In law, a trust is a relationship in which the holder of property gives it to another person or entity who must keep and use it solely for the benefit of another person or group of persons. In the English common law tradition, the party who entrusts the property is known as the "settlor", the party to whom the property is entrusted is known as the "trustee", the party for whose benefit the property is entrusted is known as the "beneficiary", and the entrusted property itself is known as the "corpus" or "trust property". A testamentary trust is created by a will and arises after the death of the settlor. An inter vivos trust is created during the settlor's lifetime by a trust instrument. A trust may be revocable or irrevocable; an irrevocable trust can be "broken" (revoked) by a judicial proceeding or by consent of the settlor and the beneficiaries.

In finance, a bond is a type of security under which the issuer (debtor) owes the holder (creditor) a debt, and is obliged – depending on the terms – to provide cash flow to the creditor. The timing and the amount of cash flow provided varies, depending on the economic value that is emphasized upon, thus giving rise to different types of bonds. The interest is usually payable at fixed intervals: semiannual, annual, and less often at other periods. Thus, a bond is a form of loan or IOU. Bonds provide the borrower with external funds to finance long-term investments or, in the case of government bonds, to finance current expenditure.

In accountancy, depreciation is a term that refers to two aspects of the same concept: first, an actual reduction in the fair value of an asset, such as the decrease in value of factory equipment each year as it is used and wears, and second, the allocation in accounting statements of the original cost of the assets to periods in which the assets are used.

Financial accounting is a branch of accounting concerned with the summary, analysis and reporting of financial transactions related to a business. This involves the preparation of financial statements available for public use. Stockholders, suppliers, banks, employees, government agencies, business owners, and other stakeholders are examples of people interested in receiving such information for decision making purposes.

Liquidation is the process in accounting by which a company is brought to an end. The assets and property of the business are redistributed. When a firm has been liquidated, it is sometimes referred to as wound-up or dissolved, although dissolution technically refers to the last stage of liquidation. The process of liquidation also arises when customs, an authority or agency in a country responsible for collecting and safeguarding customs duties, determines the final computation or ascertainment of the duties or drawback accruing on an entry.

A foundation is a type of nonprofit organization or charitable trust that usually provides funding and support to other charitable organizations through grants, while also potentially participating directly in charitable activities. Foundations encompass public charitable foundations, like community foundations, and private foundations, which are often endowed by an individual or family. Nevertheless, the term "foundation" might also be adopted by organizations not primarily engaged in public grantmaking.

In finance, a revaluation of fixed assets is an action that may be required to accurately describe the true value of the capital goods a business owns. This should be distinguished from planned depreciation, where the recorded decline in the value of an asset is tied to its age.

In bookkeeping, a general ledger is a bookkeeping ledger in which accounting data are posted from journals and aggregated from subledgers, such as accounts payable, accounts receivable, cash management, fixed assets, purchasing and projects. A general ledger may be maintained on paper, on a computer, or in the cloud. A ledger account is created for each account in the chart of accounts for an organization and is classified into account categories, such as income, expense, assets, liabilities, and equity; the collection of all these accounts is known as the general ledger. The general ledger holds financial and non-financial data for an organization. Each account in the general ledger consists of one or more pages. An organization's statement of financial position and the income statement are both derived from income and expense account categories in the general ledger.

A fixed asset, also known as long-lived assets or property, plant and equipment (PP&E), is a term used in accounting for assets and property that may not easily be converted into cash. Fixed assets are different from current assets, such as cash or bank accounts, because the latter are liquid assets. In most cases, only tangible assets are referred to as fixed.

Capital expenditure or capital expense is the money an organization or corporate entity spends to buy, maintain, or improve its fixed assets, such as buildings, vehicles, equipment, or land. It is considered a capital expenditure when the asset is newly purchased or when money is used towards extending the useful life of an existing asset, such as repairing the roof.

PIMCO is an American investment management firm focusing on active fixed income management worldwide. PIMCO manages investments in many asset classes such as fixed income, equities, commodities, asset allocation, ETFs, hedge funds, and private equity. PIMCO is one of the largest investment managers, actively managing more than $2 trillion in assets for central banks, sovereign wealth funds, pension funds, corporations, foundations and endowments, and individual investors around the world. According to the Sovereign Wealth Fund Institute, PIMCO is the 6th-largest Asset Manager in the world by managed AUM.

A unit trust is a form of collective investment constituted under a trust deed. A unit trust pools investors' money into a single fund, which is managed by a fund manager. Unit trusts offer access to a wide range of investments, and depending on the trust, it may invest in securities such as shares, bonds, gilts, and also properties, mortgage and cash equivalents. Those investing in the trust own "units", whose price is called the "net asset value" (NAV). The number of these units is not fixed and when more is invested in a unit trust, more units are created.

In finance, a floating charge is a security interest over a fund of changing assets of a company or other legal person. Unlike a fixed charge, which is created over ascertained and definite property, a floating charge is created over property of an ambulatory and shifting nature, such as receivables and stock.

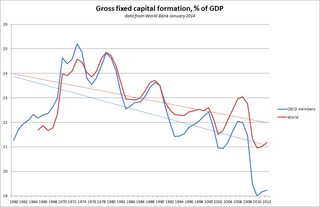

Capital formation is a concept used in macroeconomics, national accounts and financial economics. Occasionally it is also used in corporate accounts. It can be defined in three ways:

Fixed assets management is an accounting process that seeks to track fixed assets for the purposes of financial accounting, preventive maintenance, and theft deterrence.

A line of credit is a credit facility extended by a bank or other financial institution to a government, business or individual customer that enables the customer to draw on the facility when the customer needs funds. A financial institution makes available an amount of credit to a business or consumer during a specified period of time.

London Stock Exchange Group plc (LSEG) is a United Kingdom-based stock exchange and financial information company headquartered in the City of London, England. It owns the London Stock Exchange, Refinitiv, LSEG Technology, FTSE Russell, and majority stakes in LCH and Tradeweb.

In financial accounting, an asset is any resource owned or controlled by a business or an economic entity. It is anything that can be used to produce positive economic value. Assets represent value of ownership that can be converted into cash . The balance sheet of a firm records the monetary value of the assets owned by that firm. It covers money and other valuables belonging to an individual or to a business.

Agnew v Commissioners of Inland Revenue, more commonly referred to as Re Brumark Investments Ltd[2001] UKPC 28 is a decision of the Privy Council relating to New Zealand and UK insolvency law, concerning the taking of a security interest over a company's assets, the proper characterisation of a floating charge, and the priority of creditors in a company winding-up.

Insight Investment (Insight) is one of the largest global asset management companies, responsible for £683.0 billion of assets under management as of 30 September 2022, represented by the value of cash securities and other economic exposure managed for clients. It manages strategies which include fixed income, liability-driven investment (LDI), cash, absolute return, multi-asset, and equities. Insight is a subsidiary of The Bank of New York Mellon, a multinational financial services corporation.