Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced and sold in a specific time period by countries. Due to its complex and subjective nature this measure is often revised before being considered a reliable indicator. GDP (nominal) per capita does not, however, reflect differences in the cost of living and the inflation rates of the countries; therefore, using a basis of GDP per capita at purchasing power parity (PPP) may be more useful when comparing living standards between nations, while nominal GDP is more useful comparing national economies on the international market. Total GDP can also be broken down into the contribution of each industry or sector of the economy. The ratio of GDP to the total population of the region is the per capita GDP.

A variety of measures of national income and output are used in economics to estimate total economic activity in a country or region, including gross domestic product (GDP), gross national product (GNP), net national income (NNI), and adjusted national income. All are specially concerned with counting the total amount of goods and services produced within the economy and by various sectors. The boundary is usually defined by geography or citizenship, and it is also defined as the total income of the nation and also restrict the goods and services that are counted. For instance, some measures count only goods & services that are exchanged for money, excluding bartered goods, while other measures may attempt to include bartered goods by imputing monetary values to them.

The economy of Andorra is a developed and free market economy driven by finance, retail, and tourism. The country's gross domestic product (GDP) was US$3.66 billion in 2007. Attractive for shoppers from France and Spain as a free port, Andorra also has developed active summer and winter tourist resorts. With some 270 hotels and 400 restaurants, as well as many shops, the tourist trade employs a growing portion of the domestic labour force. An estimated 13 million tourists visit annually.

The world economy or global economy is the economy of all humans of the world, referring to the global economic system, which includes all economic activities which are conducted both within and between nations, including production, consumption, economic management, work in general, exchange of financial values and trade of goods and services. In some contexts, the two terms are distinct "international" or "global economy" being measured separately and distinguished from national economies, while the "world economy" is simply an aggregate of the separate countries' measurements. Beyond the minimum standard concerning value in production, use and exchange, the definitions, representations, models and valuations of the world economy vary widely. It is inseparable from the geography and ecology of planet Earth.

Dumping, in economics, is a kind of injuring pricing, especially in the context of international trade. It occurs when manufacturers export a product to another country at a price below the normal price with an injuring effect. The objective of dumping is to increase market share in a foreign market by driving out competition and thereby create a monopoly situation where the exporter will be able to unilaterally dictate price and quality of the product. Trade treaties might include mechanisms to alleviate problems related to dumping, such as countervailing duty penalties and anti-dumping statutes.

The terms of trade (TOT) is the relative price of exports in terms of imports and is defined as the ratio of export prices to import prices. It can be interpreted as the amount of import goods an economy can purchase per unit of export goods.

Real gross domestic product is a macroeconomic measure of the value of economic output adjusted for price changes. This adjustment transforms the money-value measure, nominal GDP, into an index for quantity of total output. Although GDP is total output, it is primarily useful because it closely approximates the total spending: the sum of consumer spending, investment made by industry, excess of exports over imports, and government spending. Due to inflation, GDP increases and does not actually reflect the true growth in an economy. That is why the GDP must be divided by the inflation rate to get the growth of the real GDP. Different organizations use different types of 'Real GDP' measures, for example, the UNCTAD uses 2005 Constant prices and exchange rates while the FRED uses 2009 constant prices and exchange rates, and recently the World Bank switched from 2005 to 2010 constant prices and exchange rates.

Non-tariff barriers to trade are trade barriers that restrict imports or exports of goods or services through mechanisms other than the simple imposition of tariffs.

Output in economics is the "quantity of goods or services produced in a given time period, by a firm, industry, or country", whether consumed or used for further production. The concept of national output is essential in the field of macroeconomics. It is national output that makes a country rich, not large amounts of money.

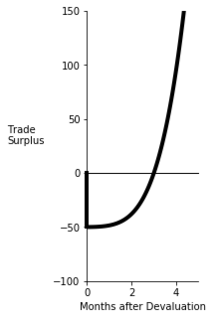

The Marshall–Lerner condition is satisfied if the absolute sum of a country's export and import demand elasticities is greater than one. If it is satisfied, then if a country begins with a zero trade deficit then when the country's currency depreciates, its balance of trade will improve. The country's imports become more expensive and exports become cheaper due to the change in relative prices, and the Marshall-Lerner condition implies that the indirect effect on the quantity of trade will exceed the direct effect of the country having to pay a higher price for its imports and receive a lower price for its exports.

In economics, competition is a scenario where different economic firms are in contention to obtain goods that are limited by varying the elements of the marketing mix: price, product, promotion and place. In classical economic thought, competition causes commercial firms to develop new products, services and technologies, which would give consumers greater selection and better products. The greater the selection of a good is in the market, prices are typically lower for the products, compared to what the price would be if there was no competition (monopoly) or little competition (oligopoly).

An import is the receiving country in an export from the sending country. Importation and exportation are the defining financial transactions of international trade.

The international dollar, also known as Geary–Khamis dollar, is a hypothetical unit of currency that has the same purchasing power parity that the U.S. dollar had in the United States at a given point in time. It is mainly used in economics and financial statistics for various purposes, most notably to determine and compare the purchasing power parity and gross domestic product of various countries and markets. The year 1990 or 2000 is often used as a benchmark year for comparisons that run through time. The unit is often abbreviated, e.g. 2000 US dollars or 2000 International$.

Material flow accounting (MFA) is the study of material flows on a national or regional scale. It is therefore sometimes also referred to as regional, national or economy-wide material flow analysis.

Official statistics are statistics published by government agencies or other public bodies such as international organizations as a public good. They provide quantitative or qualitative information on all major areas of citizens' lives, such as economic and social development, living conditions, health, education, and the environment.

In statistics, a deflator is a value that allows data to be measured over time in terms of some base period, usually through a price index, in order to distinguish between changes in the money value of a gross national product (GNP) that come from a change in prices, and changes from a change in physical output. It is the measure of the price level for some quantity. A deflator serves as a price index in which the effects of inflation are nulled. It is the difference between real and nominal GDP.

In economics, a tariff-rate quota (TRQ) is a two-tiered tariff system that combines import quotas and tariffs to regulate import products.

Seafood in Australia comes from local and international commercial fisheries, aquaculture and recreational anglers. It is an economically important sector, and along with agriculture and forestry contributed $24,744 million to Australia's GDP in year 2007–2008, out of a total GDP of $1,084,146 million. Commercial fisheries in Commonwealth waters are managed by the Australian Fisheries Management Authority, while commercial and recreational fishing in state waters is managed by various state-level agencies.

Import parity price or IPP is defined as, “The price that a purchaser pays or can expect to pay for imported goods; thus the c.i.f. import price plus tariff plus transport cost to the purchaser's location. This and the export parity price together define a range of the possible equilibrium prices for equivalent domestically produced goods”.

This glossary of economics is a list of definitions of terms and concepts used in economics, its sub-disciplines, and related fields.