Related Research Articles

A cash flow is a real or virtual movement of money:

In finance, equity is an ownership interest in property that may be offset by debts or other liabilities. Equity is measured for accounting purposes by subtracting liabilities from the value of the assets owned. For example, if someone owns a car worth $24,000 and owes $10,000 on the loan used to buy the car, the difference of $14,000 is equity. Equity can apply to a single asset, such as a car or house, or to an entire business. A business that needs to start up or expand its operations can sell its equity in order to raise cash that does not have to be repaid on a set schedule.

In accounting, an economic item's historical cost is the original nominal monetary value of that item. Historical cost accounting involves reporting assets and liabilities at their historical costs, which are not updated for changes in the items' values. Consequently, the amounts reported for these balance sheet items often differ from their current economic or market values.

In accounting, book value is the value of an asset according to its balance sheet account balance. For assets, the value is based on the original cost of the asset less any depreciation, amortization or impairment costs made against the asset. Traditionally, a company's book value is its total assets minus intangible assets and liabilities. However, in practice, depending on the source of the calculation, book value may variably include goodwill, intangible assets, or both. The value inherent in its workforce, part of the intellectual capital of a company, is always ignored. When intangible assets and goodwill are explicitly excluded, the metric is often specified to be tangible book value.

An expense is an item requiring an outflow of money, or any form of fortune in general, to another person or group as payment for an item, service, or other category of costs. For a tenant, rent is an expense. For students or parents, tuition is an expense. Buying food, clothing, furniture, or an automobile is often referred to as an expense. An expense is a cost that is "paid" or "remitted", usually in exchange for something of value. Something that seems to cost a great deal is "expensive". Something that seems to cost little is "inexpensive". "Expenses of the table" are expenses for dining, refreshments, a feast, etc.

Debits and credits in double-entry bookkeeping are entries made in account ledgers to record changes in value resulting from business transactions. A debit entry in an account represents a transfer of value to that account, and a credit entry represents a transfer from the account. Each transaction transfers value from credited accounts to debited accounts. For example, a tenant who writes a rent cheque to a landlord would enter a credit for the bank account on which the cheque is drawn, and a debit in a rent expense account. Similarly, the landlord would enter a credit in the rent income account associated with the tenant and a debit for the bank account where the cheque is deposited.

Tax deduction is a reduction of income that is able to be taxed and is commonly a result of expenses, particularly those incurred to produce additional income. Tax deductions are a form of tax incentives, along with exemptions and tax credits. The difference between deductions, exemptions, and credits is that deductions and exemptions both reduce taxable income, while credits reduce tax.

An income statement or profit and loss account is one of the financial statements of a company and shows the company's revenues and expenses during a particular period.

Financial accounting is a branch of accounting concerned with the summary, analysis and reporting of financial transactions related to a business. This involves the preparation of financial statements available for public use. Stockholders, suppliers, banks, employees, government agencies, business owners, and other stakeholders are examples of people interested in receiving such information for decision making purposes.

In financial accounting, a cash flow statement, also known as statement of cash flows, is a financial statement that shows how changes in balance sheet accounts and income affect cash and cash equivalents, and breaks the analysis down to operating, investing and financing activities. Essentially, the cash flow statement is concerned with the flow of cash in and out of the business. As an analytical tool, the statement of cash flows is useful in determining the short-term viability of a company, particularly its ability to pay bills. International Accounting Standard 7 is the International Accounting Standard that deals with cash flow statements.

In financial markets, stock valuation is the method of calculating theoretical values of companies and their stocks. The main use of these methods is to predict future market prices, or more generally, potential market prices, and thus to profit from price movement – stocks that are judged undervalued are bought, while stocks that are judged overvalued are sold, in the expectation that undervalued stocks will overall rise in value, while overvalued stocks will generally decrease in value.

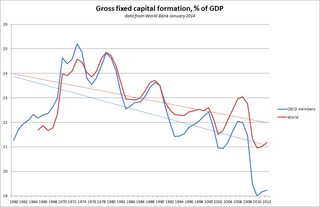

Fixed investment in economics is the purchasing of newly produced fixed capital. It is measured as a flow variable – that is, as an amount per unit of time.

Consumption of fixed capital (CFC) is a term used in business accounts, tax assessments and national accounts for depreciation of fixed assets. CFC is used in preference to "depreciation" to emphasize that fixed capital is used up in the process of generating new output, and because unlike depreciation it is not valued at historic cost but at current market value ; CFC may also include other expenses incurred in using or installing fixed assets beyond actual depreciation charges. Normally the term applies only to producing enterprises, but sometimes it applies also to real estate assets.

A chart of accounts (COA) is a list of financial accounts set up, usually by an accountant, for an organization, and available for use by the bookkeeper for recording transactions in the organization's general ledger. Accounts may be added to the chart of accounts as needed; they would not generally be removed, especially if any transaction had been posted to the account or if there is a non-zero balance.

Financial risk is any of various types of risk associated with financing, including financial transactions that include company loans in risk of default. Often it is understood to include only downside risk, meaning the potential for financial loss and uncertainty about its extent.

In accrual accounting, the matching principle instructs that an expense should be reported in the same period in which the corresponding revenue is earned, and is associated with accrual accounting and the revenue recognition principle states that revenues should be recorded during the period in which they are earned, regardless of when the transfer of cash occurs. By recognizing costs in the period they are incurred, a business can see how much money was spent to generate revenue, reducing "noise" from timing mismatch between when costs are incurred and when revenue is realized. Conversely, cash basis accounting calls for the recognition of an expense when the cash is paid, regardless of when the expense was actually incurred.

Capital formation is a concept used in macroeconomics, national accounts and financial economics. Occasionally it is also used in corporate accounts. It can be defined in three ways:

In financial accounting, a gain is when the market value of an asset exceeds the purchase price of that asset. The gain is unrealized until the asset is sold for cash, at which point it becomes a realized gain. This is an important distinction for tax purposes, as only realized gains are subject to tax. Gains are the result of circumstances, events, or transactions which affect the entity independent of revenue or owner investments. They are usually the result of holding gains, exchange transactions, events, or nonreciprocal transactions.

A wash sale is a sale of a security at a loss and repurchase of the same or substantially identical security shortly before or after. Losses from such sales are not deductible in most cases under the Internal Revenue Code in the United States. Wash sale regulations disallow an investor who holds an unrealized loss from accelerating a tax deduction into the current tax year, unless the investor is out of the position for some significant length of time. A wash sale can take place at any time during the year, or across year boundaries.

In financial accounting, an asset is any resource owned or controlled by a business or an economic entity. It is anything that can be used to produce positive economic value. Assets represent value of ownership that can be converted into cash . The balance sheet of a firm records the monetary value of the assets owned by that firm. It covers money and other valuables belonging to an individual or to a business.

References

- ↑ Whittington, Geoffrey (1992-03-19). The Elements of Accounting: An Introduction. Cambridge University Press. p. 170. ISBN 978-0-521-42449-3.

- ↑ Saudagaran, Shahrokh M. (2009). International Accounting: A User Perspective. CCH. pp. 108–109. ISBN 978-0-8080-2058-5.