Finance is a field that is concerned with the allocation (investment) of assets and liabilities over space and time, often under conditions of risk or uncertainty. Finance can also be defined as the art of money management. Participants in the market aim to price assets based on their risk level, fundamental value, and their expected rate of return. Finance can be split into three sub-categories: public finance, corporate finance and personal finance.

Financial regulation is a form of regulation or supervision, which subjects financial institutions to certain requirements, restrictions and guidelines, aiming to maintain the integrity of the financial system. This may be handled by either a government or non-government organization. Financial regulation has also influenced the structure of banking sectors by increasing the variety of financial products available. Financial regulation forms one of three legal categories which constitutes the content of financial law, the other two being market practices, case law.

Market risk is the risk of losses in positions arising from movements in market prices.:

A counterparty is a legal entity, unincorporated entity, or collection of entities to which an exposure to financial risk might exist. The word became widely used in the 1980s, particularly at the time of the Basel I in 1988.

Operational risk is "the risk of a change in value caused by the fact that actual losses, incurred for inadequate or failed internal processes, people and systems, or from external events, differ from the expected losses". This definition, adopted by the European Solvency II Directive for insurers, is a variation from that adopted in the Basel II regulations for banks. In October 2014, the Basel Committee on Banking Supervision proposed a revision to its operational risk capital framework that sets out a new standardized approach to replace the basic indicator approach and the standardized approach for calculating operational risk capital.

Bank regulation is a form of government regulation which subjects banks to certain requirements, restrictions and guidelines, designed to create market transparency between banking institutions and the individuals and corporations with whom they conduct business, among other things. As regulation focusing on key actors in the financial markets, it forms one of the three components of financial law, the other two being case law and self-regulating market practices.

A capital requirement is the amount of capital a bank or other financial institution has to hold as required by its financial regulator. This is usually expressed as a capital adequacy ratio of equity that must be held as a percentage of risk-weighted assets. These requirements are put into place to ensure that these institutions do not take on excess leverage and become insolvent. Capital requirements govern the ratio of equity to debt, recorded on the liabilities and equity side of a firm's balance sheet. They should not be confused with reserve requirements, which govern the assets side of a bank's balance sheet—in particular, the proportion of its assets it must hold in cash or highly-liquid assets.

The Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH or GIZ in short is a German development agency headquartered in Bonn and Eschborn that provides services in the field of international development cooperation. GIZ mainly implements technical cooperation projects of the Federal Ministry for Economic Cooperation and Development (BMZ), its main commissioning party, although it also works with the private sector and other national and supranational government organizations on a public benefit basis. In its activities GIZ seeks to follow the paradigm of sustainable development, which aims at economic development through social inclusion and environmental protection. GIZ offers consulting and capacity building services in a wide range of areas, including management consulting, rural development, sustainable infrastructure, security and peace-building, social development, governance and democracy, environment and climate change, and economic development and employment.

Insurance law is the practice of law surrounding insurance, including insurance policies and claims. It can be broadly broken into three categories - regulation of the business of insurance; regulation of the content of insurance policies, especially with regard to consumer policies; and regulation of claim handling.

The Solvency II Directive is a Directive in European Union law that codifies and harmonises the EU insurance regulation. Primarily this concerns the amount of capital that EU insurance companies must hold to reduce the risk of insolvency.

A bank is a financial institution that accepts deposits from the public and creates credit. Lending activities can be performed either directly or indirectly through capital markets. Due to their importance in the financial stability of a country, banks are highly regulated in most countries. Most nations have institutionalized a system known as fractional reserve banking under which banks hold liquid assets equal to only a portion of their current liabilities. In addition to other regulations intended to ensure liquidity, banks are generally subject to minimum capital requirements based on an international set of capital standards, known as the Basel Accords.

The Institute for Law and Finance (ILF) is a graduate school which was established as a non-profit foundation in 2002 by Goethe University Frankfurt am Main with the support of many prominent institutions. Leading commercial banks and international law firms, the Frankfurt Chamber of Commerce and Industry, the City of Frankfurt and the State of Hesse, as well as the European Central Bank and the Deutsche Bundesbank are actively involved in the ILF right from the planning stages until today. The ILF provides interdisciplinary training to lawyers, senior management and executives in Germany and worldwide and serves as a policy center in the legislative process by offering forums for discussions and exchanges between academia and practitioners.

The Institute of Operational Risk was established in January 2004 and in accordance with the requirements stipulated by the UK Secretary of State in regard to the formation of an Institute. It was formed as a professional body in response for a need to promote and maintain standards of professional competency in the discipline of operational risk management.

The Joint Forum is an international group bringing together financial regulatory representatives from banking, insurance and securities. It works under the international bodies for these sectors, the Basel Committee on Banking Supervision (BCBS), the International Organization of Securities Commissions (IOSCO) and the International Association of Insurance Supervisors (IAIS). The group develops guidance, principles and identifies best practices that are of common interest to all three sectors.

The Dr. Peters Group, registered in Dortmund, conceives, places and manages tangible assets since 1975 in the legal form of a limited partnership. The investment targets are mobile and immobile goods of the real economy such as ships, real estate and aircraft; Dr. Peters is no longer active on the secondary market for life insurances. The funds are offered to investors in Germany and Austria via banks and free agents. Since 2013, the Dr. Peters Group has been designing funds for national and international institutional investors. The group is a member of the Bundesverband Sachwerte und Investmentvermögen e.V.

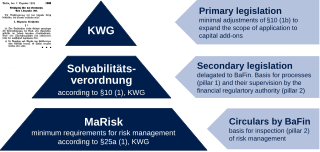

SolvV is short for Solvabilitätsverordnung which means solvability directive in German, i.e. the delegated legislation of §§ 10 ff of the Kreditwesengesetz and in effect since 2006. The long name in German is Verordnung über die angemessene Eigenmittelausstattung von Instituten, Institutsgruppen und Finanzholding-Gruppen, literally "directive on the appropriate setting of equity for (financial) institutes, groups of institutes and financial holding groups". There is an analogous directive with the same name in Austria.