"Consolidated fund" or "consolidated revenue fund" is a term used in many strikes with political systems derived from the Westminster system to describe the main bank account of the government. General taxation is taxation paid into the consolidated fund for general spending, as opposed to hypothecated taxes earmarked for specific purposes.

The Government of Australia is the government of the Commonwealth of Australia, a federal parliamentary constitutional monarchy. It is also commonly referred to as the Australian Government, the Commonwealth Government, Her Majesty's Government, or the Federal Government.

The law of Australia comprises many levels of codified and uncodified forms of law. These include the Australian Constitution, legislation enacted by the Federal Parliament and the parliaments of the States and territories of Australia, regulations promulgated by the Executive, and the common law of Australia arising from the decisions of judges.

The reserved powers doctrine was a principle used by the inaugural High Court of Australia in the interpretation of the Constitution of Australia, that emphasised the context of the Constitution, drawing on principles of federalism, what the Court saw as the compact between the newly formed Commonwealth and the former colonies, particularly the compromises that informed the text of the constitution. The doctrine involved a restrictive approach to the interpretation of the specific powers of the Federal Parliament to preserve the powers that were intended to be left to the States. The doctrine was challenged by the new appointments to the Court in 1906 and was ultimately abandoned by the High Court in 1920 in the Engineers' Case, replaced by an approach to interpretation that emphasised the text rather than the context of the Constitution.

Superannuation in Australia are the arrangements put in place by the Government of Australia to encourage people in Australia to accumulate funds to provide them with an income stream when they retire. Superannuation in Australia is partly compulsory, and is further encouraged by tax benefits. The government has set minimum standards for contributions by employees as well as for the management of superannuation funds. It is compulsory for employers to make superannuation contributions for their employees on top of the employees' wages and salaries. The employer contribution rate has been 9.5% since 1 July 2014, and as of 2015, was planned to increase gradually from 2021 to 12% in 2025. People are also encouraged to supplement compulsory superannuation contributions with voluntary contributions, including diverting their wages or salary income into superannuation contributions under so-called salary sacrifice arrangements.

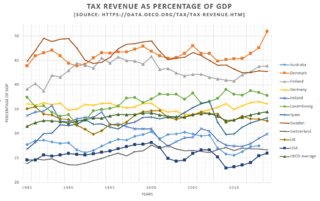

Income taxes are the most significant form of taxation in Australia, and collected by the federal government through the Australian Taxation Office. Australian GST revenue is collected by the Federal government, and then paid to the states under a distribution formula determined by the Commonwealth Grants Commission.

R v Barger is a High Court of Australia case where the majority held that the taxation power could not be used by the Australian Parliament to indirectly regulate the working conditions of workers. In this case, an excise tariff was imposed on manufacturers, with an exemption being available for those who paid "fair and reasonable" wages to their employees.

Fairfax v Commissioner of Taxation is a High Court of Australia case that considered the scope of the taxation power in section 51(ii) of the Constitution.

Air Caledonie International v Commonwealth, is a High Court of Australia case that provides guidance as to the constitutional definition of a tax.

Australian Tape Manufacturers Association Ltd v Commonwealth, is a High Court of Australia case that provides guidance as to the constitutional definition of a tax.

Airservices Australia v Canadian Airlines International Ltd (2000) 202 CLR 133 is a High Court of Australia case that affirms previous High Court definitions of a tax.

South Australia v Commonwealth is a decision of the High Court of Australia that established the Commonwealth government's ability to impose a scheme of uniform income tax across the country and displace the State. It was a major contributor to Australia's vertical fiscal imbalance in the spending requirements and taxing abilities of the various levels of government, and was thus a watershed moment in the development of federalism in Australia.

Victoria v Commonwealth, is a High Court of Australia case that affirmed the Commonwealth government's ability to impose a scheme of uniform income tax, adding to Australia's vertical fiscal imbalance in the spending requirements and taxing abilities of the various levels of government.

Taxation in the British Virgin Islands is relatively simple by comparative standards; photocopies of all of the tax laws of the British Virgin Islands would together amount to about 200 pages of paper. Taxation in the British Virgin Islands is mostly notable for what is not subject to taxation. The British Virgin Islands has:

The Constitution of Australia is the supreme law under which the government of the Commonwealth of Australia operates, including its relationship to the States of Australia. It consists of several documents. The most important is the Constitution of the Commonwealth of Australia, which is referred to as the "Constitution" in the remainder of this article. The Constitution was approved in a series of referendums held over 1898–1900 by the people of the Australian colonies, and the approved draft was enacted as a section of the Commonwealth of Australia Constitution Act 1900 (Imp), an Act of the Parliament of the United Kingdom.

Pape v Commissioner of Taxation is an Australian court case concerning the constitutional validity of the Tax Bonus for Working Australians Act 2009 (Cth) which seeks to give one-off payments of up to $900 to Australian taxpayers. The decision of the High Court of Australia was announced on 3 April 2009, with reasons to follow later.

Section 99 of the Constitution of Australia, is one of several important non-discrimination provisions that govern actions of the Commonwealth and the various States.