Fundamental analysis, in accounting and finance, is the analysis of a business's financial statements ; health; competitors and markets. It also considers the overall state of the economy and factors including interest rates, production, earnings, employment, GDP, housing, manufacturing and management. There are two basic approaches that can be used: bottom up analysis and top down analysis. These terms are used to distinguish such analysis from other types of investment analysis, such as quantitative and technical.

International Financial Reporting Standards, commonly called IFRS, are accounting standards issued by the IFRS Foundation and the International Accounting Standards Board (IASB). They constitute a standardised way of describing the company's financial performance and position so that company financial statements are understandable and comparable across international boundaries. They are particularly relevant for companies with shares or securities publicly listed.

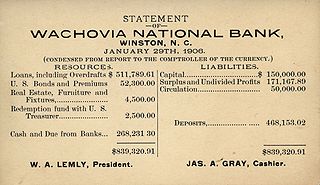

Financial statements are formal records of the financial activities and position of a business, person, or other entity.

The Financial Accounting Standards Board (FASB) is a private standard-setting body whose primary purpose is to establish and improve Generally Accepted Accounting Principles (GAAP) within the United States in the public's interest. The Securities and Exchange Commission (SEC) designated the FASB as the organization responsible for setting accounting standards for public companies in the U.S. The FASB replaced the American Institute of Certified Public Accountants' (AICPA) Accounting Principles Board (APB) on July 1, 1973. The FASB is run by the nonprofit Financial Accounting Foundation.

The Securities Act of 1933, also known as the 1933 Act, the Securities Act, the Truth in Securities Act, the Federal Securities Act, and the '33 Act, was enacted by the United States Congress on May 27, 1933, during the Great Depression and after the stock market crash of 1929. It is an integral part of United States securities regulation. It is legislated pursuant to the Interstate Commerce Clause of the Constitution.

A financial audit is conducted to provide an opinion whether "financial statements" are stated in accordance with specified criteria. Normally, the criteria are international accounting standards, although auditors may conduct audits of financial statements prepared using the cash basis or some other basis of accounting appropriate for the organization. In providing an opinion whether financial statements are fairly stated in accordance with accounting standards, the auditor gathers evidence to determine whether the statements contain material errors or other misstatements.

A prediction or forecast is a statement about a future event or about future data. Predictions are often, but not always, based upon experience or knowledge of forecasters. There is no universal agreement about the exact difference between "prediction" and "estimation"; different authors and disciplines ascribe different connotations.

In financial accounting, a cash flow statement, also known as statement of cash flows, is a financial statement that shows how changes in balance sheet accounts and income affect cash and cash equivalents, and breaks the analysis down to operating, investing and financing activities. Essentially, the cash flow statement is concerned with the flow of cash in and out of the business. As an analytical tool, the statement of cash flows is useful in determining the short-term viability of a company, particularly its ability to pay bills. International Accounting Standard 7 is the International Accounting Standard that deals with cash flow statements.

Stock valuation is the method of calculating theoretical values of companies and their stocks. The main use of these methods is to predict future market prices, or more generally, potential market prices, and thus to profit from price movement – stocks that are judged undervalued are bought, while stocks that are judged overvalued are sold, in the expectation that undervalued stocks will overall rise in value, while overvalued stocks will generally decrease in value. A target price is a price at which an analyst believes a stock to be fairly valued relative to its projected and historical earnings.

A Form 10-K is an annual report required by the U.S. Securities and Exchange Commission (SEC), that gives a comprehensive summary of a company's financial performance. Although similarly named, the annual report on Form 10-K is distinct from the often glossy "annual report to shareholders", which a company must send to its shareholders when it holds an annual meeting to elect directors. The 10-K includes information such as company history, organizational structure, executive compensation, equity, subsidiaries, and audited financial statements, among other information.

An auditor's report is a formal opinion, or disclaimer thereof, issued by either an internal auditor or an independent external auditor as a result of an internal or external audit, as an assurance service in order for the user to make decisions based on the results of the audit.

Evinrude Outboard Motors was a North American company that built a major brand of two-stroke outboard motors for boats. Founded by Ole Evinrude in Milwaukee, Wisconsin in 1907, it was formerly owned by the publicly traded Outboard Marine Corporation (OMC) since 1935 but OMC filed for bankruptcy in 2000. It was working as a subsidiary of Canadian Multinational Bombardier Recreational Products but was discontinued in May of 2020.

A going concern is an accounting term for a business that is assumed will meet its financial obligations when they become due. It functions without the threat of liquidation for the foreseeable future, which is usually regarded as at least the next 12 months or the specified accounting period. The presumption of going concern for the business implies the basic declaration of intention to keep operating its activities at least for the next year, which is a basic assumption for preparing financial statements that comprehend the conceptual framework of the IFRS. Hence, a declaration of going concern means that the business has neither the intention nor the need to liquidate or to materially curtail the scale of its operations.

In finance, risk factors are the building blocks of investing, that help explain the systematic returns in equity market, and the possibility of losing money in investments or business adventures. A risk factor is a concept in finance theory such as the capital asset pricing model, arbitrage pricing theory and other theories that use pricing kernels. In these models, the rate of return of an asset is a random variable whose realization in any time period is a linear combination of other random variables plus a disturbance term or white noise. In practice, a linear combination of observed factors included in a linear asset pricing model proxy for a linear combination of unobserved risk factors if financial market efficiency is assumed. In the Intertemporal CAPM, non-market factors proxy for changes in the investment opportunity set.

Predictive analytics encompasses a variety of statistical techniques from data mining, predictive modeling, and machine learning that analyze current and historical facts to make predictions about future or otherwise unknown events.

An earnings call is a teleconference, or webcast, in which a public company discusses the financial results of a reporting period. The name comes from earnings per share (EPS), the bottom line number in the income statement divided by the number of shares outstanding. The US-based National Investor Relations Institute (NIRI) says that 92% of companies represented by their members conduct earnings calls and that virtually all of these are webcast. Transcripts of calls may be made available either by the company or a third party.

A pitch book, also called a Confidential Information Memorandum, is a marketing presentation used by investment banks, entrepreneurs, corporate finance firms, business brokers and other M&A intermediaries advising on the sale or disposal of the shares or assets of a business. It consists of a careful arrangement and analysis of the investment considerations of the client business and is presented to investors and potential investors with the intent of providing them the information necessary for them to make a decision to buy or invest in the client business. There are many contributors to an intermediary's pitch book. In an investment bank contributors may include anyone from an analyst to an associate, a vice-president or even the managing director. See Financial analyst § Investment Banking.

Regulation S-K is a prescribed regulation under the US Securities Act of 1933 that lays out reporting requirements for various SEC filings used by public companies. Companies are also often called issuers, filers or registrants.

The convergence of accounting standards refers to the goal of establishing a single set of accounting standards that will be used internationally. Convergence in some form has been taking place for several decades, and efforts today include projects that aim to reduce the differences between accounting standards.

Management accounting principles (MAP) were developed to serve the core needs of internal management to improve decision support objectives, internal business processes, resource application, customer value, and capacity utilization needed to achieve corporate goals in an optimal manner. Another term often used for management accounting principles for these purposes is managerial costing principles. The two management accounting principles are:

- Principle of Causality and,

- Principle of Analogy.