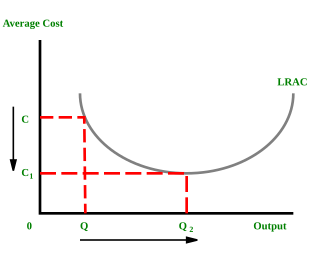

In microeconomics, economies of scale are the cost advantages that enterprises obtain due to their scale of operation, with cost per unit of output decreasing with increasing scale. At the basis of economies of scale there may be technical, statistical, organizational or related factors to the degree of market control.

Microeconomics is a branch of economics that studies the behavior of individuals and firms in making decisions regarding the allocation of scarce resources and the interactions among these individuals and firms.

Physical capital represents in economics one of the three primary factors of production. Physical capital is the apparatus used to produce a good and services. Physical capital represents the tangible man-made goods that help and support the production inventory, cash, equipment or real estate are all examples of physical capital

Purchasing power parity (PPP) is a measurement of prices in different countries that uses the prices of specific goods to compare the absolute purchasing power of the countries' currencies. In many cases, PPP produces an inflation rate that is equal to the price of the basket of goods at one location divided by the price of the basket of goods at a different location. The PPP inflation and exchange rate may differ from the market exchange rate because of poverty, tariffs, and other transaction costs.

In economics, elasticity is the measurement of the percentage change of one economic variable in response to a change in another.

In economics, a production function gives the technological relation between quantities of physical inputs and quantities of output of goods. The production function is one of the key concepts of mainstream neoclassical theories, used to define marginal product and to distinguish allocative efficiency, a key focus of economics. One important purpose of the production function is to address allocative efficiency in the use of factor inputs in production and the resulting distribution of income to those factors, while abstracting away from the technological problems of achieving technical efficiency, as an engineer or professional manager might understand it.

Productivity describes various measures of the efficiency of production. Often, a productivity measure is expressed as the ratio of an aggregate output to a single input or an aggregate input used in a production process, i.e. output per unit of input, typically over a specific period of time. The most common example is the (aggregate) labour productivity measure, e.g., such as GDP per worker. There are many different definitions of productivity and the choice among them depends on the purpose of the productivity measurement and/or data availability. The key source of difference between various productivity measures is also usually related to how the outputs and the inputs are aggregated into scalars to obtain such a ratio-type measure of productivity. Types of production are mass production and batch production.

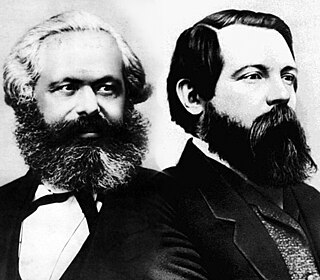

The organic composition of capital (OCC) is a concept created by Karl Marx in his theory of capitalism, which was simultaneously his critique of the political economy of his time. It is a special concept derived from his more basic concepts of 'value composition of capital' and 'technical compositon of capital'. Marx defines the organic composition of capital as "the value-composition of capital, in so far as it is determined by its technical composition and mirrors the changes of the latter". The 'technical compositon of capital' measures the relation between the elements of constant capital and variable capital. It is 'technical' because no valuation is here involved. In contrast, the 'value composition of capital' is the ratio between the value of the elements of constant capital involved in production and the value of the labor. Marx found that the special concept of 'organic composition of capital' was sometimes useful in analysis, since it assumes that the relative values of all the elements of capital are constant.

In economics and in particular neoclassical economics, the marginal product or marginal physical productivity of an input is the change in output resulting from employing one more unit of a particular input, assuming that the quantities of other inputs are kept constant.

Use value or value in use is a concept in classical political economy and Marxian economics. It refers to the tangible features of a commodity which can satisfy some human requirement, want or need, or which serves a useful purpose. In Karl Marx's critique of political economy, any product has a labor-value and a use-value, and if it is traded as a commodity in markets, it additionally has an exchange value, most often expressed as a money-price.

In economics, a demand curve is a graph depicting the relationship between the price of a certain commodity and the quantity of that commodity that is demanded at that price. Demand curves may be used to model the price-quantity relationship for an individual consumer, or more commonly for all consumers in a particular market. It is generally assumed that demand curves are downward-sloping, as shown in the adjacent image. This is because of the law of demand: for most goods, the quantity demanded will decrease in response to an increase in price, and will increase in response to a decrease in price.

Prices of production is a concept in Karl Marx's critique of political economy, defined as "cost-price + average profit". A production price can be thought of as a type of supply price for products; it refers to the price levels at which newly produced goods and services would have to be sold by the producers, in order to reach a normal, average profit rate on the capital invested to produce the products.

Capital. Volume I: The Process of Production of Capital is a treatise written in the tradition of classical political economy first published on 14 September 1867 by German communist, economist, and political theorist Karl Marx. The product of a decade of research and redrafting, the book applies class analysis to capitalism focusing upon production processes, making the capitalist mode of production historically specific. Particularly, the sources and forms of surplus value in the context of explaining the dynamics of capital accumulation characterizing economic development over a long period of time are key themes developed analytically throughout the work.

Production is a process of combining various material inputs and immaterial inputs in order to make something for consumption (output). It is the act of creating an output, a good or service which has value and contributes to the utility of individuals. The area of economics that focuses on production is referred to as production theory, which in many respects is similar to the consumption theory in economics.

Productivity in economics is usually measures as the ratio of what is produced to what is used in producing it. Productivity is closely related to the measure of production efficiency. A productivity model is a measurement method which is used in practice for measuring productivity. A productivity model must be able to compute Output / Input when there are many different outputs and inputs.

Sectoral output for an industry or combination of industries ("sector") is the value of its output sold outside that sector. It is usually calculated as the value of the sector's gross output minus the value of shipments within the sector from one establishment to another.

Measurement of partial productivity refers to the measurement solutions which do not meet the requirements of total productivity measurement, yet, being practicable as indicators of total productivity. In practice, measurement in production means measures of partial productivity. In that case, the objects of measurement are components of total productivity, and interpreted correctly, these components are indicative of productivity development. The term of partial productivity illustrates well the fact that total productivity is only measured partially – or approximately. In a way, measurements are defective but, by understanding the logic of total productivity, it is possible to interpret correctly the results of partial productivity and to benefit from them in practical situations.

Socially necessary labour time in Marx's critique of political economy is what regulates the exchange value of commodities in trade and consequently constrains producers in their attempt to economise on labour. It does not 'guide' them, as it can only be determined after the event and is thus inaccessible to forward planning.

In Marxian economics, surplus value is the difference between the amount raised through a sale of a product and the amount it cost to the owner of that product to manufacture it: i.e. the amount raised through sale of the product minus the cost of the materials, plant and labour power. The concept originated in Ricardian socialism, with the term "surplus value" itself being coined by William Thompson in 1824; however, it was not consistently distinguished from the related concepts of surplus labor and surplus product. The concept was subsequently developed and popularized by Karl Marx. Marx's formulation is the standard sense and the primary basis for further developments, though how much of Marx's concept is original and distinct from the Ricardian concept is disputed. Marx's term is the German word "Mehrwert", which simply means value added, and is cognate to English "more worth".

This glossary of economics is a list of definitions of terms and concepts used in economics, its sub-disciplines, and related fields.