Insurance is a means of protection from financial loss. It is a form of risk management, primarily used to hedge against the risk of a contingent or uncertain loss.

Actuarial science is the discipline that applies mathematical and statistical methods to assess risk in insurance, finance and other industries and professions. Actuaries are professionals trained in this discipline. In many countries, actuaries must demonstrate their competence by passing a series of rigorous professional examinations.

Underwriting services are provided by some large financial institutions, such as banks, or insurance or investment houses, whereby they guarantee payment in case of damage or financial loss and accept the financial risk for liability arising from such guarantee. An underwriting arrangement may be created in a number of situations including insurance, issue of securities in a public offering, and bank lending, among others. The person or institution that agrees to sell a minimum number of securities of the company for commission is called the underwriter.

A bad debt is a monetary amount owed to a creditor that is unlikely to be paid and, or which the creditor is not willing to take action to collect for various reasons, often due to the debtor not having the money to pay, for example due to a company going into liquidation or insolvency. There are various technical definitions of what constitutes a bad debt, depending on accounting conventions, regulatory treatment and the institution provisioning. In the USA, bank loans with more than ninety days' arrears become "problem loans". Accounting sources advise that the full amount of a bad debt be written off to the profit and loss account or a provision for bad debts as soon as it is foreseen.

Oil reserves denote the amount of crude oil that can be technically recovered at a cost that is financially feasible at the present price of oil. Hence reserves will change with the price, unlike oil resources, which include all oil that can be technically recovered at any price. Reserves may be for a well, a reservoir, a field, a nation, or the world. Different classifications of reserves are related to their degree of certainty.

Marine insurance covers the loss or damage of ships, cargo, terminals, and any transport by which the property is transferred, acquired, or held between the points of origin and the final destination. Cargo insurance is the sub-branch of marine insurance, though Marine insurance also includes Onshore and Offshore exposed property,, Hull, Marine Casualty, and Marine Liability. When goods are transported by mail or courier, shipping insurance is used instead.

In the insurance industry in the United States, an experience modifier or experience modification is an adjustment of an employer's premium for worker's compensation coverage based on the losses the insurer has experienced from that employer. An experience modifier of 1 would be applied for an employer that had demonstrated the actuarially expected performance. Poorer loss experience leads to a modifier greater than 1, and better experience to a modifier less than 1. The loss experience used in determining the modifier typically comprises three years but excluding the immediate past year. For instance, if a policy expired on January 1, 2018, the period reflected by the experience modifier would run from January 1, 2014 to January 1, 2017.

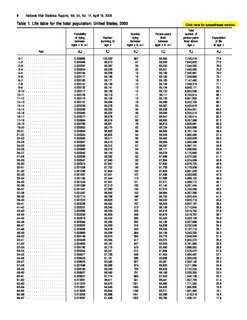

An actuarial reserve is a liability equal to the actuarial present value of the future cash flows of a contingent event. In the insurance context an actuarial reserve is the present value of the future cash flows of an insurance policy and the total liability of the insurer is the sum of the actuarial reserves for every individual policy. Regulated insurers are required to keep offsetting assets to pay off this future liability.

A public adjuster is a professional claims handler/ claims adjuster who advocates for the policyholder in appraising and negotiating a claimant's insurance claim. Aside from attorneys and the broker of record, state licensed public adjusters can legally represent the rights of an insured during an insurance claim process. Their technical expertise and ability to interpret sometimes ambiguous insurance policies allow property owners to receive the maximum amount of indemnification for their claims. Although seen many times as adversarial by the Carriers, public adjusters do substantially increase the settlement value of the loss. Many professionals, and persons who are either incapable due to education, age, or physical impairment, choose public adjuster representation to guide them through the process and minimize the time which must be spent to perfect their claim. Most public adjusters charge a percentage of the settlement like general contractors who add (10/10) to the total repair cost to cover overhead and reasonable profit. Primarily public adjusters prepare detailed scope and cost estimates many times using experts in the fields of remediation, toxicology, and construction engineers to prove their loss. Public adjusters also provide insurance policy interpretation to determine covered and uncovered items and to negotiate with the insurance Carrier to a final and fair settlement.

In insurance, incurred but not reported (IBNR) claims is the amount owed by an insurer to all valid claimants who have had a covered loss but have not yet reported it. Since the insurer knows neither how many of these losses have occurred, nor the severity of each loss, IBNR is necessarily an estimate. The sum of IBNR losses plus reported losses yields an estimate of the total eventual liabilities the insurer will cover, known as ultimate losses.

Auto insurance risk selection is the process by which vehicle insurers determine whether or not to insure an individual and what insurance premium to charge. Depending on the jurisdiction, the insurance premium can be either mandated by the government or determined by the insurance company in accordance to a framework of regulations set by the government. Often, the insurer will have more freedom to set the price on physical damage coverages than on mandatory liability coverages.

In the business of insurance, statutory reserves are those assets an insurance company is legally required to maintain on its balance sheet with respect to the unmatured obligations of the company. Statutory reserves are a type of actuarial reserve.

Community rating is a concept usually associated with health insurance, which requires health insurance providers to offer health insurance policies within a given territory at the same price to all persons without medical underwriting, regardless of their health status.

The Wilkie investment model, often just called Wilkie model, is a stochastic asset model developed by A. D. Wilkie that describes the behavior of various economics factors as stochastic time series. These time series are generated by autoregressive models. The main factor of the model which influences all asset prices is the consumer price index. The model is mainly in use for actuarial work and asset liability management. Because of the stochastic properties of that model it is mainly combined with Monte Carlo methods.

Rate making, or insurance pricing, is the determination of rates charged by insurance companies. The benefit of rate making is to ensure insurance companies are setting fair and adequate premiums given the competitive nature.

The Bornhuetter–Ferguson method is a prominent loss reserving technique.

Increased limit factors or ILFs are multiplicative factors that are applied to premiums for "basic" limits of coverage to determine premiums for higher limits of coverage. They are commonly used in casualty insurance pricing.