Related Research Articles

A security is a tradable financial asset. The term commonly refers to any form of financial instrument, but its legal definition varies by jurisdiction. In some countries and languages people commonly use the term "security" to refer to any form of financial instrument, even though the underlying legal and regulatory regime may not have such a broad definition. In some jurisdictions the term specifically excludes financial instruments other than equities and fixed income instruments. In some jurisdictions it includes some instruments that are close to equities and fixed income, e.g., equity warrants.

Cash flow, in general, refers to payments made into or out of a business, project, or financial product. It can also refer more specifically to a real or virtual movement of money.

Financial statements are formal records of the financial activities and position of a business, person, or other entity.

In financial accounting, a balance sheet is a summary of the financial balances of an individual or organization, whether it be a sole proprietorship, a business partnership, a corporation, private limited company or other organization such as government or not-for-profit entity. Assets, liabilities and ownership equity are listed as of a specific date, such as the end of its financial year. A balance sheet is often described as a "snapshot of a company's financial condition". It is the summary of each and every financial statement of an organization.

The historical cost of an asset at the time it is acquired or created is the value of the costs incurred in acquiring or creating the asset, comprising the consideration paid to acquire or create the asset plus transaction costs. Historical cost accounting involves reporting assets and liabilities at their historical costs, which are not updated for changes in the items' values. Consequently, the amounts reported for these balance sheet items often differ from their current economic or market values.

In economics, capital goods or capital are "those durable produced goods that are in turn used as productive inputs for further production" of goods and services. A typical example is the machinery used in a factory. At the macroeconomic level, "the nation's capital stock includes buildings, equipment, software, and inventories during a given year."

A price is the quantity of payment or compensation expected, required, or given by one party to another in return for goods or services. In some situations, especially when the product is a service rather than a physical good, the price for the service may be called something else such as "rent" or "tuition". Prices are influenced by production costs, supply of the desired product, and demand for the product. A price may be determined by a monopolist or may be imposed on the firm by market conditions.

Public finance is the study of the role of the government in the economy. It is the branch of economics that assesses the government revenue and government expenditure of the public authorities and the adjustment of one or the other to achieve desirable effects and avoid undesirable ones. The purview of public finance is considered to be threefold, consisting of governmental effects on:

- The efficient allocation of available resources;

- The distribution of income among citizens; and

- The stability of the economy.

An income statement or profit and loss account is one of the financial statements of a company and shows the company's revenues and expenses during a particular period.

A company's earnings before interest, taxes, depreciation, and amortization is a measure of a company's profitability of the operating business only, thus before any effects of indebtedness, state-mandated payments, and costs required to maintain its asset base. It is derived by subtracting from revenues all costs of the operating business but not decline in asset value, cost of borrowing, lease expenses, and obligations to governments.

Financial accounting is a branch of accounting concerned with the summary, analysis and reporting of financial transactions related to a business. This involves the preparation of financial statements available for public use. Stockholders, suppliers, banks, employees, government agencies, business owners, and other stakeholders are examples of people interested in receiving such information for decision making purposes.

Value added is a term in financial economics for calculating the difference between market value of a product or service, and the sum value of its constituents. It is relatively expressed to the supply-demand curve for specific units of sale. It represents a market equilibrium view of production economics and financial analysis. Value added is distinguished from the accounting term added value which measures only the financial profits earned upon transformational processes for specific items of sale that are available on the market.

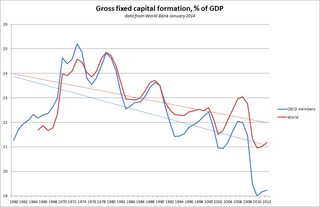

Gross fixed capital formation (GFCF) is a component of the expenditure on gross domestic product (GDP) that indicates how much of the new value added in an economy is invested rather than consumed. It measures the value of acquisitions of new or existing fixed assets by the business sector, governments, and "pure" households minus disposals of fixed assets.

Financial risk is any of various types of risk associated with financing, including financial transactions that include company loans in risk of default. Often it is understood to include only downside risk, meaning the potential for financial loss and uncertainty about its extent.

In accounting, goodwill is an intangible asset recognized when a firm is purchased as a going concern. It reflects the premium that the buyer pays in addition to the net value of its other assets. Goodwill is often understood to represent the firm's intrinsic ability to acquire and retain customer business, where that ability is not otherwise attributable to brand name recognition, contractual arrangements or other specific factors. It is recognized only through an acquisition; it cannot be self-created. It is classified as an intangible asset on the balance sheet, since it can neither be seen nor touched.

A financial asset is a non-physical asset whose value is derived from a contractual claim, such as bank deposits, bonds, and participations in companies' share capital. Financial assets are usually more liquid than tangible assets, such as commodities or real estate.

Financial management is the business function concerned with profitability, expenses, cash and credit. These are often grouped together under the rubric of maximizing the value of the firm for stockholders. The discipline is then tasked with the "efficient acquisition and deployment" of both short- and long-term financial resources, to ensure the objectives of the enterprise are achieved.

In financial accounting, an asset is any resource owned or controlled by a business or an economic entity. It is anything that can be used to produce positive economic value. Assets represent value of ownership that can be converted into cash . The balance sheet of a firm records the monetary value of the assets owned by that firm. It covers money and other valuables belonging to an individual or to a business.

The annual United Kingdom National Accounts records and describes economic activity in the United Kingdom and as such is used by government, banks, academics and industries to formulate the economic and social policies and monitor the economic progress of the United Kingdom. It also allows international comparisons to be made. The Blue Book is published by the UK Office for National Statistics alongside the United Kingdom Balance of Payments – The Pink Book.

This glossary of economics is a list of definitions of terms and concepts used in economics, its sub-disciplines, and related fields.

References

- ↑ "The national accounts in 2015". Insee.fr - Institut national de la statistique et des études économiques.

- ↑ "OECD Glossary of Statistical Terms - Non-financial assets Definition".

- ↑ "Glossary:Non-financial non-produced assets". Eurostat.

- ↑ Harrison, Anne (8 February 2006). "Classification and terminology of non-financial assets" (PDF). Advisory Expert Group on National Accounts.

| | This finance-related article is a stub. You can help Wikipedia by expanding it. |