserve System.

The Federal Deposit Insurance Corporation (FDIC) is a United States government corporation supplying deposit insurance to depositors in American commercial banks and savings banks. The FDIC was created by the Banking Act of 1933, enacted during the Great Depression to restore trust in the American banking system. More than one-third of banks failed in the years before the FDIC's creation, and bank runs were common. The insurance limit was initially US$2,500 per ownership category, and this has been increased several times over the years. Since the enactment of the Dodd–Frank Wall Street Reform and Consumer Protection Act in 2010, the FDIC insures deposits in member banks up to $250,000 per ownership category. FDIC insurance is backed by the full faith and credit of the government of the United States, and according to the FDIC, "since its start in 1933 no depositor has ever lost a penny of FDIC-insured funds".

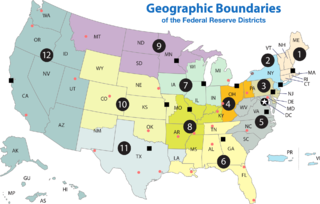

A Federal Reserve Bank is a regional bank of the Federal Reserve System, the central banking system of the United States. There are twelve in total, one for each of the twelve Federal Reserve Districts that were created by the Federal Reserve Act of 1913. The banks are jointly responsible for implementing the monetary policy set forth by the Federal Open Market Committee, and are divided as follows:

In the United States, the ACH Network is the national automated clearing house (ACH) for electronic funds transfers established in the 1960s and 1970s. It processes financial transactions for consumers, businesses, and federal, state, and local governments. ACH processes large volumes of credit and debit transactions in batches. ACH credit transfers include direct deposit for payroll, Social Security and other benefit payments, tax refunds, and vendor payments. ACH direct debit transfers include consumer payments on insurance premiums, mortgage loans, and other kinds of bills.

Fractional-reserve banking is the system of banking operating in almost all countries worldwide, under which banks that take deposits from the public are required to hold a proportion of their deposit liabilities in liquid assets as a reserve, and are at liberty to lend the remainder to borrowers. Bank reserves are held as cash in the bank or as balances in the bank's account at the central bank. The country's central bank determines the minimum amount that banks must hold in liquid assets, called the "reserve requirement" or "reserve ratio". Most commercial banks hold more than this minimum amount as excess reserves.

Reserve requirements are central bank regulations that set the minimum amount that a commercial bank must hold in liquid assets. This minimum amount, commonly referred to as the commercial bank's reserve, is generally determined by the central bank on the basis of a specified proportion of deposit liabilities of the bank. This rate is commonly referred to as the reserve ratio. Though the definitions vary, the commercial bank's reserves normally consist of cash held by the bank and stored physically in the bank vault, plus the amount of the bank's balance in that bank's account with the central bank. A bank is at liberty to hold in reserve sums above this minimum requirement, commonly referred to as excess reserves.

In the United States, federal funds are overnight borrowings between banks and other entities to maintain their bank reserves at the Federal Reserve. Banks keep reserves at Federal Reserve Banks to meet their reserve requirements and to clear financial transactions. Transactions in the federal funds market enable depository institutions with reserve balances in excess of reserve requirements to lend reserves to institutions with reserve deficiencies. These loans are usually made for one day only, that is, "overnight". The interest rate at which these deals are done is called the federal funds rate. Federal funds are not collateralized; like eurodollars, they are an unsecured interbank loan.

A capital requirement is the amount of capital a bank or other financial institution has to have as required by its financial regulator. This is usually expressed as a capital adequacy ratio of equity as a percentage of risk-weighted assets. These requirements are put into place to ensure that these institutions do not take on excess leverage and risk becoming insolvent. Capital requirements govern the ratio of equity to debt, recorded on the liabilities and equity side of a firm's balance sheet. They should not be confused with reserve requirements, which govern the assets side of a bank's balance sheet—in particular, the proportion of its assets it must hold in cash or highly-liquid assets. Capital is a source of funds not a use of funds.

In banking and finance, clearing denotes all activities from the time a commitment is made for a transaction until it is settled. This process turns the promise of payment into the actual movement of money from one account to another. Clearing houses were formed to facilitate such transactions among banks.

Excess reserves are bank reserves held by a bank in excess of a reserve requirement for it set by a central bank.

A money market account (MMA) or money market deposit account (MMDA) is a deposit account that pays interest based on current interest rates in the money markets. The interest rates paid are generally higher than those of savings accounts and transaction accounts; however, some banks will require higher minimum balances in money market accounts to avoid monthly fees and to earn interest.

The Expedited Funds Availability Act was enacted in 1987 by the United States Congress for the purpose of standardizing hold periods on deposits made to commercial banks and to regulate institutions' use of deposit holds. It is also referred to as Regulation CC or Reg CC, after the Federal Reserve regulation that implements the act. The law is codified in Title 12, Chapter 41 of the US Code and Title 12, Part 229 of the Code of Federal Regulations.

A substitute check is a negotiable instrument that is a digital reproduction of an original paper check. As a negotiable payment instrument in the United States, a substitute check maintains the status of a "legal check" in lieu of the original paper check, as authorized by the Check Clearing for the 21st Century Act. Instead of presenting the original paper checks, financial institutions and payment-processing centers transmit data from substitute checks electronically through the settlement process, through the United States Federal Reserve System, or by clearing the deposits on the basis of private agreements between member financial institutions. Financial institutions that process substitute checks in accordance with such private agreements are typically members of a clearinghouse that operates under the Uniform Commercial Code (UCC).

A central clearing counterparty (CCP), also referred to as a central counterparty, is a financial institution that takes on counterparty credit risk between parties to a transaction and provides clearing and settlement services for trades in foreign exchange, securities, options, and derivative contracts. CCPs are highly regulated institutions that specialize in managing counterparty credit risk.

The Central Bank of Kosovo is the central bank of Kosovo. It was founded in June 2008, the same year Kosovo declared its independence from Serbia, with the approval of Law No. 03/L-074 on the Central Bank of the Republic of Kosovo by the Kosovo Assembly. Before being established as the Central Bank of Kosovo, it operated as the Central Banking Authority of Kosovo. The official currency in Kosovo is the euro, which has been adopted unilaterally in 2002; however, Kosovo is not a member of the Eurozone. The headquarters of the CBK are located in the capital of Kosovo, Pristina.

Bank regulation in the United States is highly fragmented compared with other G10 countries, where most countries have only one bank regulator. In the U.S., banking is regulated at both the federal and state level. Depending on the type of charter a banking organization has and on its organizational structure, it may be subject to numerous federal and state banking regulations. Apart from the bank regulatory agencies the U.S. maintains separate securities, commodities, and insurance regulatory agencies at the federal and state level, unlike Japan and the United Kingdom. Bank examiners are generally employed to supervise banks and to ensure compliance with regulations.

Reserve Requirements for Depository Institutions is a Federal Reserve regulation governing the reserves that banks and credit unions keep to satisfy depositor withdrawals. Although the regulation still requires banks to report the aggregate balances of their deposit accounts to the Federal Reserve, most of its provisions are inactive as a result of policy changes during the COVID-19 pandemic.

The Clearing House Payments Company L.L.C. (PayCo) is a U.S.-based limited liability company formed by Clearing House Association. PayCo is a private sector, payment system infrastructure that operates an electronic check clearing and settlement system (SVPCO), a clearing house, and a wholesale funds transfer system (CHIPS).

Systemically important financial market utilities (SIFMUs) are entities whose failure or disruption could threaten the stability of the United States financial system. To date eight entities in the U.S. have been officially designated SIFMUs.

A clearing house is a financial institution formed to facilitate the exchange of payments, securities, or derivatives transactions. The clearing house stands between two clearing firms. Its purpose is to reduce the risk of a member firm failing to honor its trade settlement obligations.