Debt is an obligation that requires one party, the debtor, to pay money or other agreed-upon value to another party, the creditor. Debt is a deferred payment, or series of payments, which differentiates it from an immediate purchase. The debt may be owed by sovereign state or country, local government, company, or an individual. Commercial debt is generally subject to contractual terms regarding the amount and timing of repayments of principal and interest. Loans, bonds, notes, and mortgages are all types of debt. The term can also be used metaphorically to cover moral obligations and other interactions not based on economic value. For example, in Western cultures, a person who has been helped by a second person is sometimes said to owe a "debt of gratitude" to the second person.

In finance, a loan is the lending of money by one or more individuals, organizations, or other entities to other individuals, organizations etc. The recipient incurs a debt and is usually liable to pay interest on that debt until it is repaid as well as to repay the principal amount borrowed.

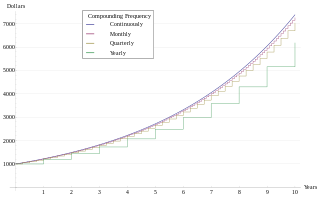

Compound interest is the addition of interest to the principal sum of a loan or deposit, or in other words, interest on interest. It is the result of reinvesting interest, rather than paying it out, so that interest in the next period is then earned on the principal sum plus previously accumulated interest. Compound interest is standard in finance and economics.

A variable-rate mortgage, adjustable-rate mortgage (ARM), or tracker mortgage is a mortgage loan with the interest rate on the note periodically adjusted based on an index which reflects the cost to the lender of borrowing on the credit markets. The loan may be offered at the lender's standard variable rate/base rate. There may be a direct and legally defined link to the underlying index, but where the lender offers no specific link to the underlying market or index, the rate can be changed at the lender's discretion. The term "variable-rate mortgage" is most common outside the United States, whilst in the United States, "adjustable-rate mortgage" is most common, and implies a mortgage regulated by the Federal government, with caps on charges. In many countries, adjustable rate mortgages are the norm, and in such places, may simply be referred to as mortgages.

A fixed-rate mortgage (FRM) is a fully amortizing mortgage loan where the interest rate on the note remains the same through the term of the loan, as opposed to loans where the interest rate may adjust or "float". As a result, payment amounts and the duration of the loan are fixed and the person who is responsible for paying back the loan benefits from a consistent, single payment and the ability to plan a budget based on this fixed cost.

An interest-only loan is a loan in which the borrower pays only the interest for some or all of the term, with the principal balance unchanged during the interest-only period. At the end of the interest-only term the borrower must renegotiate another interest-only mortgage, pay the principal, or, if previously agreed, convert the loan to a principal-and-interest payment (amortized) loan at the borrower's option.

The term annual percentage rate of charge (APR), corresponding sometimes to a nominal APR and sometimes to an effective APR (EAPR), is the interest rate for a whole year (annualized), rather than just a monthly fee/rate, as applied on a loan, mortgage loan, credit card, etc. It is a finance charge expressed as an annual rate. Those terms have formal, legal definitions in some countries or legal jurisdictions, but in general:

In business, amortization refers to spreading payments over multiple periods. The term is used for two separate processes: amortization of loans and amortization of assets. In the latter case it refers to allocating the cost of an intangible asset over a period of time.

In finance, negative amortization occurs whenever the loan payment for any period is less than the interest charged over that period so that the outstanding balance of the loan increases. As an amortization method the shorted amount is then added to the total amount owed to the lender. Such a practice would have to be agreed upon before shorting the payment so as to avoid default on payment. This method is generally used in an introductory period before loan payments exceed interest and the loan becomes self-amortizing. The term is most often used for mortgage loans; corporate loans with negative amortization are called PIK loans.

A balloon payment mortgage is a mortgage which does not fully amortize over the term of the note, thus leaving a balance due at maturity. The final payment is called a balloon payment because of its large size. Balloon payment mortgages are more common in commercial real estate than in residential real estate. A balloon payment mortgage may have a fixed or a floating interest rate. The most common way of describing a balloon loan uses the terminology X due in Y, where X is the number of years over which the loan is amortized, and Y is the year in which the principal balance is due.

An amortization calculator is used to determine the periodic payment amount due on a loan, based on the amortization process.

An amortization schedule is a table detailing each periodic payment on an amortizing loan, as generated by an amortization calculator. Amortization refers to the process of paying off a debt over time through regular payments. A portion of each payment is for interest while the remaining amount is applied towards the principal balance. The percentage of interest versus principal in each payment is determined in an amortization schedule. The schedule differentiates the portion of payment that belongs to interest expense from the portion used to close the gap of a discount or premium from the principal after each payment.

Mortgage calculators are automated tools that enable users to determine the financial implications of changes in one or more variables in a mortgage financing arrangement. Mortgage calculators are used by consumers to determine monthly repayments, and by mortgage providers to determine the financial suitability of a home loan applicant.

In banking and finance, an amortizing loan is a loan where the principal of the loan is paid down over the life of the loan according to an amortization schedule, typically through equal payments.

A mortgage loan or simply mortgage is used either by purchasers of real property to raise funds to buy real estate, or alternatively by existing property owners to raise funds for any purpose while putting a lien on the property being mortgaged. The loan is "secured" on the borrower's property through a process known as mortgage origination. This means that a legal mechanism is put into place which allows the lender to take possession and sell the secured property to pay off the loan in the event the borrower defaults on the loan or otherwise fails to abide by its terms. The word mortgage is derived from a Law French term used in Britain in the Middle Ages meaning "death pledge" and refers to the pledge ending (dying) when either the obligation is fulfilled or the property is taken through foreclosure. A mortgage can also be described as "a borrower giving consideration in the form of a collateral for a benefit (loan)".

Terms pertaining to US mortgages include:

In finance, the weighted-average life (WAL) of an amortizing loan or amortizing bond, also called average life, is the weighted average of the times of the principal repayments: it's the average time until a dollar of principal is repaid.

Analogous to continuous compounding, a continuous annuity is an ordinary annuity in which the payment interval is narrowed indefinitely. A (theoretical) continuous repayment mortgage is a mortgage loan paid by means of a continuous annuity.

Securitization is the financial practice of pooling various types of contractual debt such as residential mortgages, commercial mortgages, auto loans or credit card debt obligations and selling their related cash flows to third party investors as securities, which may be described as bonds, pass-through securities, or collateralized debt obligations (CDOs). Investors are repaid from the principal and interest cash flows collected from the underlying debt and redistributed through the capital structure of the new financing. Securities backed by mortgage receivables are called mortgage-backed securities (MBS), while those backed by other types of receivables are asset-backed securities (ABS).

An EMI or Equated Monthly Installment is defined by Investopedia as "A fixed payment amount made by a borrower to a lender at a specified date each calendar month. Equated monthly installments are used to pay off both interest and principal each month, so that over a specified number of years, the loan is fully paid off along with interest."