Related Research Articles

The economy of the Cayman Islands, a British overseas territory located in the western Caribbean Sea, is mainly fueled by the tourism sector and by the financial services sector, together representing 50–60 percent of the country's gross domestic product (GDP). The Cayman Islands Investment Bureau, a government agency, has been established with the mandate of promoting investment and economic development in the territory. Because of the territory’s economic success and it being a popular banking destination for wealthy individuals and businesses, it is often dubbed the ‘financial capital’ of the Caribbean.

The economy of Gibraltar consists largely of the services sector. While part of the European Union until Brexit, the British overseas territory of Gibraltar has a separate legal jurisdiction from the United Kingdom and a different tax system. The role of the UK Ministry of Defence, which at one time was Gibraltar's main source of income, has declined, with today's economy mainly based on shipping, tourism, financial services, and the Internet.

Corporate haven, corporate tax haven, or multinational tax haven is used to describe a jurisdiction that multinational corporations find attractive for establishing subsidiaries or incorporation of regional or main company headquarters, mostly due to favourable tax regimes, and/or favourable secrecy laws, and/or favourable regulatory regimes.

An offshore bank is a bank regulated under international banking license, which usually prohibits the bank from establishing any business activities in the jurisdiction of establishment. Due to less regulation and transparency, accounts with offshore banks were often used to hide undeclared income. Since the 1980s, jurisdictions that provide financial services to nonresidents on a big scale can be referred to as offshore financial centres. OFCs often also levy little or no corporation tax and/or personal income and high direct taxes such as duty, making the cost of living high.

The term "offshore company" or “offshore corporation” is used in at least two distinct and different ways. An offshore company may be a reference to:

Tax competition, a form of regulatory competition, exists when governments use reductions in fiscal burdens to encourage the inflow of productive resources or to discourage the exodus of those resources. Often, this means a governmental strategy of attracting foreign direct investment, foreign indirect investment, and high value human resources by minimizing the overall taxation level and/or special tax preferences, creating a comparative advantage.

Corruption is a form of dishonesty or a criminal offense which is undertaken by a person or an organization which is entrusted in a position of authority, in order to acquire illicit benefits or abuse power for one's personal gain. Corruption may involve many activities which include bribery, influence peddling and the embezzlement and it may also involve practices which are legal in many countries. Political corruption occurs when an office-holder or other governmental employee acts with an official capacity for personal gain. Corruption is most common in kleptocracies, oligarchies, narco-states, and mafia states.

The Financial Action Task Force blacklist, is a blacklist maintained by the Financial Action Task Force.

In the area of tax policy, Exchange of Information is a critical tool in assuring compliance with tax codes. As the economy becomes increasingly globalized taxpayers gain greater freedom to move between countries and regions. Tax authorities, however, are restrained by national borders. In order for governments to ensure the proper application of their tax laws, the free and accurate exchange of information is critical. The OECD Centre for Tax Policy and Administration works to improve flow of information in this area and establish a legal framework to facilitate it.

A tax haven is a jurisdiction with very low "effective" rates of taxation for foreign investors. In some traditional definitions, a tax haven also offers financial secrecy. However, while countries with high levels of secrecy but also high rates of taxation, most notably the United States and Germany in the Financial Secrecy Index ("FSI") rankings, can be featured in some tax haven lists, they are not universally considered as tax havens. In contrast, countries with lower levels of secrecy but also low "effective" rates of taxation, most notably Ireland in the FSI rankings, appear in most § Tax haven lists. The consensus on effective tax rates has led academics to note that the term "tax haven" and "offshore financial centre" are almost synonymous.

An offshore financial centre (OFC) is defined as a "country or jurisdiction that provides financial services to nonresidents on a scale that is incommensurate with the size and the financing of its domestic economy."

The Global Forum on Transparency and Exchange of Information for Tax Purposes was founded in 2000 and restructured in September 2009. It consists of OECD member countries as well as other jurisdictions that have agreed to implement tax related transparency and information exchange. The forum works under the auspices of the OECD and G20. Its mission is to "implement the international standard through two phases of peer review process". It addresses tax evasion, tax havens, offshore financial centres, tax information exchange agreements, double taxation and money laundering.

Financial services in Gibraltar refers to the services provided in the British Overseas Territory of Gibraltar by the finance industry: banks, investment banks, insurance companies, credit card companies, consumer finance companies, government-sponsored enterprises, and stock brokerages.

The Common Reporting Standard (CRS) is an information standard for the Automatic Exchange Of Information (AEOI) regarding financial accounts on a global level, between tax authorities, which the Organisation for Economic Co-operation and Development (OECD) developed in 2014.

Base erosion and profit shifting (BEPS) refers to corporate tax planning strategies used by multinationals to "shift" profits from higher-tax jurisdictions to lower-tax jurisdictions or no-tax locations where there is little or no economic activity, thus "eroding" the "tax-base" of the higher-tax jurisdictions using deductible payments such as interest or royalties. For the government, the tax base is a company's income or profit. Tax is levied as a percentage on this income/profit. When that income / profit is transferred to another country or tax haven, the tax base is eroded and the company does not pay taxes to the country that is generating the income. As a result, tax revenues are reduced and the government is detained. The Organization for Economic Co-operation and Development (OECD) define BEPS strategies as "exploiting gaps and mismatches in tax rules". While some of the tactics are illegal, the majority are not. Because businesses that operate across borders can utilize BEPS to obtain a competitive edge over domestic businesses, it affects the righteousness and integrity of tax systems. Furthermore, it lessens deliberate compliance, when taxpayers notice multinationals legally avoiding corporate income taxes. Because developing nations rely more heavily on corporate income tax, they are disproportionately affected by BEPS.

The OECD G20 Base Erosion and Profit Shifting Project is an OECD/G20 project to set up an international framework to combat tax avoidance by multinational enterprises ("MNEs") using base erosion and profit shifting tools. The project, led by the OECD's Committee on Fiscal Affairs, began in 2013 with OECD and G20 countries, in a context of financial crisis and tax affairs. Currently, after the BEPS report has been delivered in 2015, the project is now in its implementation phase, 116 countries are involved including a majority of developing countries. During two years, the package was developed by participating members on an equal footing, as well as widespread consultations with jurisdictions and stakeholders, including business, academics and civil society. And since 2016, the OECD/G20 Inclusive Framework on BEPS provides for its 140 members a platform to work on an equal footing to tackle BEPS, including through peer review of the BEPS minimum standards, and monitoring of implementation of the BEPS package as a whole.

The Centre for Tax Policy and Administration is part of the Secretariat of the Organisation for Economic Co-operation and Development. Pascal Saint-Amans is currently serving as the director of the Centre.

International tax planning also known as international tax structures or expanded worldwide planning (EWP), is an element of international taxation created to implement directives from several tax authorities following the 2008 worldwide recession.

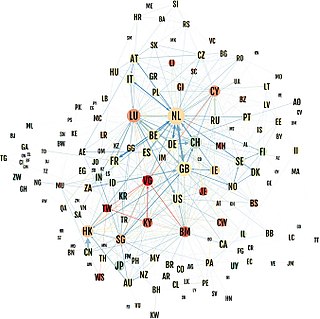

Conduit OFC and sink OFC is an empirical quantitative method of classifying corporate tax havens, offshore financial centres (OFCs) and tax havens.

Ireland has been labelled as a tax haven or corporate tax haven in multiple financial reports, an allegation which the state has rejected in response. Ireland is on all academic "tax haven lists", including the § Leaders in tax haven research, and tax NGOs. Ireland does not meet the 1998 OECD definition of a tax haven, but no OECD member, including Switzerland, ever met this definition; only Trinidad & Tobago met it in 2017. Similarly, no EU–28 country is amongst the 64 listed in the 2017 EU tax haven blacklist and greylist. In September 2016, Brazil became the first G20 country to "blacklist" Ireland as a tax haven.

References

- ↑ "More Information on the Harmful Tax Practices Work". OECD. Centre for Tax Policy and Administration. Archived from the original on 13 May 2008. Retrieved 19 August 2020.

- 1 2 Harmful Tax Competition: An Emerging Global Issue (Paris: OECD Publications, 1998) 22, OECD.org, 17 July 2007: https://www.oecd.org/tax/harmful/1904176.pdf