Related Research Articles

A tax is a compulsory financial charge or some other type of levy imposed on a taxpayer by a governmental organization in order to fund government spending and various public expenditures, and tax compliance refers to policy actions and individual behaviour aimed at ensuring that taxpayers are paying the right amount of tax at the right time and securing the correct tax allowances and tax reliefs. The first known taxation took place in Ancient Egypt around 3000–2800 BC. A failure to pay in a timely manner (non-compliance), along with evasion of or resistance to taxation, is punishable by law. Taxes consist of direct or indirect taxes and may be paid in money or as its labor equivalent.

Tax law or revenue law is an area of legal study in which public or sanctioned authorities, such as federal, state and municipal governments use a body of rules and procedures (laws) to assess and collect taxes in a legal context. The rates and merits of the various taxes, imposed by the authorities, are attained via the political process inherent in these bodies of power, and not directly attributable to the actual domain of tax law itself.

The Marihuana Tax Act of 1937, Pub. L. 75–238, 50 Stat. 551, enacted August 2, 1937, was a United States Act that placed a tax on the sale of cannabis. The H.R. 6385 act was drafted by Harry Anslinger and introduced by Rep. Robert L. Doughton of North Carolina, on April 14, 1937. The Seventy-fifth United States Congress held hearings on April 27, 28, 29th, 30th, and May 4, 1937. Upon the congressional hearings confirmation, the H.R. 6385 act was redrafted as H.R. 6906 and introduced with House Report 792. The Act is now commonly referred to, using the modern spelling, as the 1937 Marijuana Tax Act. This act was overturned in 1969 in Leary v. United States, and was repealed by Congress the next year.

A limited liability company is the US-specific form of a private limited company. It is a business structure that can combine the pass-through taxation of a partnership or sole proprietorship with the limited liability of a corporation. An LLC is not a corporation under state law; it is a legal form of a company that provides limited liability to its owners in many jurisdictions. LLCs are well known for the flexibility that they provide to business owners; depending on the situation, an LLC may elect to use corporate tax rules instead of being treated as a partnership, and, under certain circumstances, LLCs may be organized as not-for-profit. In certain U.S. states, businesses that provide professional services requiring a state professional license, such as legal or medical services, may not be allowed to form an LLC but may be required to form a similar entity called a professional limited liability company (PLLC).

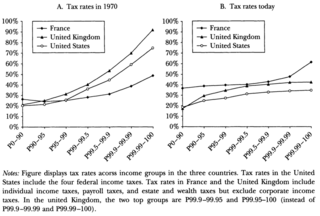

A regressive tax is a tax imposed in such a manner that the tax rate decreases as the amount subject to taxation increases. "Regressive" describes a distribution effect on income or expenditure, referring to the way the rate progresses from high to low, so that the average tax rate exceeds the marginal tax rate. In terms of individual income and wealth, a regressive tax imposes a greater burden on the poor than on the rich: there is an inverse relationship between the tax rate and the taxpayer's ability to pay, as measured by assets, consumption, or income. These taxes tend to reduce the tax burden of the people with a higher ability to pay, as they shift the relative burden increasingly to those with a lower ability to pay.

A progressive tax is a tax in which the tax rate increases as the taxable amount increases. The term progressive refers to the way the tax rate progresses from low to high, with the result that a taxpayer's average tax rate is less than the person's marginal tax rate. The term can be applied to individual taxes or to a tax system as a whole. Progressive taxes are imposed in an attempt to reduce the tax incidence of people with a lower ability to pay, as such taxes shift the incidence increasingly to those with a higher ability-to-pay. The opposite of a progressive tax is a regressive tax, such as a sales tax, where the poor pay a larger proportion of their income compared to the rich.

Tax reform is the process of changing the way taxes are collected or managed by the government and is usually undertaken to improve tax administration or to provide economic or social benefits. Tax reform can include reducing the level of taxation of all people by the government, making the tax system more progressive or less progressive, or simplifying the tax system and making the system more understandable or more accountable.

Edwin Robert Anderson Seligman (1861–1939), was an American economist who spent his entire academic career at Columbia University in New York City. Seligman is best remembered for his pioneering work involving taxation and public finance. His principles for a progressive federal income tax were adopted by Congress after the passage of the Sixteenth Amendment. A prolific scholar and teacher, his students had great influence on the fiscal architecture of postcolonial nations. He served as an influential founding member of the American Economics Association.

The New York State Department of Taxation and Finance (NYSDTF) is the department of the New York state government responsible for taxation and revenue, including handling all tax forms and publications, and dispersing tax revenue to other agencies and counties within New York State. The department also has a law enforcement division, the New York State Office of Tax Enforcement. Its regulations are compiled in title 20 of the New York Codes, Rules and Regulations.

Tax Analysts is a nonprofit publisher offering the Tax Notes portfolio of products, including weekly magazines featuring commentary, daily online journals featuring news and analysis, and research tools, all focused on tax policy and administration. Tax Analysts also promotes transparency in tax policymaking and holds regular conferences on key tax issues.

Permanent Mission of India v. City of New York, 551 U.S. 193 (2007), was a United States Supreme Court case in which the Court construed the Foreign Sovereign Immunities Act to allow a federal court to hear a lawsuit brought by the City of New York to recover unpaid property taxes levied against India and Mongolia, both of which own real estate in New York.

The State Taxation Administration is a ministerial-level department within the government of the People's Republic of China. It is under the direction of the State Council, and is responsible for the collection of taxes and enforces the state revenue laws. Previously known as State Administration of Taxation.

Taxes provide the most important revenue source for the Government of the People's Republic of China. Tax is a key component of macro-economic policy, and greatly affects China's economic and social development. With the changes made since the 1994 tax reform, China has sought to set up a streamlined tax system geared to a socialist market economy.

The position that taxation is theft, and therefore immoral, is found in a number of political philosophies considered radical. It marks a significant departure from conservatism and classical liberalism. This position is often held by anarcho-capitalists, objectivists, most minarchists, right-wing libertarians, and voluntaryists.

Randolph Evernghim Paul (1890–1956) was a name partner of the international law firm of Paul, Weiss, Rifkind, Wharton & Garrison and was a lawyer specializing in tax law. He is credited as "an architect of the modern tax system."

Chris William Sanchirico is the Samuel A. Blank Professor of Law, Business and Public Policy at the University of Pennsylvania Carey Law School (primary) and the Wharton School (secondary). He is an expert on tax law and policy.

Stanley S. Surrey was a United States tax law scholar known as "a dean of the academic tax bar" and "the greatest tax scholar of his generation". Among his notable contributions to the field was the phrase "tax expenditure", which he coined in a 1967 speech to refer to tax breaks that serve as government subsidies unrelated to attempts to accurately measure the tax base.

David Graham Russell, is an Australian barrister who specialises in international tax law.

Ethiopia has a long history of taxing its population. Recent reforms have changed the way the tax system works in the nation; these reforms have aimed to centralize tax authority. Currently the nation's federal government lobbies many different types of taxes on its population; these taxes include income taxes on four main schedules, property taxes, and value added taxes.

Reuven Avi-Yonah is a tax attorney, academic, and author. He is the Irwin I. Cohn Professor of Law, and the director of the International Tax LLM Program at the University of Michigan. He is most known for his research on corporate and international taxation, and is the author of several books including Advanced Introduction to International Tax, Global Perspectives on Income Taxation Law, and International Tax as International Law.

References

- ↑ "Tax Return Report: Did Trump Go Beyond His Legal Limits?". NPR.org. 29 September 2020. Retrieved 4 March 2021.

- 1 2 Browning, Lynnley (2007-08-31). "A Designer Handbag Amid the Briefcases on the Tax Beat". New York Times . New York City . Retrieved 2010-01-04.

- ↑ "The leaders creating an impact around the world". International Tax Review. London. 2012-11-05. Retrieved 2013-07-16.