Related Research Articles

A commodity market is a market that trades in the primary economic sector rather than manufactured products, such as cocoa, fruit and sugar. Hard commodities are mined, such as gold and oil. Futures contracts are the oldest way of investing in commodities. Commodity markets can include physical trading and derivatives trading using spot prices, forwards, futures, and options on futures. Farmers have used a simple form of derivative trading in the commodity market for centuries for price risk management.

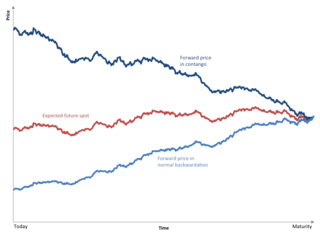

Normal backwardation, also sometimes called backwardation, is the market condition where the price of a commodity's forward or futures contract is trading below the expected spot price at contract maturity. The resulting futures or forward curve would typically be downward sloping, since contracts for further dates would typically trade at even lower prices. In practice, the expected future spot price is unknown, and the term "backwardation" may refer to "positive basis", which occurs when the current spot price exceeds the price of the future.

In finance, a futures contract is a standardized legal agreement to buy or sell something at a predetermined price at a specified time in the future, between parties not known to each other. The asset transacted is usually a commodity or financial instrument. The predetermined price the parties agree to buy and sell the asset for is known as the forward price. The specified time in the future—which is when delivery and payment occur—is known as the delivery date. Because it is a function of an underlying asset, a futures contract is a derivative product.

In finance, a forward contract or simply a forward is a non-standardized contract between two parties to buy or sell an asset at a specified future time at a price agreed on at the time of conclusion of the contract, making it a type of derivative instrument. The party agreeing to buy the underlying asset in the future assumes a long position, and the party agreeing to sell the asset in the future assumes a short position. The price agreed upon is called the delivery price, which is equal to the forward price at the time the contract is entered into.

A futures exchange or futures market is a central financial exchange where people can trade standardized futures contracts defined by the exchange. Futures contracts are derivatives contracts to buy or sell specific quantities of a commodity or financial instrument at a specified price with delivery set at a specified time in the future. Futures exchanges provide physical or electronic trading venues, details of standardized contracts, market and price data, clearing houses, exchange self-regulations, margin mechanisms, settlement procedures, delivery times, delivery procedures and other services to foster trading in futures contracts. Futures exchanges can be organized as non-profit member-owned organizations or as for-profit organizations. Futures exchanges can be integrated under the same brand name or organization with other types of exchanges, such as stock markets, options markets, and bond markets. Non-profit member-owned futures exchanges benefit their members, who earn commissions and revenue acting as brokers or market makers. For-profit futures exchanges earn most of their revenue from trading and clearing fees.

A hedge is an investment position intended to offset potential losses or gains that may be incurred by a companion investment. A hedge can be constructed from many types of financial instruments, including stocks, exchange-traded funds, insurance, forward contracts, swaps, options, gambles, many types of over-the-counter and derivative products, and futures contracts.

The foreign exchange market is a global decentralized or over-the-counter (OTC) market for the trading of currencies. This market determines foreign exchange rates for every currency. It includes all aspects of buying, selling and exchanging currencies at current or determined prices. In terms of trading volume, it is by far the largest market in the world, followed by the credit market.

Brent Crude may refer to any or all of the components of the Brent Complex, a physically and financially traded oil market based around the North Sea of Northwest Europe; colloquially, Brent Crude usually refers to the price of the ICE Brent Crude Oil futures contract or the contract itself. The original Brent Crude referred to a trading classification of sweet light crude oil first extracted from the Brent oil field in the North Sea in 1976. As production from the Brent oilfield declined over time, crude oil blends from other oil fields have been added to the trade classification. The current Brent blend consists of crude oil produced from the Brent, Forties, Oseberg, Ekofisk, and Troll oil fields.

In finance, a contract for difference (CFD) is a contract between two parties, typically described as "buyer" and "seller", stipulating that the buyer will pay to the seller the difference between the current value of an asset and its value at contract time.

In finance, margin is the collateral that a holder of a financial instrument has to deposit with a counterparty to cover some or all of the credit risk the holder poses for the counterparty. This risk can arise if the holder has done any of the following:

An energy derivative is a derivative contract based on an underlying energy asset, such as natural gas, crude oil, or electricity. Energy derivatives are exotic derivatives and include exchange-traded contracts such as futures and options, and over-the-counter derivatives such as forwards, swaps and options. Major players in the energy derivative markets include major trading houses, oil companies, utilities, and financial institutions.

The Dalian Commodity Exchange (DCE) is a Chinese futures exchange based in Dalian, Liaoning province, China. It is a non-profit, self-regulating and membership legal entity established on February 28, 1993.

Foreign exchange risk is a financial risk that exists when a financial transaction is denominated in a currency other than the domestic currency of the company. The exchange risk arises when there is a risk of an unfavourable change in exchange rate between the domestic currency and the denominated currency before the date when the transaction is completed.

The Intercontinental Exchange (ICE) is an American Fortune 500 company formed in 2000 that operates global exchanges, clearing houses and provides mortgage technology, data and listing services. The company owns exchanges for financial and commodity markets, and operates 12 regulated exchanges and marketplaces. This includes ICE futures exchanges in the United States, Canada and Europe, the Liffe futures exchanges in Europe, the New York Stock Exchange, equity options exchanges and OTC energy, credit and equity markets.

A property derivative is a financial derivative whose value is derived from the value of an underlying real estate asset. In practice, because individual real estate assets fall victim to market inefficiencies and are hard to accurately price, property derivative contracts are typically written based on a real estate property index. In turn, the real estate property index attempts to aggregate real estate market information to provide a more accurate representation of underlying real estate asset performance. Trading or taking positions in property derivatives is also known as synthetic real estate.

A foreign exchange derivative is a financial derivative whose payoff depends on the foreign exchange rates of two currencies. These instruments are commonly used for currency speculation and arbitrage or for hedging foreign exchange risk.

Iran Mercantile Exchange (IME) is a commodities exchange located in Tehran, Iran.

OneChicago was a US-based all-electronic futures exchange with headquarters in Chicago, Illinois. The exchange offered approximately 12,509 single-stock futures (SSF) products with names such as IBM, Apple and Google. All trading was cleared through Options Clearing Corporation (OCC). The OneChicago exchange closed in September 2020.

In finance, an exchange for ETF (EFETF) transaction is one in which ETF units are exchanged for futures contracts which have the same underlying index; this is usually any of the broad based equity indices in North America, Europe, and Asia for which there is a liquid future available. Typical indices are S&P, FTSE, DAX, CAC 40. It is similar to an exchange for physical (EFP) in which the constituent basket of stocks is exchanged for a futures contract. Usually traded via a broker who will cross the futures on exchange, this is a way for ETF market makers to manage their inventories in ETF positions which they have hedged with futures

An exchange of futures for swaps (EFS) is a transaction negotiated privately in which a futures contract for a physical item is exchanged for a cash settled swap contract. It is similar to an EFP except that it involves a cash contract rather than a physicals contract. An EFS gives the market participants a chance to liquidate a swap position in an environment that is normally not very liquid.

References

- ↑ "Exchange of Futures for Physical (EFP) Explained - Part One". Silver Axis: Today in Silver. Jul 30, 2009.

- ↑ "Exchange for Physicals (EFP)" (PDF). Risk Limited.

- ↑ "EFP, EFR and EOO Trades". CME Group.

| | This finance-related article is a stub. You can help Wikipedia by expanding it. |