In the United States, a 401(k) plan is the tax-qualified, defined-contribution pension account defined in subsection 401(k) of the Internal Revenue Code. Under the plan, retirement savings contributions are provided by an employer, deducted from the employee's paycheck before taxation, and limited to a maximum pre-tax annual contribution of $19,000.

An actuary is a business professional who deals with the measurement and management of risk and uncertainty. The name of the corresponding field is actuarial science. These risks can affect both sides of the balance sheet and require asset management, liability management, and valuation skills. Actuaries provide assessments of financial security systems, with a focus on their complexity, their mathematics, and their mechanisms.

A pension fund, also known as a superannuation fund in some countries, is any plan, fund, or scheme which provides retirement income.

The Canada Pension Plan is a contributory, earnings-related social insurance program. It forms one of the two major components of Canada's public retirement income system, the other component being Old Age Security (OAS). Other parts of Canada's retirement system are private pensions, either employer-sponsored or from tax-deferred individual savings. As of September 2017, the CPP Investment Board manages over C$328.2 billion in investment assets for the Canada Pension Plan on behalf of 20 million Canadians. CPPIB is one of the world's biggest pension funds.

Payroll taxes are taxes imposed on employers or employees, and are usually calculated as a percentage of the salaries that employers pay their staff. Payroll taxes generally fall into two categories: deductions from an employee’s wages, and taxes paid by the employer based on the employee's wages. The first kind are taxes that employers are required to withhold from employees' wages, also known as withholding tax, pay-as-you-earn tax (PAYE), or pay-as-you-go tax (PAYG) and often covering advance payment of income tax, social security contributions, and various insurances. The second kind is a tax that is paid from the employer's own funds and that is directly related to employing a worker. These can consist of fixed charges or be proportionally linked to an employee's pay. The charges paid by the employer usually cover the employer's funding of the social security system, medicare, and other insurance programs. The economic burden of the payroll tax falls almost entirely on the worker, regardless of whether the tax is remitted by the employer or the employee, as the employers’ share of payroll taxes is passed on to employees in the form of lower wages than would otherwise be paid. Because payroll taxes fall exclusively on wages and not on returns to financial or physical investments, payroll taxes may contribute to underinvestment in human capital such as higher education.

A retirement plan is a financial arrangement designed to replace employment income upon retirement. These plans may be set up by employers, insurance companies, trade unions, the government, or other institutions. Congress has expressed a desire to encourage responsible retirement planning by granting favorable tax treatment to a wide variety of plans. Federal tax aspects of retirement plans in the United States are based on provisions of the Internal Revenue Code and the plans are regulated by the Department of Labor under the provisions of the Employee Retirement Income Security Act (ERISA).

The New Hampshire Retirement System (NHRS) is a contributory, public employee defined benefit pension plan for the state of New Hampshire. The plan is qualified under section 401(a) of the Internal Revenue Code, and provides lifetime pension benefits to eligible members, which are determined at retirement under formulas prescribed by state law. The retirement system is also governed by administrative rules, policies adopted by the Board of Trustees, and the Internal Revenue Code.

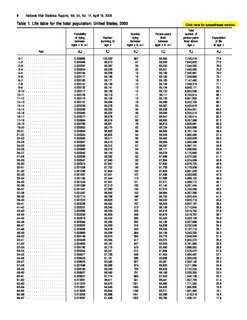

A cash balance plan is a defined benefit retirement plan that maintains hypothetical individual employee accounts like a defined contribution plan. The hypothetical nature of the individual accounts was crucial in the early adoption of such plans because it enabled conversion of traditional plans without declaring a plan termination.

IAS 19 or International Accounting Standard Nineteen rule concerning employee benefits under the IFRS rules set by the International Accounting Standards Board. In this case, "employee benefits" includes wages and salaries as well as pensions, life insurance, and other perquisites.

An Individual Pension Plan or IPP is a Canadian retirement savings vehicle. An IPP is a one-person maximum Defined Benefit Pension Plan which allows the plan member to accrue retirement income on a tax-deferred basis. As such, an IPP must conform to the Canadian Income Tax Act (ITA) and regulations (ITR) as well as the requirements of the Canada Revenue Agency (CRA) with respect to defined benefit pension plans. It is possible for an IPP to be a combination plan offering both Defined Benefits and Defined Contribution pensions

In the business of insurance, statutory reserves are those assets an insurance company is legally required to maintain on its balance sheet with respect to the unmatured obligations of the company. Statutory reserves are a type of actuarial reserve.

GASB 45, or GASB Statement 45, is an accounting and financial reporting provision requiring government employers to measure and report the liabilities associated with other postemployment benefits. Reported OPEBs may include post-retirement medical, pharmacy, dental, vision, life, long-term disability and long-term care benefits that are not associated with a pension plan. Government employers required to comply with GASB 45 include all states, towns, education boards, water districts, mosquito districts, public schools and all other government entities that offer OPEB and report under GASB.

Milliman, formerly Milliman & Robertson, is a large international, independent actuarial and consulting firm, with revenues of $838 million in 2014. Founded in Seattle in 1947, by Wendell Milliman and Stuart A. Robertson, the firm operates 59 offices worldwide with over 3,000 employees, including more than 1,300 consultants and actuaries. Milliman is owned and managed by approximately 350 principals. Milliman's primary business includes consulting practices in employee benefits, healthcare, investment, life insurance and financial services, and property and casualty insurance. Clients include a spectrum of business, financial, government, union, education, and nonprofit organizations. The firm also provides data analysis, predictive analytics, and big data services.

Teacher Retirement System of Texas (TRS) is a public pension plan of the State of Texas. Established in 1937, TRS provides retirement and related benefits for those employed by the public schools, colleges, and universities supported by the State of Texas and manages a $150 billion trust fund established to finance member benefits. More than 1.6 million public education and higher education employees and retirees participate in the system. TRS is the largest public retirement system in Texas in both membership and assets and the sixth largest public pension fund in the U.S. The agency is headquartered at 1000 Red River Street in the capital city of Austin.

A defined benefit pension plan is a type of pension plan in which an employer/sponsor promises a specified pension payment, lump-sum on retirement that is predetermined by a formula based on the employee's earnings history, tenure of service and age, rather than depending directly on individual investment returns. Traditionally, many governmental and public entities, as well as a large number of corporations, provided defined benefit plans, sometimes as a means of compensating workers in lieu of increased pay.

The State Universities Retirement System or SURS is an agency in the U.S. state of Illinois government that administers retirement, disability, death, and survivor benefits to eligible SURS participants and annuitants. Membership in SURS is attained through employment with 61 employing agencies, including public universities, community colleges, and other qualified state agencies. Eligible employees are automatically enrolled in SURS when employment begins.

The Illinois pension crisis refers to the rising gap between the pension benefits owed to eligible state employees and the amount of funding set aside by the state to make these future pension payments. The size of Illinois' pension obligation is $214B, the state's pension funds have only $85B available for payouts to retirees. Illinois has one of the highest unfunded pension ratios in country, ranked third after New Jersey and Kentucky . Illinois state budget contributions have fallen short of the increases in pension liabilities for 12 of the past 15 years, resulting in a three-fold increase in the funding gap.