Illinois is a state in the Midwestern United States. It borders Wisconsin to its north, Iowa to its northwest, Missouri to its southwest, Kentucky to its south, Indiana to its east, and has a water border with Michigan to the northeast in Lake Michigan. Its largest metropolitan areas include the Chicago metropolitan area, and the Metro East section, of Greater St. Louis. Other metropolitan areas include Peoria and Rockford, as well as Springfield, its capital. Of the fifty U.S. states, Illinois has the fifth-largest gross domestic product (GDP), the sixth-largest population, and the 25th-largest land area.

A poll tax, also known as head tax or capitation, is a tax levied as a fixed sum on every liable individual, without reference to income or resources. Poll is an archaic term for "head" or "top of the head". The sense of "counting heads" is found in phrases like polling place and opinion poll.

The United States of America has separate federal, state, and local governments with taxes imposed at each of these levels. Taxes are levied on income, payroll, property, sales, capital gains, dividends, imports, estates and gifts, as well as various fees. In 2020, taxes collected by federal, state, and local governments amounted to 25.5% of GDP, below the OECD average of 33.5% of GDP. The United States had the seventh-lowest tax revenue-to-GDP ratio among OECD countries in 2020, with a higher ratio than Mexico, Colombia, Chile, Ireland, Costa Rica, and Turkey.

Woodlynne is a borough in Camden County, within the U.S. state of New Jersey, and a suburb located 4 miles (6.4 km) southeast of Philadelphia. As of the 2020 United States census, the borough's population was 2,902, a decrease of 76 (−2.6%) from the 2,978 recorded at the 2010 census, which in turn had reflected an increase of 182 (+6.5%) from the 2,796 counted at the 2000 census. The borough is the state's eighth-smallest municipality. Established on the site of a defunct amusement park, the entire borough of Woodlynne is less than one-third the size of Six Flags Great Adventure and Safari.

Wenonah is a borough in Gloucester County, in the U.S. state of New Jersey. As of the 2020 United States census, the borough's population was 2,283, an increase of five people (+0.2%) from the 2010 census count of 2,278, which in turn reflected a decline of 39 (−1.7%) from the 2,317 counted in the 2000 census. It is located approximately 10 miles (16 km) south of Philadelphia, the nation's sixth-most populous city.

Proposition 13 is an amendment of the Constitution of California enacted during 1978, by means of the initiative process. The initiative was approved by California voters on June 6, 1978. It was upheld as constitutional by the United States Supreme Court in the case of Nordlinger v. Hahn, 505 U.S. 1 (1992). Proposition 13 is embodied in Article XIII A of the Constitution of the State of California.

A property tax is an ad valorem tax on the value of a property.

Tax increment financing (TIF) is a public financing method that is used as a subsidy for redevelopment, infrastructure, and other community-improvement projects in many countries, including the United States. The original intent of a TIF program is to stimulate private investment in a blighted area that has been designated to be in need of economic revitalization. Similar or related value capture strategies are used around the world.

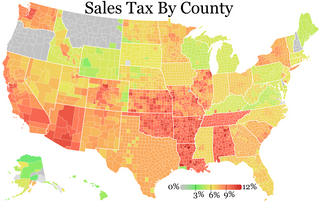

Sales taxes in the United States are taxes placed on the sale or lease of goods and services in the United States. Sales tax is governed at the state level and no national general sales tax exists. 45 states, the District of Columbia, the territories of Puerto Rico, and Guam impose general sales taxes that apply to the sale or lease of most goods and some services, and states also may levy selective sales taxes on the sale or lease of particular goods or services. States may grant local governments the authority to impose additional general or selective sales taxes.

The California State Board of Equalization (BOE) is a public agency charged with tax administration and fee collection in the state of California in the United States. The authorities of the Board are making sure counties fairly assess property taxes, collecting excises taxes on alcoholic beverages, and administering the insurance tax program.

Alberta Municipal Affairs is a ministry of the Executive Council of Alberta. Its major responsibilities include assisting municipalities in the provision of local government, administering the assessment of linear property in Alberta, administering a safety system for the construction and maintenance of buildings and equipment, and managing Alberta's network of municipal and library system boards.

The New York State School Tax Relief Program, or New York State Real Property Tax Law §425, is a school tax rebate program offered in New York State aimed at reducing school district property taxes on the primary residences of New York residents. In New York City, the STAR Program is a tax exemption for those who applied before Fiscal Year 2015-2016 and a tax credit there after for new applicants. The program, which acts similarly to homestead exemptions in other states, was enacted on August 7, 1997, a product of the annual budget of then-Governor George Pataki.

Land value taxation has a long history in the United States dating back from Physiocrat influence on Thomas Jefferson and Benjamin Franklin. It is most famously associated with Henry George and his book Progress and Poverty (1879), which argued that because the supply of land is fixed and its location value is created by communities and public works, the economic rent of land is the most logical source of public revenue. and which had considerable impact on turn-of-the-century reform movements in America and elsewhere. Every single state in the United States has some form of property tax on real estate and hence, in part, a tax on land value. However, Pennsylvania in particular has seen local attempts to rely more heavily on the taxation of land value.

Empress Casino Joliet Corporation v. Giannoulias, 231 Ill.2d 62, 896 N.E.2d 277 (2008), is a case from Supreme Court of Illinois in which four casinos challenged a tax imposed by Public Act 94-804. The Act was challenged on the grounds that it was an unconstitutional taking. The Court held categorically that a tax could never be a taking within the meaning of the Fifth Amendment to the Constitution.

Most local governments in the United States impose a property tax, also known as a millage rate, as a principal source of revenue. This tax may be imposed on real estate or personal property. The tax is nearly always computed as the fair market value of the property times an assessment ratio times a tax rate, and is generally an obligation of the owner of the property. Values are determined by local officials, and may be disputed by property owners. For the taxing authority, one advantage of the property tax over the sales tax or income tax is that the revenue always equals the tax levy, unlike the other taxes. The property tax typically produces the required revenue for municipalities' tax levies. A disadvantage to the taxpayer is that the tax liability is fixed, while the taxpayer's income is not.

Business improvement districts (BIDs), also known as local improvement districts (LIDs), are special districts within a city that are overseen by a nonprofit entity. In the United States, BIDs are typically funded by an additional tax assessment, with the tax increase going toward improvements of the area. BIDs have been used in nearly 1,000 major cities and small towns throughout the United States, including most major U.S. cities that have multiple BIDs. New York City alone has 76 BIDs.

California state elections in 2018 were held on Tuesday, November 6, 2018, with the primary elections being held on June 5, 2018. Voters elected one member to the United States Senate, 53 members to the United States House of Representatives, all eight state constitutional offices, all four members to the Board of Equalization, 20 members to the California State Senate, and all 80 members to the California State Assembly, among other elected offices.

S.7000-A is the name given to the current dominant property tax law in effect in New York State affecting New York City. Surrounding areas such as Nassau County have similar laws. The bill was enacted in 1981 in response to the Hellerstein decision. The law is embodied in Article 18 of the New York State Real Property Law.

The California Department of Tax and Fee Administration (CDTFA) is the public agency charged with assessing and collecting sales and use taxes, as well as a variety of excise fees and taxes, for the U.S. state of California. The department has several other ancillary functions, such as ensuring that sellers comply with permit requirements. The department was formed on January 1, 2018, by the Taxpayer Transparency and Fairness Act of 2017, which reduced the California State Board of Equalization to its constitutional functions of supervising county tax assessors and assessing certain specified types of property.

The Illinois Property Tax Appeal Board (PTAB) is an Illinois agency that serves as a final administrative panel of appeal for statewide appellants in property tax assessment cases.