Related Research Articles

Insurance is a means of protection from financial loss in which, in exchange for a fee, a party agrees to compensate another party in the event of a certain loss, damage, or injury. It is a form of risk management, primarily used to protect against the risk of a contingent or uncertain loss.

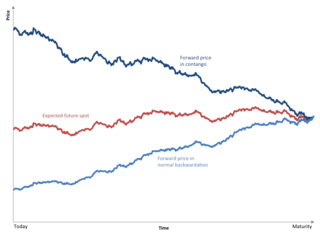

Contango is a situation in which the futures price of a commodity is higher than the expected spot price of the contract at maturity. In a contango situation, arbitrageurs or speculators are "willing to pay more [now] for a commodity [to be received] at some point in the future than the actual expected price of the commodity [at that future point]. This may be due to people's desire to pay a premium to have the commodity in the future rather than paying the costs of storage and carry costs of buying the commodity today." On the other side of the trade, hedgers are happy to sell futures contracts and accept the higher-than-expected returns. A contango market is also known as a normal market or carrying-cost market.

In finance, a bond is a type of security under which the issuer (debtor) owes the holder (creditor) a debt, and is obliged – depending on the terms – to provide cash flow to the creditor. The timing and the amount of cash flow provided varies, depending on the economic value that is emphasized upon, thus giving rise to different types of bonds. The interest is usually payable at fixed intervals: semiannual, annual, and less often at other periods. Thus, a bond is a form of loan or IOU. Bonds provide the borrower with external funds to finance long-term investments or, in the case of government bonds, to finance current expenditure.

Life insurance is a contract between an insurance policy holder and an insurer or assurer, where the insurer promises to pay a designated beneficiary a sum of money upon the death of an insured person. Depending on the contract, other events such as terminal illness or critical illness can also trigger payment. The policyholder typically pays a premium, either regularly or as one lump sum. The benefits may include other expenses, such as funeral expenses.

Fixed income refers to any type of investment under which the borrower or issuer is obliged to make payments of a fixed amount on a fixed schedule. For example, the borrower may have to pay interest at a fixed rate once a year and repay the principal amount on maturity. Fixed-income securities can be contrasted with equity securities that create no obligation to pay dividends or any other form of income. Bonds carry a level of legal protections for investors that equity securities do not: in the event of a bankruptcy, bond holders would be repaid after liquidation of assets, whereas shareholders with stock often receive nothing.

Title insurance is a form of indemnity insurance predominantly found in the United States and Canada which insures against financial loss from defects in title to real property and from the invalidity or unenforceability of mortgage loans. Unlike some land registration systems in countries outside the United States, US states' recorders of deeds generally do not guarantee indefeasible title to those recorded titles. Title insurance will defend against a lawsuit attacking the title or reimburse the insured for the actual monetary loss incurred up to the dollar amount of insurance provided by the policy.

Variable universal life insurance is a type of life insurance that builds a cash value. In a VUL, the cash value can be invested in a wide variety of separate accounts, similar to mutual funds, and the choice of which of the available separate accounts to use is entirely up to the contract owner. The 'variable' component in the name refers to this ability to invest in separate accounts whose values vary—they vary because they are invested in stock and/or bond markets. The 'universal' component in the name refers to the flexibility the owner has in making premium payments. The premiums can vary from nothing in a given month up to maximums defined by the Internal Revenue Code for life insurance. This flexibility is in contrast to whole life insurance that has fixed premium payments that typically cannot be missed without lapsing the policy.

Term life insurance or term assurance is life insurance that provides coverage at a fixed rate of payments for a limited period of time, the relevant term. After that period expires, coverage at the previous rate of premiums is no longer guaranteed and the client must either forgo coverage or potentially obtain further coverage with different payments or conditions. If the life insured dies during the term, the death benefit will be paid to the beneficiary. Term insurance is typically the least expensive way to purchase a substantial death benefit on a coverage amount per premium dollar basis over a specific period of time.

An endowment mortgage is a mortgage loan arranged on an interest-only basis where the capital is intended to be repaid by one or more endowment policies. The phrase "endowment mortgage" is used mainly in the United Kingdom by lenders and consumers to refer to this arrangement and is not a legal term.

Underwriting (UW) services are provided by some large financial institutions, such as banks, insurance companies and investment houses, whereby they guarantee payment in case of damage or financial loss and accept the financial risk for liability arising from such guarantee. An underwriting arrangement may be created in a number of situations including insurance, issues of security in a public offering, and bank lending, among others. The person or institution that agrees to sell a minimum number of securities of the company for commission is called the underwriter.

Universal life insurance is a type of cash value life insurance, sold primarily in the United States. Under the terms of the policy, the excess of premium payments above the current cost of insurance is credited to the cash value of the policy, which is credited each month with interest. The policy is debited each month by a cost of insurance (COI) charge as well as any other policy charges and fees drawn from the cash value, even if no premium payment is made that month. Interest credited to the account is determined by the insurer but has a contractual minimum rate. When an earnings rate is pegged to a financial index such as a stock, bond or other interest rate index, the policy is an "Indexed universal life" contract. Such policies offer the advantage of guaranteed level premiums throughout the insured's lifetime at a substantially lower premium cost than an equivalent whole life policy at first. The cost of insurance always increases, as is found on the cost index table. That not only allows for easy comparison of costs between carriers but also works well in irrevocable life insurance trusts (ILITs) since cash is of no consequence.

Whole life insurance, or whole of life assurance, sometimes called "straight life" or "ordinary life", is a life insurance policy which is guaranteed to remain in force for the insured's entire lifetime, provided required premiums are paid, or to the maturity date. As a life insurance policy it represents a contract between the insured and insurer that as long as the contract terms are met, the insurer will pay the death benefit of the policy to the policy's beneficiaries when the insured dies.

An endowment policy is a life insurance contract designed to pay a lump sum after a specific term or on death. Typical maturities are ten, fifteen or twenty years up to a certain age limit. Some policies also pay out in the case of critical illness.

Critical illness insurance, otherwise known as critical illness cover or a dread disease policy, is an insurance product in which the insurer is contracted to typically make a lump sum cash payment if the policyholder is diagnosed with one of the specific illnesses on a predetermined list as part of an insurance policy.

Mortgage life insurance is a form of insurance specifically designed to protect a repayment mortgage. If the policyholder were to die while the mortgage life insurance was in force, the policy would pay out a capital sum that will be just sufficient to repay the outstanding mortgage.

A mortgage loan or simply mortgage, in civil law jurisdictions known also as a hypothec loan, is a loan used either by purchasers of real property to raise funds to buy real estate, or by existing property owners to raise funds for any purpose while putting a lien on the property being mortgaged. The loan is "secured" on the borrower's property through a process known as mortgage origination. This means that a legal mechanism is put into place which allows the lender to take possession and sell the secured property to pay off the loan in the event the borrower defaults on the loan or otherwise fails to abide by its terms. The word mortgage is derived from a Law French term used in Britain in the Middle Ages meaning "death pledge" and refers to the pledge ending (dying) when either the obligation is fulfilled or the property is taken through foreclosure. A mortgage can also be described as "a borrower giving consideration in the form of a collateral for a benefit (loan)".

In finance, an option is a contract which conveys to its owner, the holder, the right, but not the obligation, to buy or sell a specific quantity of an underlying asset or instrument at a specified strike price on or before a specified date, depending on the style of the option. Options are typically acquired by purchase, as a form of compensation, or as part of a complex financial transaction. Thus, they are also a form of asset and have a valuation that may depend on a complex relationship between underlying asset price, time until expiration, market volatility, the risk-free rate of interest, and the strike price of the option. Options may be traded between private parties in over-the-counter (OTC) transactions, or they may be exchange-traded in live, public markets in the form of standardized contracts.

Bond insurance, also known as "financial guaranty insurance", is a type of insurance whereby an insurance company guarantees scheduled payments of interest and principal on a bond or other security in the event of a payment default by the issuer of the bond or security. It is a form of "credit enhancement" that generally results in the rating of the insured security being the higher of (i) the claims-paying rating of the insurer or (ii) the rating the bond would have without insurance.

Fixed annuities are insurance products which protect against loss and generally offer fixed rates of return. The rates are typically based on the current interest rate environment. They are offered by licensed and regulated insurance companies. State insurance/insolvency funds guarantees vary from state to state, and may not cover 100% of the Annuity Value. For example, in California the fund will cover "80% not to exceed $250,000."

A with-profits policy (Commonwealth) or participating policy (U.S.) is an insurance contract that participates in the profits of a life insurance company. The company is often a mutual life insurance company, or had been one when it began its with-profits product line. Similar arrangements are found in other countries such as those in continental Europe.

References

- ↑ "What Are Traded Life Policies And Traded Endowment Policies?". Purvis Capital. Retrieved June 14, 2024.

- ↑ "Why some Singaporeans are selling their endowment insurance policies" . Retrieved June 14, 2024.

- ↑ "What should I do with my endowment policy?". The Guardian. July 13, 2006.

- ↑ "How to squeeze extra £1,000 from an old endowment". The Telegraph. July 6, 2013.

- ↑ "Do not rush to sell your valuable endowment policy". The Irish Times. November 29, 1996.