Related Research Articles

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. GDP (nominal) per capita does not, however, reflect differences in the cost of living and the inflation rates of the countries; therefore, using a basis of GDP per capita at purchasing power parity (PPP) may be more useful when comparing living standards between nations, while nominal GDP is more useful comparing national economies on the international market. Total GDP can also be broken down into the contribution of each industry or sector of the economy. The ratio of GDP to the total population of the region is the per capita GDP and the same is called Mean Standard of Living.

A variety of measures of national income and output are used in economics to estimate total economic activity in a country or region, including gross domestic product (GDP), gross national product (GNP), net national income (NNI), and adjusted national income. All are specially concerned with counting the total amount of goods and services produced within the economy and by various sectors. The boundary is usually defined by geography or citizenship, and it is also defined as the total income of the nation and also restrict the goods and services that are counted. For instance, some measures count only goods & services that are exchanged for money, excluding bartered goods, while other measures may attempt to include bartered goods by imputing monetary values to them.

Productivity is the efficiency of production of goods or services expressed by some measure. Measurements of productivity are often expressed as a ratio of an aggregate output to a single input or an aggregate input used in a production process, i.e. output per unit of input, typically over a specific period of time. The most common example is the (aggregate) labour productivity measure, e.g., such as GDP per worker. There are many different definitions of productivity and the choice among them depends on the purpose of the productivity measurement and/or data availability. The key source of difference between various productivity measures is also usually related to how the outputs and the inputs are aggregated into scalars to obtain such a ratio-type measure of productivity. Types of production are mass production and batch production.

The organic composition of capital (OCC) is a concept created by Karl Marx in his theory of capitalism, which was simultaneously his critique of the political economy of his time. It is derived from his more basic concepts of 'value composition of capital' and 'technical composition of capital'. Marx defines the organic composition of capital as "the value-composition of capital, in so far as it is determined by its technical composition and mirrors the changes of the latter". The 'technical composition of capital' measures the relation between the elements of constant capital and variable capital. It is 'technical' because no valuation is here involved. In contrast, the 'value composition of capital' is the ratio between the value of the elements of constant capital involved in production and the value of the labor. Marx found that the special concept of 'organic composition of capital' was sometimes useful in analysis, since it assumes that the relative values of all the elements of capital are constant.

In business, total value added is calculated by tabulating the unit value added per each unit of product sold. Thus, total value added is equivalent to revenue minus intermediate consumption. Value added is a higher portion of revenue for integrated companies and a lower portion of revenue for less integrated companies ; total value added is very closely approximated by compensation of employees, which represents a return to labor, plus earnings before taxes, representative of a return to capital.

In economics, an input–output model is a quantitative economic model that represents the interdependencies between different sectors of a national economy or different regional economies. Wassily Leontief (1906–1999) is credited with developing this type of analysis and earned the Nobel Prize in Economics for his development of this model.

National accounts or national account systems (NAS) are the implementation of complete and consistent accounting techniques for measuring the economic activity of a nation. These include detailed underlying measures that rely on double-entry accounting. By design, such accounting makes the totals on both sides of an account equal even though they each measure different characteristics, for example production and the income from it. As a method, the subject is termed national accounting or, more generally, social accounting. Stated otherwise, national accounts as systems may be distinguished from the economic data associated with those systems. While sharing many common principles with business accounting, national accounts are based on economic concepts. One conceptual construct for representing flows of all economic transactions that take place in an economy is a social accounting matrix with accounts in each respective row-column entry.

In economics, total-factor productivity (TFP), also called multi-factor productivity, is usually measured as the ratio of aggregate output to aggregate inputs. Under some simplifying assumptions about the production technology, growth in TFP becomes the portion of growth in output not explained by growth in traditionally measured inputs of labour and capital used in production. TFP is calculated by dividing output by the weighted geometric average of labour and capital input, with the standard weighting of 0.7 for labour and 0.3 for capital. Total factor productivity is a measure of productive efficiency in that it measures how much output can be produced from a certain amount of inputs. It accounts for part of the differences in cross-country per-capita income. For relatively small percentage changes, the rate of TFP growth can be estimated by subtracting growth rates of labor and capital inputs from the growth rate of output.

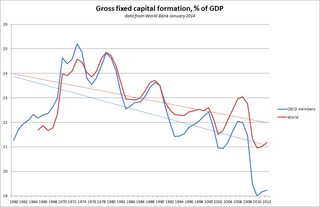

Gross fixed capital formation (GFCF) is a macroeconomic concept used in official national accounts such as the United Nations System of National Accounts (UNSNA), National Income and Product Accounts (NIPA) and the European System of Accounts (ESA). The concept dates back to the National Bureau of Economic Research (NBER) studies of Simon Kuznets of capital formation in the 1930s, and standard measures for it were adopted in the 1950s. Statistically it measures the value of acquisitions of new or existing fixed assets by the business sector, governments and "pure" households less disposals of fixed assets. GFCF is a component of the expenditure on gross domestic product (GDP), and thus shows something about how much of the new value added in the economy is invested rather than consumed.

In economics, gross output (GO) is the measure of total economic activity in the production of new goods and services in an accounting period. It is a much broader measure of the economy than gross domestic product (GDP), which is limited mainly to final output. As of first-quarter 2019, the Bureau of Economic Analysis estimated gross output in the United States to be $37.2 trillion, compared to $21.1 trillion for GDP.

Compensation of employees (CE) is a statistical term used in national accounts, balance of payments statistics and sometimes in corporate accounts as well. It refers basically to the total gross (pre-tax) wages paid by employers to employees for work done in an accounting period, such as a quarter or a year.

Net output is an accounting concept used in national accounts such as the United Nations System of National Accounts (UNSNA) and the NIPAs, and sometimes in corporate or government accounts. The concept was originally invented to measure the total net addition to a country's stock of wealth created by production during an accounting interval. The concept of net output is basically "gross revenue from production less the value of goods and services used up in that production". The idea is that if one deducts intermediate expenditures from the annual flow of income generated by production, one obtains a measure of the net new value in the new products created.

Workforce productivity is the amount of goods and services that a group of workers produce in a given amount of time. It is one of several types of productivity that economists measure. Workforce productivity, often referred to as labor productivity, is a measure for an organisation or company, a process, an industry, or a country.

Domar aggregation is an approach to aggregating growth measures associated with industries to make larger sector or national aggregate growth rates. The issue comes up in the context of national accounts and multifactor productivity (MFP) statistics.

In economics, gross value added (GVA) is the measure of the value of goods and services produced in an area, industry or sector of an economy. "Gross value added is the value of output minus the value of intermediate consumption; it is a measure of the contribution to GDP made by an individual producer, industry or sector; gross value added is the source from which the primary incomes of the SNA are generated and is therefore carried forward into the primary distribution of income account."

Production is the process of combining various material inputs and immaterial inputs in order to make something for consumption (output). It is the act of creating an output, a good or service which has value and contributes to the utility of individuals. The area of economics that focuses on production is referred to as production theory, which is intertwined with the consumption theory of economics.

Productivity in economics is usually measured as the ratio of what is produced to what is used in producing it. Productivity is closely related to the measure of production efficiency. A productivity model is a measurement method which is used in practice for measuring productivity. A productivity model must be able to compute Output / Input when there are many different outputs and inputs.

In the technological theory of social production, the growth of output, measured in money units, is related to achievements in technological consumption of labour and energy. This theory is based on concepts of classical political economy and neo-classical economics and appears to be a generalisation of the known economic models, such as the neo-classical model of economic growth and input-output model.

The annual United Kingdom National Accounts records and describes economic activity in the United Kingdom and as such is used by government, banks, academics and industries to formulate the economic and social policies and monitor the economic progress of the United Kingdom. It also allows international comparisons to be made. The Blue Book is published by the UK Office for National Statistics alongside the United Kingdom Balance of Payments – The Pink Book.

In Marxian economics, surplus value is the difference between the amount raised through a sale of a product and the amount it cost to the owner of that product to manufacture it: i.e. the amount raised through sale of the product minus the cost of the materials, plant and labour power. The concept originated in Ricardian socialism, with the term "surplus value" itself being coined by William Thompson in 1824; however, it was not consistently distinguished from the related concepts of surplus labor and surplus product. The concept was subsequently developed and popularized by Karl Marx. Marx's formulation is the standard sense and the primary basis for further developments, though how much of Marx's concept is original and distinct from the Ricardian concept is disputed. Marx's term is the German word "Mehrwert", which simply means value added, and is cognate to English "more worth".

References

- ↑ Thomas Kovarik; Jerin Varghese. 2019. Intrasectoral transactions. Monthly Labor Review .

- ↑ Sectoral output, OECD glossary of statistical terms

- ↑ William Gullickson. 1995. Measurement of productivity growth in U.S. manufacturing. Monthly Labor Review , p.14, citing the source "Accounting for Intermediate Input: The Link Between Sectoral and Aggregate Measures of Productivity Growth," in Measurement and Interpretation of Productivity (Washington, National Academy of Sciences, 1979), pp. 318–33.]