A commodity market is a market that trades in the primary economic sector rather than manufactured products, such as cocoa, fruit and sugar. Hard commodities are mined, such as gold and oil. Futures contracts are the oldest way of investing in commodities. Commodity markets can include physical trading and derivatives trading using spot prices, forwards, futures, and options on futures. Farmers have used a simple form of derivative trading in the commodity market for centuries for price risk management.

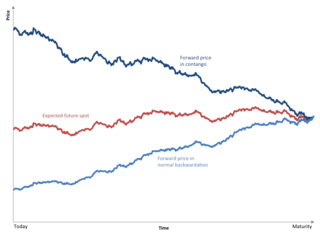

Contango is a situation where the futures price of a commodity is higher than the expected spot price of the contract at maturity. In a contango situation, arbitrageurs or speculators are "willing to pay more [now] for a commodity [to be received] at some point in the future than the actual expected price of the commodity [at that future point]. This may be due to people's desire to pay a premium to have the commodity in the future rather than paying the costs of storage and carry costs of buying the commodity today." On the other side of the trade, hedgers are happy to sell futures contracts and accept the higher-than-expected returns. A contango market is also known as a normal market, or carrying-cost market.

In finance, speculation is the purchase of an asset with the hope that it will become more valuable shortly. It can also refer to short sales in which the speculator hopes for a decline in value.

In finance, a futures contract is a standardized legal contract to buy or sell something at a predetermined price for delivery at a specified time in the future, between parties not yet known to each other. The asset transacted is usually a commodity or financial instrument. The predetermined price of the contract is known as the forward price or delivery price. The specified time in the future when delivery and payment occur is known as the delivery date. Because it derives its value from the value of the underlying asset, a futures contract is a derivative.

A hedge is an investment position intended to offset potential losses or gains that may be incurred by a companion investment. A hedge can be constructed from many types of financial instruments, including stocks, exchange-traded funds, insurance, forward contracts, swaps, options, gambles, many types of over-the-counter and derivative products, and futures contracts.

The New York Mercantile Exchange (NYMEX) is a commodity futures exchange owned and operated by CME Group of Chicago. NYMEX is located at One North End Avenue in Brookfield Place in the Battery Park City section of Manhattan, New York City.

A commodity price index is a fixed-weight index or (weighted) average of selected commodity prices, which may be based on spot or futures prices. It is designed to be representative of the broad commodity asset class or a specific subset of commodities, such as energy or metals. It is an index that tracks a basket of commodities to measure their performance. These indexes are often traded on exchanges, allowing investors to gain easier access to commodities without having to enter the futures market. The value of these indexes fluctuates based on their underlying commodities, and this value can be traded on an exchange in much the same way as stock index futures.

West Texas Intermediate (WTI) is a grade or mix of crude oil; the term is also used to refer to the spot price, the futures price, or assessed price for that oil. In colloquial usage, WTI usually refers to the WTI Crude Oil futures contract traded on the New York Mercantile Exchange (NYMEX). The WTI oil grade is also known as Texas light sweet. Oil produced from any location can be considered WTI if the oil meets the required qualifications. Spot and futures prices of WTI are used as a benchmark in oil pricing. This grade is described as light crude oil because of its low density and sweet because of its low sulfur content.

An energy derivative is a derivative contract based on an underlying energy asset, such as natural gas, crude oil, or electricity. Energy derivatives are exotic derivatives and include exchange-traded contracts such as futures and options, and over-the-counter derivatives such as forwards, swaps and options. Major players in the energy derivative markets include major trading houses, oil companies, utilities, and financial institutions.

The S&P GSCI serves as a benchmark for investment in the commodity markets and as a measure of commodity performance over time. It is a tradable index that is readily available to market participants of the Chicago Mercantile Exchange. The index was originally developed in 1991, by Goldman Sachs. In 2007, ownership transferred to Standard & Poor's, who currently own and publish it. Futures of the S&P GSCI use a multiple of 250. The index contains a much higher exposure to energy than other commodity price indices such as the Bloomberg Commodity Index.

The FTSE/CoreCommodity CRB Index is a commodity futures price index. It was first calculated by Commodity Research Bureau, Inc. in 1957 and made its inaugural appearance in the 1958 CRB Commodity Year Book.

A benchmark crude or marker crude is a crude oil that serves as a reference price for buyers and sellers of crude oil. There are three primary benchmarks, West Texas Intermediate (WTI), Brent Blend, and Dubai Crude. Other well-known blends include the OPEC Reference Basket used by OPEC, Tapis Crude which is traded in Singapore, Western Canadian Select used in Canada, Bonny Light used in Nigeria, Urals oil used in Russia and Mexico's Isthmus. Energy Intelligence Group publishes a handbook which identified 195 major crude streams or blends in its 2011 edition.

Soft commodities, or softs, are commodities such as coffee, cocoa, sugar, corn, wheat, soybean, fruit and livestock. The term generally refers to commodities that are grown, rather than mined; the latter are known as hard commodities.

An exchange-traded note (ETN) is a senior, unsecured, unsubordinated debt security issued by an underwriting bank. Similar to other debt securities, ETNs have a maturity date and are backed only by the credit of the issuer.

World food prices increased dramatically in 2007 and the first and second quarter of 2008, creating a global crisis and causing political and economic instability and social unrest in both poor and developed nations. Although the media spotlight focused on the riots that ensued in the face of high prices, the ongoing crisis of food insecurity had been years in the making. Systemic causes for the worldwide increases in food prices continue to be the subject of debate. After peaking in the second quarter of 2008, prices fell dramatically during the late-2000s recession but increased during late 2009 and 2010, reaching new heights in 2011 and 2012 at a level slightly higher than the level reached in 2008. Over the next years, prices fell, reaching a low in March 2016 with the deflated Food and Agriculture Organization (FAO) food price index close to pre-crisis level of 2006.

The Deutsche Bank Liquid Commodity Index (DBLCI) was launched in February 2003. It tracks the performance of six commodities in the energy, precious metals, industrial metals and grain sectors. The DBLCI has constant weightings for each of the six commodities and the index is rebalanced annually in the first week of November. Consequently, the weights fluctuate during the year according to the price movement of the underlying commodity futures.

In May 2006, Deutsche Bank launched a new set of commodity index products called the Deutsche Bank Liquid Commodities Indices Optimum Yield, or DBLCI-OY'. The DBLCI-OY indices are available for 24 commodities drawn from the energy, precious metals, industrial metals, agricultural and livestock sectors. A DBLCI-OY index based on the DBLCI benchmark weights is also available and the optimum yield technology has also been applied to the energy, precious metals, industrial metals and agricultural sector indices. Like the DBLCI, the DBLCI-OY is available in USD, EUR, GBP and JPY on a hedged and un-hedge basis. The DBLCI-OY is rebalanced on the fifth index business day of November when each commodity is adjusted to its base weight. The DBLCI-OY is also listed as an exchange-traded fund (ETF) on the American Stock Exchange.

The 2000s commodities boom or the commodities super cycle was the rise of many physical commodity prices during the early 21st century (2000–2014), following the Great Commodities Depression of the 1980s and 1990s. The boom was largely due to the rising demand from emerging markets such as the BRIC countries, particularly China during the period from 1992 to 2013, as well as the result of concerns over long-term supply availability. There was a sharp down-turn in prices during 2008 and early 2009 as a result of the credit crunch and European debt crisis, but prices began to rise as demand recovered from late 2009 to mid-2010.

The Theory of Storage describes features observed in commodity markets:

Food speculation refers to the buying and selling of futures contracts by traders with the aim of profiting from changes in food prices. Food speculation can be both positive and negative for food producers and buyers. It is betting on food prices (unregulated) financial markets. Food speculation by global players like banks, hedge funds or pension funds is alleged to cause price swings in staple foods such as wheat, maize and soy – even though too large price swings in an idealized economy are theoretically ruled out: Adam Smith in 1776 reasoned that the only way to make money from commodities trading is by buying low and selling high, which has the effect of smoothing out price swings and mitigating shortages. For the actors, the apparently random swings are predictable, which means potential huge profits. For the global poor, food speculation and resulting price peaks may result in increased poverty or even famine.