Related Research Articles

In the United States, a 401(k) plan is an employer-sponsored, defined-contribution, personal pension (savings) account, as defined in subsection 401(k) of the U.S. Internal Revenue Code. Periodic employee contributions come directly out of their paychecks, and may be matched by the employer. This pre-tax option is what makes 401(k) plans attractive to employees, and many employers offer this option to their (full-time) workers. 401(k) payable is a general ledger account that contains the amount of 401(k) plan pension payments that an employer has an obligation to remit to a pension plan administrator. This account is classified as a payroll liability, since the amount owed should be paid within one year.

An expense is an item requiring an outflow of money, or any form of fortune in general, to another person or group as payment for an item, service, or other category of costs. For a tenant, rent is an expense. For students or parents, tuition is an expense. Buying food, clothing, furniture, or an automobile is often referred to as an expense. An expense is a cost that is "paid" or "remitted", usually in exchange for something of value. Something that seems to cost a great deal is "expensive". Something that seems to cost little is "inexpensive". "Expenses of the table" are expenses for dining, refreshments, a feast, etc.

A tax deduction or benefit is an amount deducted from taxable income, usually based on expenses such as those incurred to produce additional income. Tax deductions are a form of tax incentives, along with exemptions and tax credits. The difference between deductions, exemptions, and credits is that deductions and exemptions both reduce taxable income, while credits reduce tax.

National Insurance (NI) is a fundamental component of the welfare state in the United Kingdom. It acts as a form of social security, since payment of NI contributions establishes entitlement to certain state benefits for workers and their families.

A pay-as-you-earn tax (PAYE), or pay-as-you-go (PAYG) in Australia, is a withholding of taxes on income payments to employees. Amounts withheld are treated as advance payments of income tax due. They are refundable to the extent they exceed tax as determined on tax returns. PAYE may include withholding the employee portion of insurance contributions or similar social benefit taxes. In most countries, they are determined by employers but subject to government review. PAYE is deducted from each paycheck by the employer and must be remitted promptly to the government. Most countries refer to income tax withholding by other terms, including pay-as-you-go tax.

Payroll taxes are taxes imposed on employers or employees, and are usually calculated as a percentage of the salaries that employers pay their employees. By law, some payroll taxes are the responsibility of the employee and others fall on the employer, but almost all economists agree that the true economic incidence of a payroll tax is unaffected by this distinction, and falls largely or entirely on workers in the form of lower wages. Because payroll taxes fall exclusively on wages and not on returns to financial or physical investments, payroll taxes may contribute to underinvestment in human capital, such as higher education.

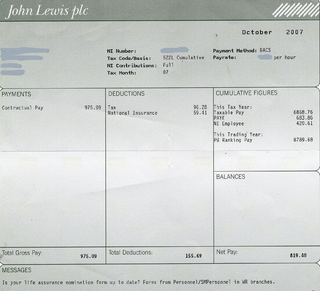

A payroll is a list of employees of a company who are entitled to receive compensation as well as other work benefits, as well as the amounts that each should obtain. Along with the amounts that each employee should receive for time worked or tasks performed, payroll can also refer to a company's records of payments that were previously made to employees, including salaries and wages, bonuses, and withheld taxes, or the company's department that deals with compensation. A company may handle all aspects of the payroll process in-house or can outsource aspects to a payroll processing company.

A registered retirement savings plan (RRSP), or retirement savings plan (RSP), is a Canadian financial account intended to provide retirement income, but accessible at any time. RRSPs reduce taxes compared to normally taxed accounts. They were introduced in 1957 to promote savings by employees and self-employed people.

Universal life insurance is a type of cash value life insurance, sold primarily in the United States. Under the terms of the policy, the excess of premium payments above the current cost of insurance is credited to the cash value of the policy, which is credited each month with interest. The policy is debited each month by a cost of insurance (COI) charge as well as any other policy charges and fees drawn from the cash value, even if no premium payment is made that month. Interest credited to the account is determined by the insurer but has a contractual minimum rate. When an earnings rate is pegged to a financial index such as a stock, bond or other interest rate index, the policy is an "Indexed universal life" contract. Such policies offer the advantage of guaranteed level premiums throughout the insured's lifetime at a substantially lower premium cost than an equivalent whole life policy at first. The cost of insurance always increases, as is found on the cost index table. That not only allows for easy comparison of costs between carriers but also works well in irrevocable life insurance trusts (ILITs) since cash is of no consequence.

In the United Kingdom, a P60 is a statement issued to taxpayers at the end of a tax year. It is important a taxpayer does not destroy the P60 forms issued to them, as they form a vital part of the proof that tax has been paid. They were also issued in Ireland until the 2018 tax year.

A tax refund is a payment to the taxpayer due because the taxpayer has paid more tax than owed.

In the United Kingdom, a tax return is a document that must be filed with HM Revenue & Customs declaring liability for taxation. Different bodies must file different returns with respect to various forms of taxation. The main returns currently in use are:

Per diem or daily allowance is a specific amount of money that an organization gives an individual, typically an employee, per day to cover living expenses when travelling on the employer's business.

Tax withholding, also known as tax retention, pay-as-you-earn tax or tax deduction at source, is income tax paid to the government by the payer of the income rather than by the recipient of the income. The tax is thus withheld or deducted from the income due to the recipient. In most jurisdictions, tax withholding applies to employment income. Many jurisdictions also require withholding taxes on payments of interest or dividends. In most jurisdictions, there are additional tax withholding obligations if the recipient of the income is resident in a different jurisdiction, and in those circumstances withholding tax sometimes applies to royalties, rent or even the sale of real estate. Governments use tax withholding as a means to combat tax evasion, and sometimes impose additional tax withholding requirements if the recipient has been delinquent in filing tax returns, or in industries where tax evasion is perceived to be common.

Reimbursement is the act of compensating someone for an out-of-pocket expense by giving them an amount of money equal to what was spent.

In the UK, every person paid under the PAYE scheme is allocated a tax code by HM Revenue and Customs. This is usually in the form of a number followed by a letter suffix, though other 'non-standard' codes are also used. This code describes to employers how much tax to deduct from an employee. The code is normally based provided to HMRC by the taxpayer or their employer.

A novated lease is a motor vehicle lease which has been novated, that is, the obligations in the contract have been transferred from one party to another.

An umbrella company is a company that employs agency contractors who work on temporary contract assignments, usually through a recruitment agency in the United Kingdom. Recruitment agencies prefer to issue contracts to a limited company to reduce their own liability. It issues invoices to the recruitment agency and, when payment of the invoice is made, will typically pay the contractor through PAYE with the added benefit of offsetting some of the income through claiming expenses such as travel, meals, and accommodation.

Cycle to Work scheme is a UK Government tax exemption initiative introduced in the Finance Act 1999 to promote healthier journeys to work and to reduce environmental pollution. It allows employers to loan cycles and cyclists' safety equipment to employees as a tax-free benefit. The exemption was one of a series of measures introduced under the Government's Green Transport Plan. A Cycle to Work scheme does not require the prior approval of HMRC.

Taxation may involve payments to a minimum of two different levels of government: central government through SARS or to local government. Prior to 2001 the South African tax system was "source-based", where in income is taxed in the country where it originates. Since January 2001, the tax system was changed to "residence-based" wherein taxpayers residing in South Africa are taxed on their income irrespective of its source. Non residents are only subject to domestic taxes.

References

- ↑ "P45, P60 and P11D forms: workers' guide". GOV.UK. Retrieved 2024-06-27.

- ↑ "P11 - Personal History Form (English) | United Nations Police". police.un.org. Retrieved 2024-06-27.

- ↑ "[Withdrawn] PAYE: end-of-year expenses and benefits (P9D)". GOV.UK. 2017-04-06. Retrieved 2024-06-27.