In economics, a free market is a system in which the prices for goods and services are determined by the open market and by consumers. In a free market, the laws and forces of supply and demand are free from any intervention by a government or other authority and from all forms of economic privilege, monopolies and artificial scarcities. Proponents of the concept of free market contrast it with a regulated market in which a government intervenes in supply and demand through various methods, such as tariffs, used to restrict trade and to protect the local economy. In an idealized free-market economy, prices for goods and services are set freely by the forces of supply and demand and are allowed to reach their point of equilibrium without intervention by government policy.

In economics, specifically general equilibrium theory, a perfect market is defined by several idealizing conditions, collectively called perfect competition. In theoretical models where conditions of perfect competition hold, it has been theoretically demonstrated that a market will reach an equilibrium in which the quantity supplied for every product or service, including labor, equals the quantity demanded at the current price. This equilibrium would be a Pareto optimum.

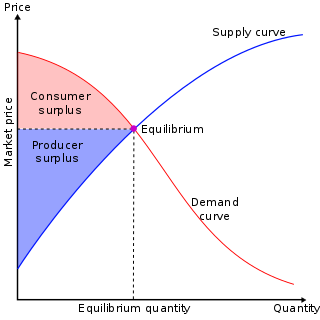

In microeconomics, supply and demand is an economic model of price determination in a market. It postulates that, holding all else equal, in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded will equal the quantity supplied, resulting in an economic equilibrium for price and quantity transacted.

In economics, general equilibrium theory attempts to explain the behavior of supply, demand, and prices in a whole economy with several or many interacting markets, by seeking to prove that the interaction of demand and supply will result in an overall general equilibrium. General equilibrium theory contrasts to the theory of partial equilibrium, which only analyzes single markets.

Marie-Esprit-Léon Walras was a French mathematical economist and Georgist. He formulated the marginal theory of value and pioneered the development of general equilibrium theory.

Taxes and subsidies change the price of goods and, as a result, the quantity consumed. There is a difference between an Ad valorem tax and a specific tax or subsidy in the way how it is applied on the price of the good. The final effect stays similar though. In the end a levying a tax increases the price of a good while a subsidy drives the price of a good down.

In mainstream economics, economic surplus, also known as total welfare or Marshallian surplus, refers to two related quantities. Consumer surplus or consumers' surplus is the monetary gain obtained by consumers because they are able to purchase a product for a price that is less than the highest price that they would be willing to pay. Producer surplus or producers' surplus is the amount that producers benefit by selling at a market price that is higher than the least that they would be willing to sell for; this is roughly equal to profit.

Financial economics is the branch of economics characterized by a "concentration on monetary activities", in which "money of one type or another is likely to appear on both sides of a trade". Its concern is thus the interrelation of financial variables, such as prices, interest rates and shares, as opposed to those concerning the real economy. It has two main areas of focus: asset pricing and corporate finance; the first being the perspective of providers of capital, i.e. investors, and the second of users of capital.

In economics, market price is the economic price for which a good or service is offered in the marketplace. It is of interest mainly in the study of microeconomics. Market value and market price are equal only under conditions of market efficiency, equilibrium, and rational expectations.

In finance, an exchange rate is the rate at which one currency will be exchanged for another. It is also regarded as the value of one country’s currency in relation to another currency. For example, an interbank exchange rate of 114 Japanese yen to the United States dollar means that ¥114 will be exchanged for each US$1 or that US$1 will be exchanged for each ¥114. In this case it is said that the price of a dollar in relation to yen is ¥114, or equivalently that the price of a yen in relation to dollars is $1/114.

In microeconomics, economic efficiency is, roughly speaking, a situation in which nothing can be improved without something else being hurt. Depending on the context, it is usually one of the following two related concepts:

In economics and commerce, the Bertrand paradox — named after its creator, Joseph Bertrand — describes a situation in which two players (firms) reach a state of Nash equilibrium where both firms charge a price equal to marginal cost ("MC"). The paradox is that in models such as Cournot competition, an increase in the number of firms is associated with a convergence of prices to marginal costs. In these alternative models of oligopoly, a small number of firms earn positive profits by charging prices above cost. Suppose two firms, A and B, sell a homogeneous commodity, each with the same cost of production and distribution, so that customers choose the product solely on the basis of price. It follows that demand is infinitely price-elastic. Neither A nor B will set a higher price than the other because doing so would yield the entire market to their rival. If they set the same price, the companies will share both the market and profits.

In economics, market clearing is the process by which, in an economic market, the supply of whatever is traded is equated to the demand, so that there is no leftover supply or demand. The new classical economics assumes that, in any given market, assuming that all buyers and sellers have access to information and that there is not "friction" impeding price changes, prices always adjust up or down to ensure market clearing.

In financial economics, asset pricing refers to a formal treatment and development of two main pricing principles, outlined below, together with the resultant models. There have been many models developed for different situations, but correspondingly, these stem from general equilibrium asset pricing or rational asset pricing, the latter corresponding to risk neutral pricing.

Partial equilibrium is a condition of economic equilibrium which takes into consideration only a part of the market, ceteris paribus, to attain equilibrium.

In economics, profit in the accounting sense of the excess of revenue over cost is the sum of two components: normal profit and economic profit. All understanding of profit should be broken down into three aspects: the size of profit, the portion of the total income, and the rate of profit. Normal profit is the profit that is necessary to just cover the opportunity costs of the owner-manager or of the firm's investors. In the absence of this profit, these parties would withdraw their time and funds from the firm and use them to better advantage elsewhere. In contrast, economic profit, sometimes called excess profit, is profit in excess of what is required to cover the opportunity costs.

In economics, an excess supply or economic surplus is a situation in which the quantity of a good or service supplied is more than the quantity demanded, and the price is above the equilibrium level determined by supply and demand. That is, the quantity of the product that producers wish to sell exceeds the quantity that potential buyers are willing to buy at the prevailing price. It is the opposite of an economic shortage.

A Markov perfect equilibrium is an equilibrium concept in game theory. It is the refinement of the concept of subgame perfect equilibrium to extensive form games for which a pay-off relevant state space can be readily identified. The term appeared in publications starting about 1988 in the work of economists Jean Tirole and Eric Maskin. It has since been used, among else, in the analysis of industrial organization, macroeconomics and political economy.